Regional gamers are in for a tough earnings season if PENN is any indication. The problem is deeper than just market softness.

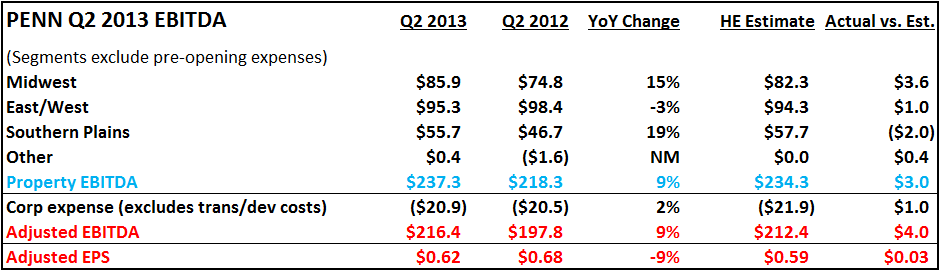

The table below details the soft quarter just posted by PENN. The quarter met recently reduced Street estimates but guidance was well below consensus. As we wrote about in our 07/15/13 preview, we expect an ugly earnings season from regional gaming companies. Might this earnings season finally be the negative fundamental catalyst we’ve been waiting for? We think so. Valuations have expanded, rightfully so given the real estate angle to which these companies are now viewed. However, estimates are clearly too high and massive long-term headwinds remains – that is, market saturation and a declining base of slot players. Baby Boomers are passing on and younger generations refuse to embrace slot play as a leisure pursuit.

We disagree with management that their issues are not something to worry about over the long-term. US same store gaming revenues may continue to be under pressure for years to come due to the demographics. Management also dismissed the impact of saturation yet many of their properties are facing new competition. That would at least partially explain why trips are down – demographics also contributes. And there is more to come. We think we will continue to see new markets open in the US as states continue to face long-term budgetary issues.

We’ve reduced our 2013 and 2014 EBITDA estimates to $825 and $867 million, respectively, pre-split. Note that we remain slightly above PENN’s new guidance for 2013 of $805 million. Following the drop in stock price and estimates, PENN now trades at 8.5x 2014 EV/EBITDA which seems fair. On a sum of the parts valuation basis, post-split, we value OpCo and PropCo combined at a range of $39-54. The midpoint of our valuation range falls a little below where PENN currently trades.