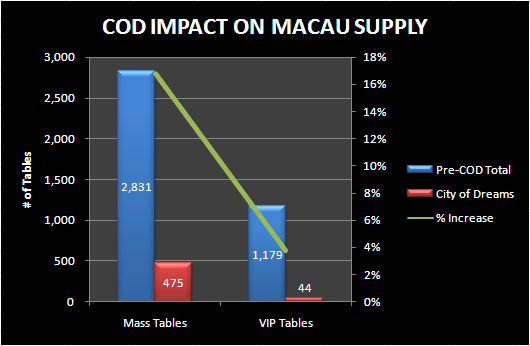

Crown's City of Dreams (COD) will open on June 1st. Unlike its sister property Altira, formerly Crown Casino, COD will focus on the Mass Market (MM) segment. Over 90% of COD's table games will be dedicated to MM.

So who are the other big MM players? Here's the breakdown of the Macau operators and their exposure to MM:

On the surface, SJM and LVS are most at risk of losing share from the opening of COD given their MM exposure. However, COD is situated on the Cotai Strip, across from The Venetian and Four Seasons. Cotai traffic will increase dramatically and cross visitation to the LVS properties should offset some of the capacity increase. I'm less enthused about the peninsula properties of SJM, MGM, and Wynn. The higher end Mass customer at Wynn Macau in particular seems to be a target of COD.

Over the intermediate term, however, the outlook is more positive. Macau remains possibly the only market with excess demand. Despite the visa restrictions, MM has been holding its own on a YoY basis. We adhere to the school of thought that Beijing will loosen the restrictions later this year to provide a tailwind to the new Macau Chief Executive.

The COD ramp will be interesting to watch. I expect COD to do quite well in the Mass Market business from the start. However, analysts consistently overestimate start up margins. Moreover, COD's strategy to market directly to VIP's, circumventing the high cost junket structure, is logical but also obvious. If it was so easy to do why hasn't anyone else (Wynn?) mastered the strategy. If they can figure it out God bless them. The property would be a home run.