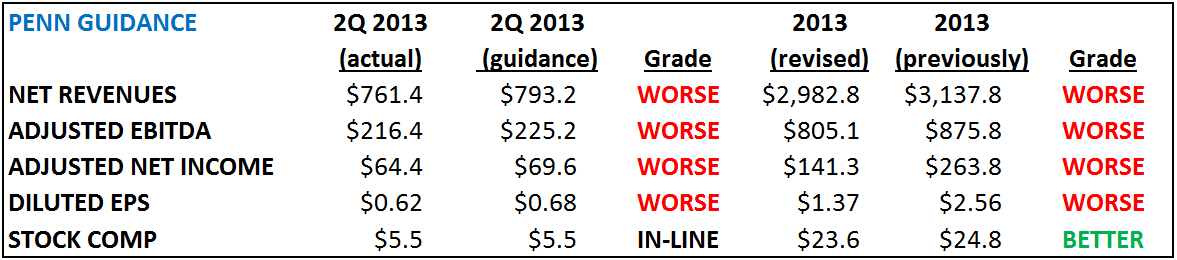

In an effort to evaluate performance and as a follow up to our YouTube, we compare how the quarter measured up to previous management commentary and guidance

OVERALL

- WORSE: A big cut in guidance confirms our regional gaming thesis. It's not just the economy. Demographics are a big headwind. Our model predicted a tough June but a flattish July. With management portraying July as similar to June, underlying demand is actually getting worse.

CONSUMER TRENDS

- WORSE: While spend per visit hasn't changed much, visitiation count has decreased a couple of % points. Consumers are more conservative with their discretionary spending. July trends are similar to June's.

- PREVIOUSLY: "Most of our data suggests that the weather had a big impact on visitation. We didn't see much change in spend per visit at our core properties year-over-year. Most of the effect was admission trends and visitation trends that I think were either impacted by new competition in our markets or weather-related. It doesn't seem to be any change in consumer spending when they do visit our properties. It's been more of the same, generally flat."

PROMOTIONAL ACTIVITY

- WORSE: Horseshoe Cincinnati has been very aggressive with discounting, pressuring Hollywood Columbus results, which has significantly underperformed expectations. Cleveland is another market that is highly promotional.

- PREVIOUSLY: "I would continue to characterize overall the promotional activity across these regional markets as fairly stable."

OHIO CASINOS

- WORSE: Mgmt says margins and market share at its Columbus facility are below their expectations. Its Toledo property's top line results have met their expectations though operating margins were weaker than they anticipated.

- PREVIOUSLY: "I think you're going to see another build that will start in the July-August timeframe as we hit the summer months as well. We're still working on marketing activities to continue to expose our new property to customers for the first time, and that's gone very well. Our repeat visitation has been very, very strong; our database growth continues to be very, very strong. So, this is very typical what we've seen in how Penn National opens a property in both Toledo and Columbus."

YOUNGSTOWN/DAYTON RACETRACKS

- SAME: Received approval from the Ohio Racing Commission for the relocation of Beulah Park in Columbus to Austintown in Mahoning Valley and for Raceway Park in Toledo to move to Dayton. Both facilities expected to open 2H 2014. PENN will be conservative with the slot count.

- PREVIOUSLY: "The two next projects are Youngstown and Dayton racetracks. Capital spend, which includes $125 million for license, basically a relocation fee and a gaming license. And so we're looking to $267 million and $257 million of cap spend, which will happen over the course of the next year and a half. We expect to open sometime in 2014."

SPIN-OFF FINANCING AGREEMENT

- SAME: No changes to financing costs. Mgmt sees no obstacles to completing the spin-off.

- PREVIOUSLY: "Next steps, we have to finalize the Carlino Group agreement. We need to finalize our financing agreements with our banks. We also have to start the process of refinancing of all of PENN's existing debt and putting in place the bank agreement, as well as the bonds for the transaction going forward. And then we would expect that in the fourth quarter that we'll complete the spin and the E&P purge will happen hopefully in the first quarter of 2014, at which point in time, we'll make our REIT election."

OH INTERNET CAFES

- SAME: Governor has given cafe operators 90 days to collect their signatures. Senate legislation has passed a bill enforcing the ban. Mgmt is hopeful the House will come back in early September and support the bill.

- PREVIOUSLY: "My expectation is once the internet cafes do get contained, we will see improved business volumes, and it's just going to be a wait and see approach on how we address the overall count in the Columbus operation. But I would expect at this point that the 2,500 count that we have there today will get us through 2013."

HOLLYWOOD ST. LOUIS RENOVATION

- SAME: Had significant construction disruption in 2Q. Remains on schedule with 5 months left of construction and on budget. $61MM have been spent with $32.8MM remaining on capex.

- PREVIOUSLY: "We're planning to spend roughly $61 million in total to rehab the property. One of the things about purchasing an asset from Harrah's was we recognized that there have been some deferred maintenance and also that the property needed to be refreshed and obviously the slot product needed some updating."