This note was originally published July 16, 2013 at 16:04 in Financials

One of Housing's Leading Indicators Grows Increasingly More Positive

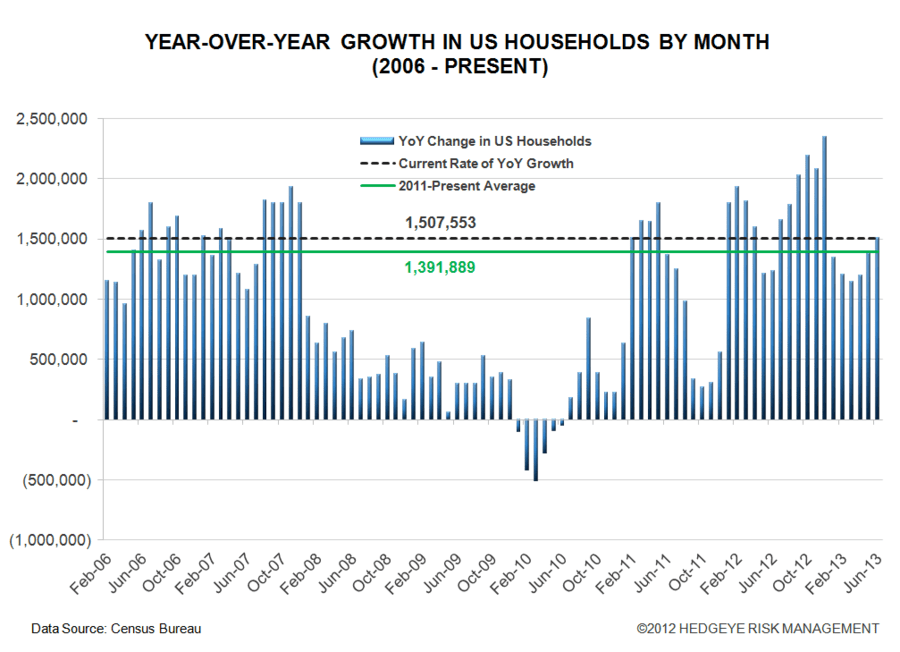

The latest household formation data is solid - a sequential acceleration. The Census Bureau just released its June household formation survey data, which showed that at the end of June there were 122,881,824 households in the United States. This data comes from their monthly phone survey of 50,000 households, which is statistically representative of the country as a whole.

The proper contextualization is to look at the rate of year-over-year growth since the data is not seasonally adjusted. On that basis, the U.S. added 1,507,553 net new households vs. June 2012. This is a rate in excess of the 2011-Present average of 1,391,889. In the charts below we present various snapshots of the trends in household formation. Most of the data is self-explanatory, however, the hatched red line in the second chart, for clarification, shows the rolling 12-month average rate of YoY growth. That figure currently stands at 1,655,470 through June.

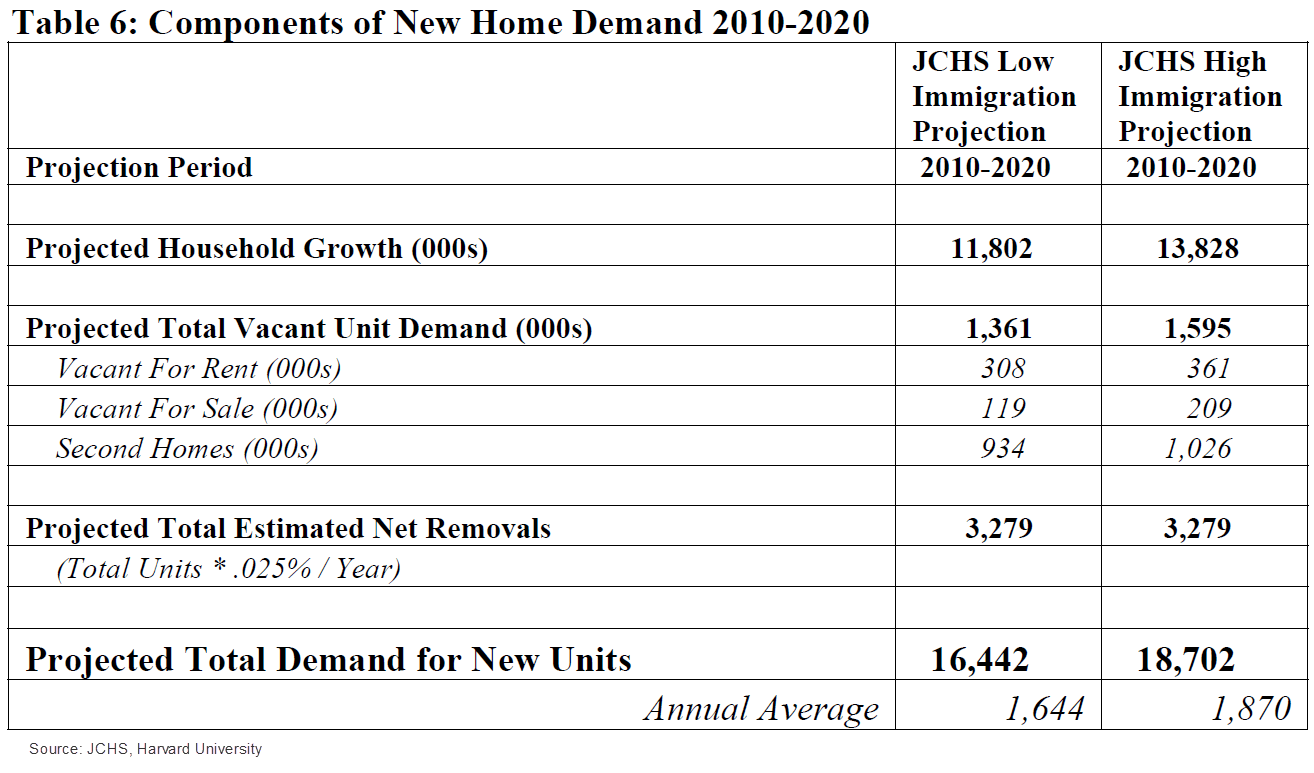

We wrote a note recently (May 15) entitled "Housing: A Double From Here?", in which we argued that the rate of building construction could double from present levels to ~2 million starts/year over time. For the detailed take on why we think that's likely, refer to our note. The executive summary, however, is that by applying the JCHS ratio of 1.35-1.39 new housing units to net new household formations (see the table above), and using the current rolling average rate of household formation, we find that we would need (1.655 * 1.35) = 2.2 million new starts. Using just the June data, we find a need for (1.507 * 1.35) = 2.03 million new housing units. For reference, this compares with the 0.914 million starts rate for May. We'll get the June data tomorrow. This morning's NAHB HMI builder confidence reading of 57, a 6 point month-over-month increase, also concurs with the trends we're seeing in HH formation.

The ratio of single-family/multifamily is open for debate, but we looked at this issue in our note (June 5) "Housing: Are Rising Rates a Big Deal", and concluded that a) ownership remains highly compelling vs. renting at the national level in spite of the recent back-up in rates, and b) the ratio of single family to total has averaged 72% since 1960 and is currently at 72%.

Last month we cautioned that in light of the recent run-up in rates, it would be more instructive to watch HH formation trends in June/July. Now, with the June data in hand, we think there's growing evidence that the rise in rates thus far hasn't derailed the housing recovery's momentum.

Joshua Steiner, CFA

203-562-6500

Jonathan Casteleyn, CFA, CMT

203-562-6500