This note was originally published July 16, 2013 at 14:17 in Consumer Staples

KO is trading down today as volume results for Q2 2013 came in below expectations (globally +1% vs +4% last quarter) with the company citing a challenged macro environment (U.S., Europe, Asia, and Latin America), social unrest, and poor weather conditions (wet and cold across multiple regions) that impacted consumer spending and demand. North America, which is ~ 44% of sales, saw volume down a disappointing -1% in the quarter.

Performance was hit by tough Q2 comps given the especially good weather in 1H last year: Pacific volumes were +2% vs +10% last year; Brazil’s volume was even cycling +6% a year ago; and India’s volume grew +1% versus a +20% comp.

The company cited optimism around a turnaround in 2H for its key international markets (China, Brazil, Russia, Mexico, and India) on improvement in the macro environment, continued marketing support of its brands, weather improvements (India performs historically stronger in the back half), and its systems execution.

While we expect many of the forces dragging on confidence and demand to remain in the back half of the year, including high unemployment (especially in southern Europe), social unrest, and inflation, we like that the back half quarters of 2013 are lapping much easier comparisons year-over-year. On the top line, the Q3 2012 comp is +0.8% versus this quarter’s +2.8%. Gross margin was pretty consistent throughout last year, however the operating margin gets easier in the final two quarters of last year (+23.6% and +21.7%, respectively) versus +26.1% this quarter.

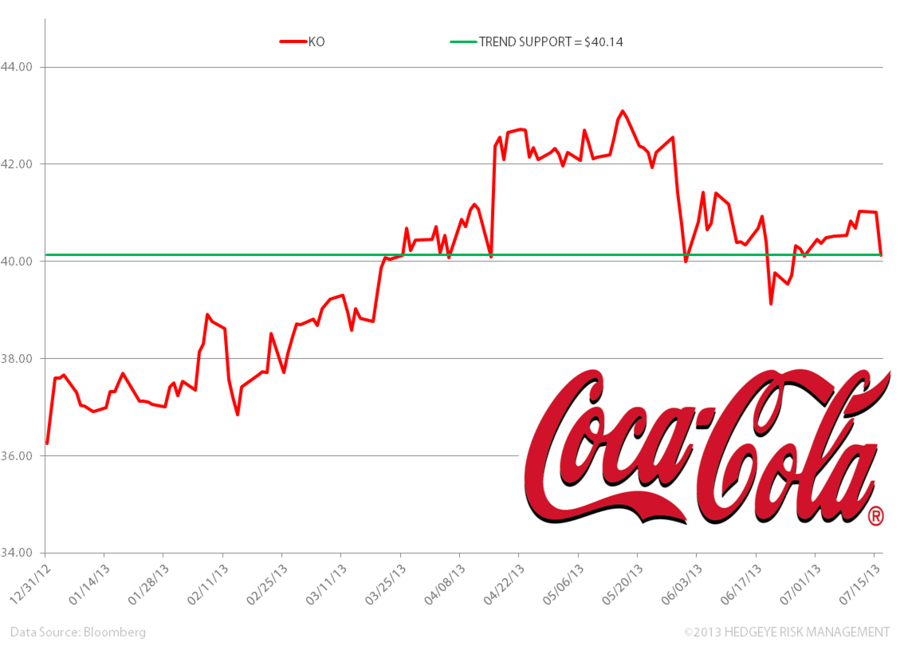

The stock is currently trading above its intraday lows at around $40.45. Our quantitative levels suggest that KO has an intermediate term price TREND line of support at $40.14.

What we liked:

- EPS inline with consensus at $0.63

- Outperformance of still beverages, volume +6% vs sparkling 0%

- Packaged water volume up +6% and energy drinks +5%

- Russia volume +11% with a strong marketing calendar tied to the 2014 Sochi Winter Olympics

- COGS decreased -5%

- Eurasia and Africa volume up 9% (benefitting from Aujan partnership)

- New guidance on the effective tax rate of 23.0% for 2013 vs last quarter’s estimate of 23.5%

What we didn’t like:

- Net Revenues were down -2.6% in the quarter and missed estimates ($12.75B vs $12.96B)

- Operating income fell -1.5% in the quarter

- Europe volume -4% (vs -4% in Q1 2013) on colder weather and flooding in Germany and central Europe

Matthew Hedrick

Senior Analyst