We remain bearish on MCD.

The stock has underperformed since we added it to our Best Ideas list on April 25 and will likely continue to do so. If we are right on the numbers, the situation could become worse than expected for shareholders.

MCD will report 2Q13 EPS before the market opens on July 22nd. For the quarter, the street is looking for 6% EPS growth to $1.40 on 3% revenue growth. We believe the 3% revenue target is aggressive and contend that the lack of leverage in the business model will disappoint investors looking for 6% EPS growth. In 1Q13, MCD reported 2% EPS growth on 1% revenue growth.

The company has a lot of work to do in order to improve their operational performance and we fail to see any indication that this will transpire soon. Looking forward to the 2Q13 earnings call, we expect to hear management’s recital of the (stale) tenets of the current Plan to Win strategy: “Optimize our menu, modernize the customer experience and broaden accessibility to brand McDonald’s around the world.” We believe 2Q13 results and the aforementioned message will fail to instill confidence in investors, as we do not see the current leadership coming up with ideas innovative enough to counteract the company’s current operating headwinds.

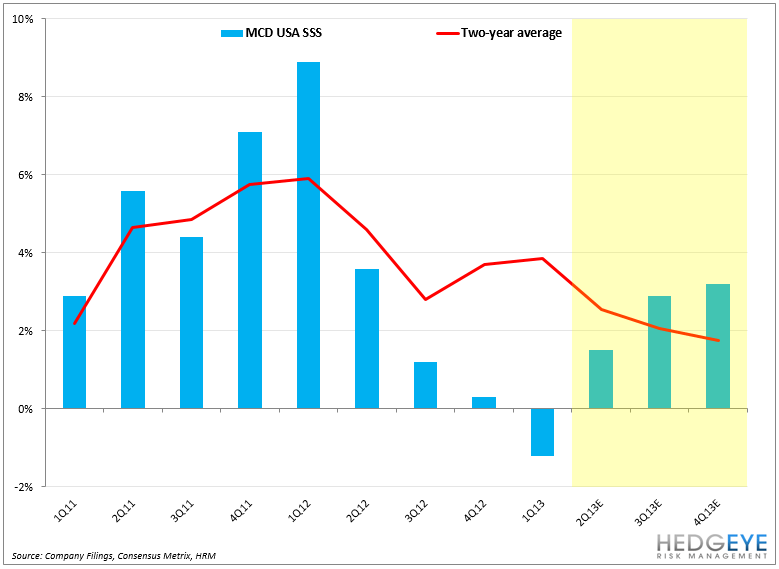

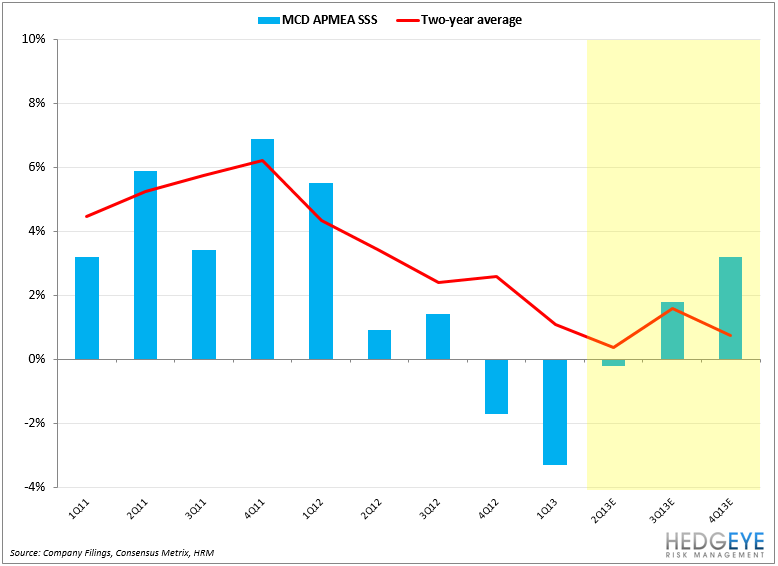

SALES TRENDS

The short case we laid out back in April was predicated on MCD missing 2H13 sales numbers. We’ve always envisioned the June/July timeframe to be when our thesis begins to truly materialize. July is the time when most of the 2013 menu strategy has been implemented, effectively giving the street a better indication of how management is addressing the current issues. Looking at the three key regions, expectations are for a recovery in sales, however, we give little merit to this view given that the 2-year sales trends appear to be decelerating.

HEDGEYE – We will get a closer look at June sales trends and management’s early view on July trends when MCD reports 2Q13 results. We believe that both months will produce results below street estimates.

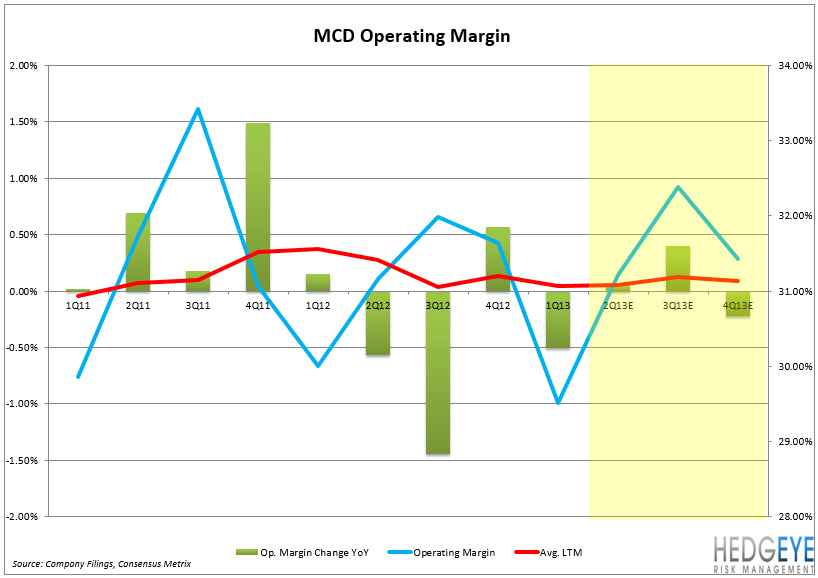

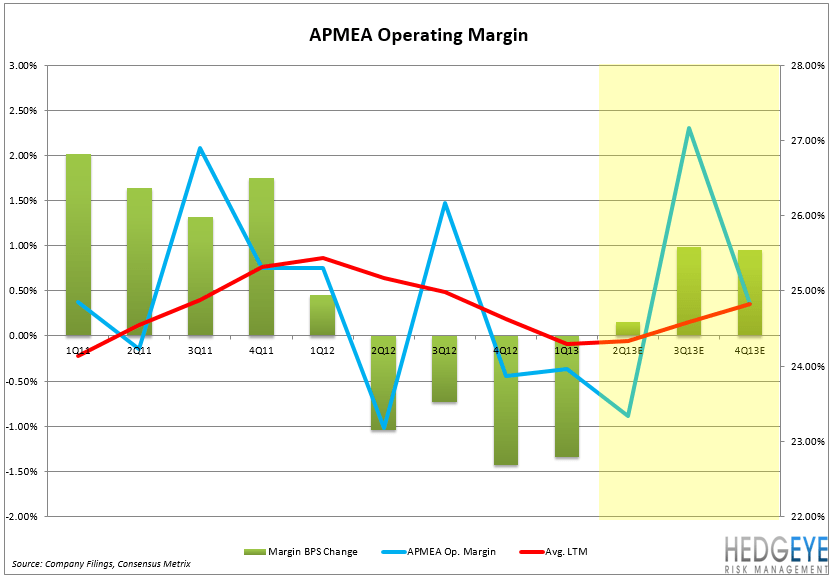

MARGINS

A quick look at MCD’s restaurant level margin will show you why the franchisee community is upset with management’s current business plan. Although the trends in restaurant level margins are less meaningful than the operating margins, they still matter. With that being said, on an annual basis, since the peak of 4Q10, MCD has given up nearly 180bps of restaurant level margins.

In contrast, enterprise operating margins have held up significantly better. On an annual basis, operating margins peaked in 1Q12 and have only declined 47bps since. Naturally, there is less volatility in operating margins, but expect sustained subpar same-store sales to inflict further pressure on margins.

Regionally, operating margins are down 110bps, 85bps and 59bps in the APMEA region, the U.S. and Europe, respectively. Given current trends, we believe MCD is vulnerable to further margin declines in both the U.S. and Europe.

HEDGEYE – We suspect that a 40bps decline in restaurant level margins will be in line with what the company will report. Furthermore, we contend that current street expectations for operating margins to hold flat in 2Q13 and to increase 40bps in 3Q13 are overly optimistic.

FOOD COST TRENDS

Since the lows in 4Q10, MCD has seen global food costs rise 132bps to an estimated 34% of overall sales in 2Q13. While McDonald’s has a very strong supply chain, it is likely that the company will continue to see their food costs rise for the foreseeable future, particularly due to its exposure to red meat. MCD benefited greatly from lower food costs in 1Q13, but we expect to see this trend reverse for the balance of 2013.

MCD has guided food inflation to be within the 1.5-2.5% range. Europe’s food inflation was up around 2.5% in 1Q13 with expectations of a comparable increase in 2Q13. Full-year food inflation for the region is estimated to be in the 2.5-3.5% range.

HEDGEYE – We’d be remiss not to note that any food inflation will have an adverse effect on the franchisee community.

LABOR COST TRENDS

In comparison to food costs, MCD had seen very stable labor cost trends over the past two years. We believe that the company will continue to face upward pressure on its labor costs for the foreseeable future.

HEDGEYE – If the company wants to regain traction on improving same-store sales it will not be accomplished using fewer workers. Labor costs are headed higher!

OTHER OPERATING TRENDS

Other operating costs were MCD’s largest source of margin decline in the U.S. in 1Q13. Overall, operating costs increased 41bps year-over-year, a trend that should persist for the remainder of 2013.

HEDGEYE – Similar to labor cost trends, MCD will experience higher costs across the P&L as management seeks to implement a more cohesive strategy to improve traffic trends.

SENTIMENT

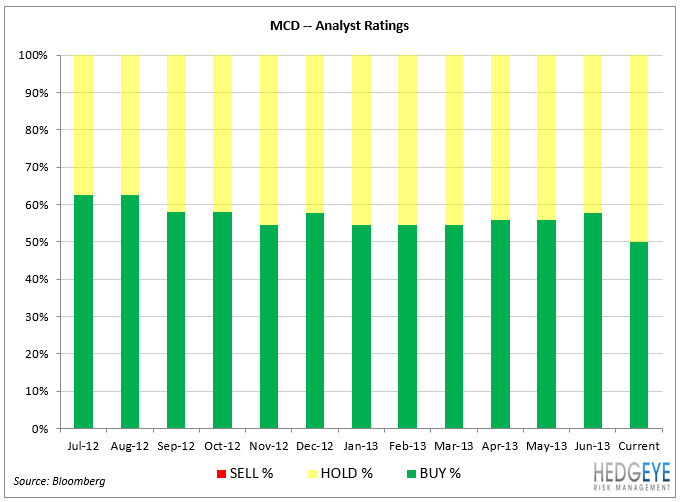

Highlighted in the chart below, 50% of analysts rate MCD a Buy while the other 50% rate MCD a Hold.

This puts sell-side sentiment regarding the stock approaching levels not seen since 2004. Further, short interest in the stock is only 0.91% of the float.

HEDGEYE – I believe that the 2Q13 results will confirm our bearish thesis on MCD. The street may have a bearish bias on MCD, but are they bearish enough?

VALUATION

McDonald’s stock is up 14.4% YTD, below the 17.5% increase in the S&P 500. At 10.6x EV/EBITDA MCD is trading significantly below the QSR peer group trading at 12.3x EV/EBITDA.

HEDGEYE – McDonald's aforementioned operational issues suggest that the stock might be trading at a higher implied multiple. Valuation is not a catalyst!

Howard Penney

Managing Director