We continue to believe that Chipotle is one of the best positioned growth companies in the restaurant industry. The company reported a very strong 2Q13 and we continue to believe that it is well positioned for the balance of 2H13. Below are some of our thoughts on CMG’s 2Q13 results:

WHAT LOOKS GOOD

- 2Q13 same-store sales of 5.5% beat consensus of 3.7% (as extra day adds 1%) and the two-year trend remains steady at 6.8% vs. 6.9% in 1Q13.

- Management raised its guidance for 2013 same-store sales from “flat-to-low single-digits” to “low-to-mid single-digits.”

- We expect 2Q13 traffic of 4.5% to continue into 3Q13.

- $2.82 EPS was in line as a higher tax rate held back EPS by $0.04-$0.05.

- Increased marketing appears to be driving incremental traffic. Marketing costs increased to 1.5% of sales in 2Q13 compared to about 0.7% in 2Q12.

- The company ended 2Q13 with $775 million in cash and cash equivalent along with no debt.

- New restaurants are opening at (or above the high end) of the $1.5 million to $1.6 million sales target.

- The company is expected to delay raising prices in 2H13, as management remains focused on continuing to drive traffic and take market share.

- Chipotle opened 44 new restaurants in 2Q13, putting year-to-date openings at 92. It is clear to us that CMG is likely to exceed the high end of management’s targeted opening range (165-180 restaurants) for FY13.

POTENTIAL CAUSE FOR CONCERN

- The majority of our concerns stem from margin pressure.

- Restaurant level margin contracted -160bps in 2Q, primarily due to higher food costs.

- The company reported food costs to be around 33% of sales in 2Q13 as salsa, chicken and cheese added the most pressure to margins. We suspect that 33% may be the peak in food costs during the current cycle.

- We continue to monitor new unit performance very closely.

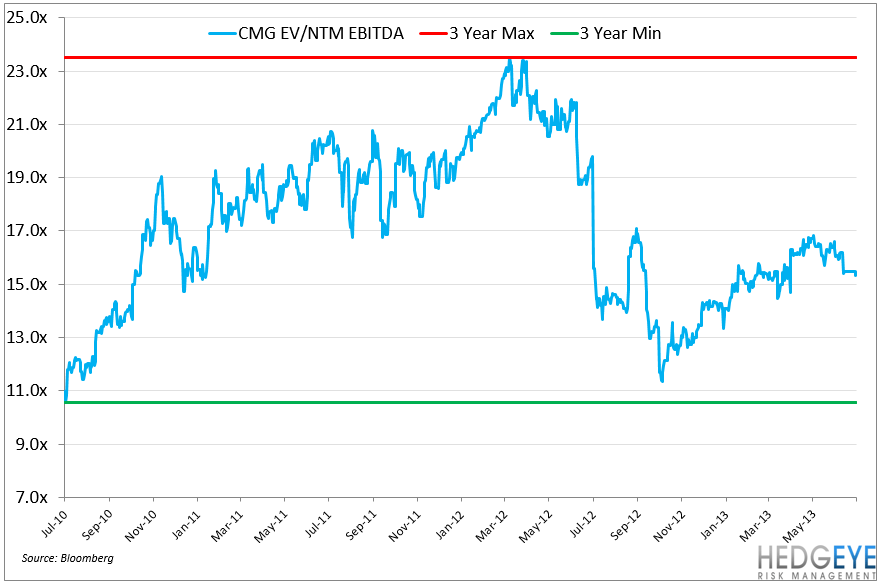

- Valuation is rich, but we believe the business model is built to stay this way.

Howard Penney

Managing Director