CONCLUSION: UnderArmour footwear and apparel trends look solid headed into Thursday's print, especially in comparing wholesale sell-in versus retail sell-through. Retail inventory implications are bullish, and combined with a positive sales/inventory spread trend at UA, it's left with a particularly positive Gross Margin set-up. That's a big plus, because at 35x EPS it needs to beat, and expectations aren't low. If we had to make a bet one way or another (which we don't), we'd come out with an upwards bias.

DETAILS

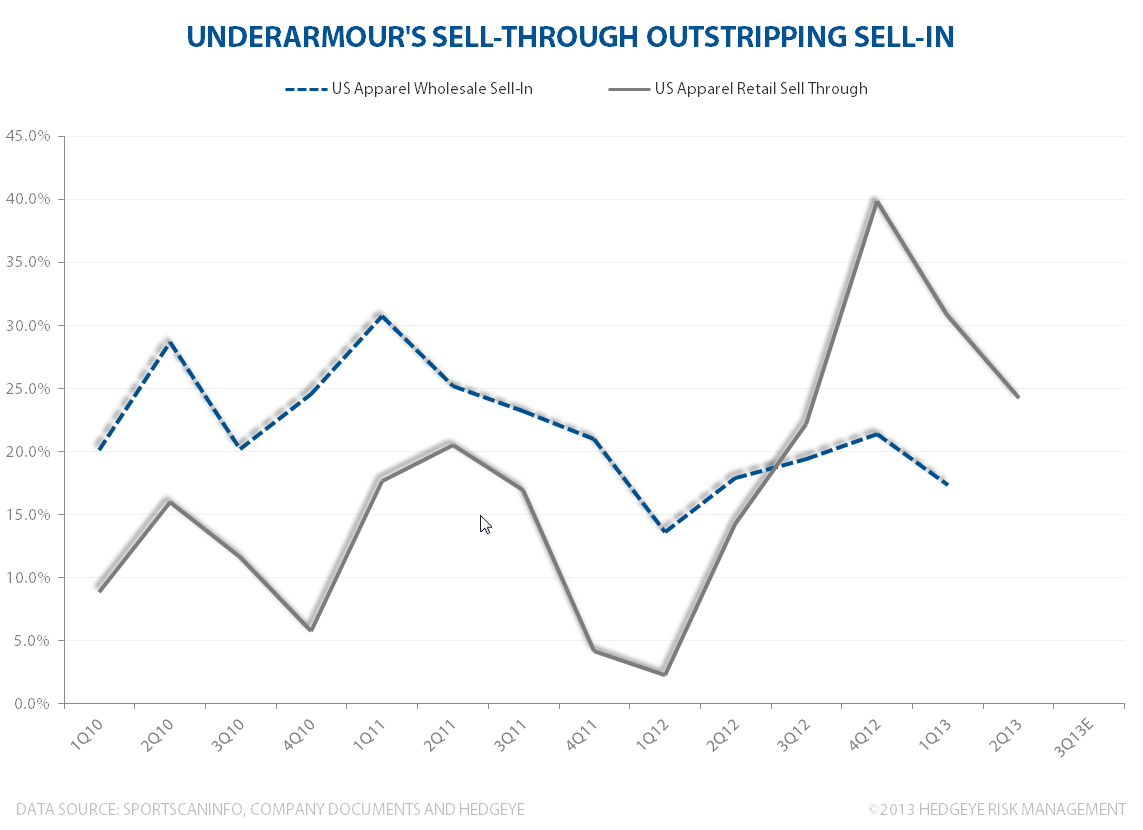

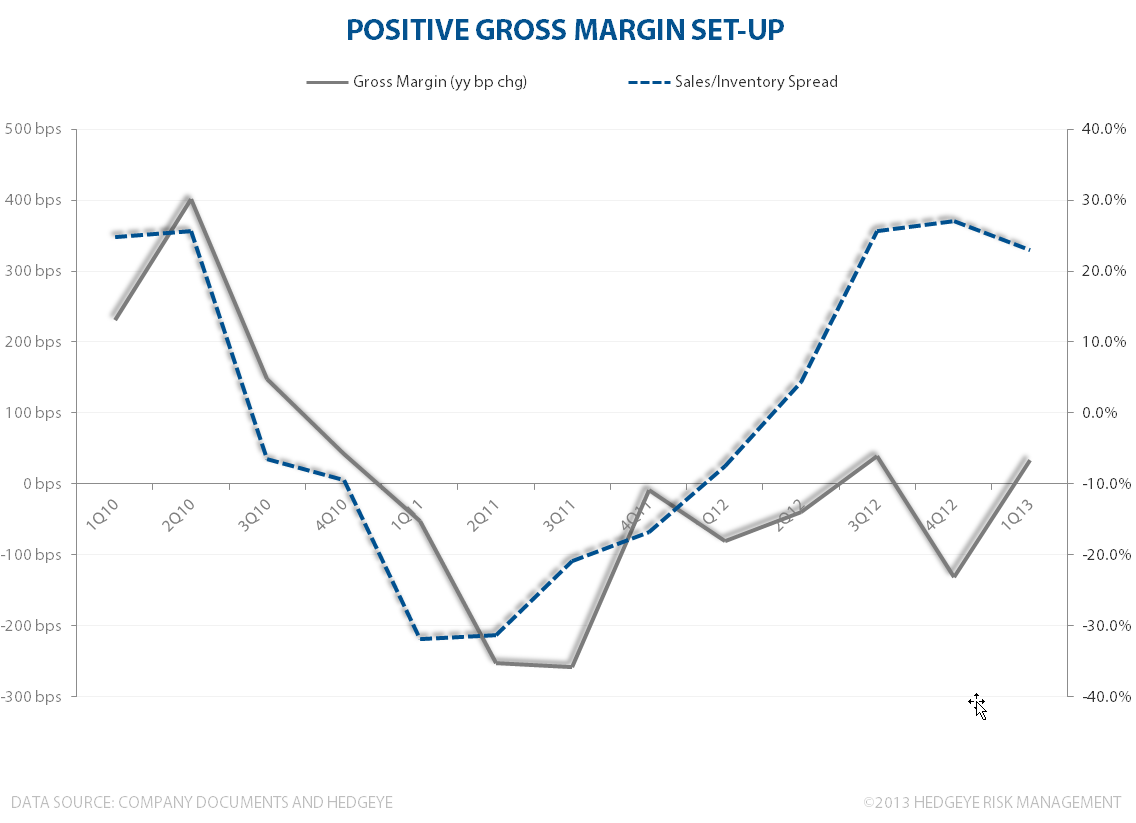

We think that UA's trends look quite positive headed into its print on Thursday. Our analysis shows that a) sell-through of apparel continues to outstrip sell-in, b) footwear is doing so at even a greater rate (and the Speedform launch is gaining traction), and c) the Gross Margin set-up is bullish given easing product costs and a favorable sales/inventory spread. All that said, we think that these trends are necessary to materially beat consensus estimates (a beat is critical for a 35x p/e growth stock). The good news is that our sentiment monitor suggests that this name remains extremely hated, which is a bullish stock setup.

One of the few risks we'd point to is if UA comes out and takes up SG&A requirements to grow the business as initiatives into Footwear and International markets become more important. This had been a concern of ours for a while, but after the company's analyst meeting last month we threw in the towel and altered our view (and our model) such that it could attain 20% top line growth without having to take the margin levels of the company sub-10%. But if it nudges up spending rates again after just having the investment community in Baltimore to sell its strategy -- then there are going to be credibility issues. We'd be surprised if this turns out to be the case.

So when we put it all together, we think that this is one of times where the consensus has it about right, but if we had to make a bet one way or another (which we don't), we'd have an upward bias.

UNDERARMOUR'S APPAREL RETAIL SALES HAVE BEEN GROWING AT A RATE FASTER THAN ITS WHOLESALE SELL-IN

Source: SportscanINFO and Hedgeye

UNDERARMOUR'S FOOTWEAR BUSINESS HAS BEEN OUTSTANDING -- AGAIN, WITH RETAIL OUTSTRIPPING WHOLESALE

Source: NPD and Hedgeye

SPEEDFORM HAS BEEN A RECENT DRIVER FOR THE FOOTWEAR BUSINESS. THIS IS THE MOST COMMERCIAL LAUNCH UA HAS HAD TO DATE

Source: UnderArmour

THE GROSS MARGIN SET-UP IS SOLID THANKS TO AND EXTREMELY FAVORABLE SALES/INVENTORY SPREAD AND FAVORABLE PRODUCT COSTS

Source: Company Reports and Hedgeye

OUR SENTIMENT MONITOR SHOWS THAT THIS STOCK REMAINS VERY HATED

Source: Hedgeye