We’ve said this 10,000 times before, but we’ll take this opportunity to repeat one of our favorite catch-phrases: “Big Government Intervention does two things: 1) shortens economic cycles and 2) amplifies market volatility”.

Both the sell-side and buy-side are explicitly bullish on the US Dollar – for many of the right reasons. But it’s also clear that a broad swath of Foreign Exchange market participants – including banks and corporations – have yet to go all in on #StrongDollar. This is likely largely due to the mixed and convoluted messages they continue to receive from Ben Bernanke.

Imagine what would happen to the USD and US interest rates if he took a vacation for a couple of months?

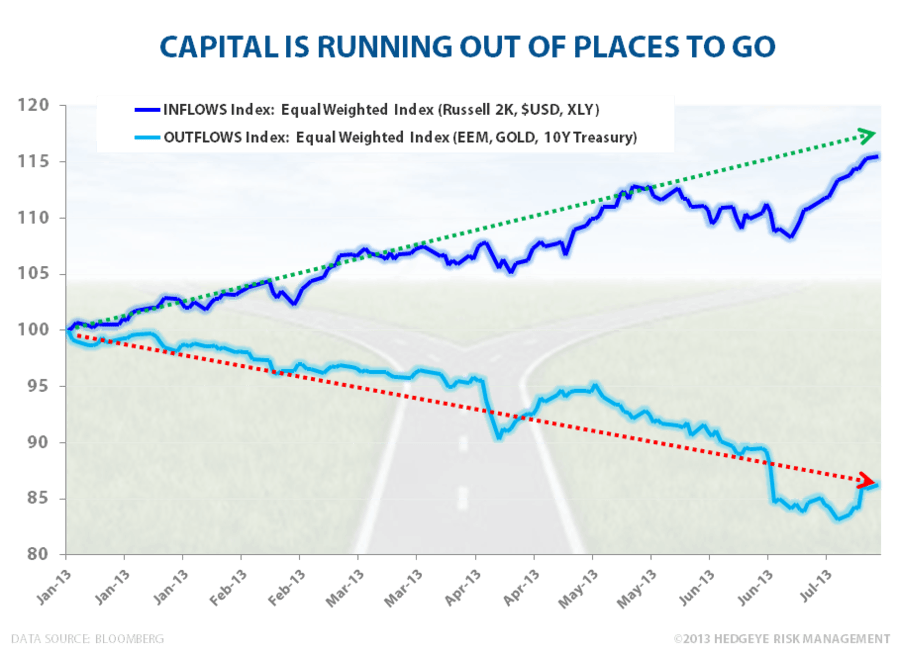

For the record, our #StrongDollar, #ShortGold, stay away from Treasuries, get the Federal Reserve out of the way, strategy has been the non-consensus bull case for growth all year.

Get Bernanke out of the way once and for all and we will witness a rip for the ages.