While the Fed’s employment of its dovish-leaning “communication tool” continues to deliver a diminishing marginal impact on yield chase and inflation hedge assets, the positive gravity of the domestic macro data, and the labor market data specifically, continues to pull the growth trade (small/mid cap, higher beta, domestic, consumption oriented) higher.

This week’s data extended the trend of positive acceleration in the labor market, which continues to buck the seasonal trend of the last 3 years and register ongoing improvement despite any existent fiscal policy related drag.

Below is the breakdown of this morning's claims data, along with some sector specific takeaways, from the Hedgeye Financials team. If you would like to setup a call with Josh or Jonathan or trial their research, please contact .

-------------------------------------------------------------

Auto Tailwinds, But Robust Nevertheless

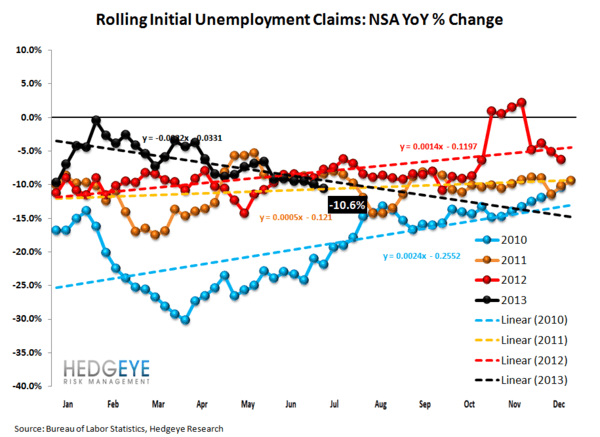

The labor market continues to improve at an accelerating rate. This week, rolling NSA initial claims were 10.6% below their level last year. This compares with the 10.1% YoY improvement posted in the prior week and 9.5% improvement in the two weeks prior to that.

There are a few potential narrative overlays (i.e. explanations) for the amount of strength we're seeing in the data. The first is ACA, i.e. Obamacare, prompting the hiring of more part-time and temp workers, on the margin.

The second is the auto industry, which normally shuts down its production plants for two weeks around July 4th. Auto workers are entitled to file initial unemployment claims for these two weeks. This year, however, due to stronger new car demand and critical, new model rollouts from GM and Chrysler, many of these plants have remained open. For instance, Ford said back in May that 21 of its North American factories will shut for only one week this summer. GM said it would idle its factories for only short periods, and Chrysler said it would close just 4 of its 10 North American assembly plants during the traditional two-week break.

While it's tough to know how many workers this positively affected, it is likely to exert some upward pressure on SA claims in the week or two ahead.

The bottom line here, however, is that the labor market continues to mend at an impressive rate. We think credit-levered, value Financials (BAC, COF) remain optimal ways to play this on the long side. BAC's results on Tuesday were very strong, fueled primarily by housing's improvement and its associated benefits to falling lititgation costs, but underpinning that is the recovery in labor. COF reports tonight. We recently published a note outlining our bullish view on COF across all three durations (short, intermediate and long term).

The Data

Prior to revision, initial jobless claims fell 26k to 334k from 360k WoW, as the prior week's number was revised down by -2k to 358k.

The headline (unrevised) number shows claims were lower by 24k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims fell -5.25k WoW to 346k.

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -10.6% lower YoY, which is a sequential improvement versus the previous week's YoY change of -10.1%

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT