We assess the electronic cigarette (e-cig) company Vapor Corp., a common stock listed on the OTC Bulletin Board under VPCO.

We caution that VPCO is a potentially volatile stock, thinly traded, however over time we believe in the growth of the e-cig category, including the opportunity for smaller players (non Big Tobacco) to compete in the space, and VPCO is the sole pure e-cig play that is publically traded.

On the Industry

We believe e-cigs may be the first truly new consumer product in the markets in many years. They offer a compelling alternative to traditional cigarettes and offer a consumer a much different experience than a nicotine patch or gum. The involvement of Big Tobacco (RAI, LO, MO) in the category should continue to lend credibility to e-cigs and accelerate growth; we expect e-cigs to be margin-enhancing to the combined cigarette category for Big Tobacco and 2014 to be a breakout year for them, having tested the waters (through acquisition and mix) through 2013.

U.S. e-cigs sales were projected at $150MM in 2011, $500MM in 2012 ($300MM across retail channels and $200MM over the internet), and are estimated to be around $1-2B in 2013. We think there is a huge runway for converters in the $90B annual tobacco industry: in America alone, nearly one in five American adults smoke. Finally, we expect e-cigs consumption will continue to benefit from its significant price point advantage over traditional cigarettes (~ 4-5x cheaper after the cost of the start-up kit) which will help to grow repeat purchase behavior.

That said we want to emphasize that e-cigs remain a miniscule portion of the portfolio for Big Tobacco, around 1%, whereas VPCO is a 100% e-cig company. There exists no basis for comparing the growth trajectory of a small e-cig company given its uniqueness as the sole publicly traded e-cig company and given the newness of e-cigs to the market.

About the VPCO Business

The company was originally incorporated as Miller Diversified Corp in 1987 and operated in the commercial cattle feeding business until October 31, 2003 when it sold all of its assets and became a discontinued corporation. On November 2009, it acquired Smoke Anywhere USA, Inc., a distributor of e-cigs, in a reverse triangular merger, and e-cigs became its sole operating business. On January 7, 2010 the company changed its name to Vapor Corp. and VPCO commenced trading on the OTC Bulletin Board on May 11, 2010.

The company currently has a market cap of $60.8MM, with 60.2MM shares outstanding, and a float of 29.5MM shares. It is not institutionally owned, has an average trading volume of 580K shares over the last 30 days, and short interest as a percentage of the float of 0.1%. The company offers no cash dividends.

The thirteen former stockholders of the subsidiary Smoke Anywhere USA, Inc., own in excess of 50% of the outstanding common stock. The largest shareholders are all Executive Officers and/or Directors of VPCO: Doron Ziv (11.53%), Jeffrey Holman (9.14%), Tamar Galazan (8.89%), Adam Frija (7.41%), Kevin Frija, President and CEO (7.15%), Isaac Galazan (6.86%). Highly concentrated insider ownership can cut both ways: the insiders have strong motivation to make the company succeed, but they may also have strong motivation to get out of their stock.

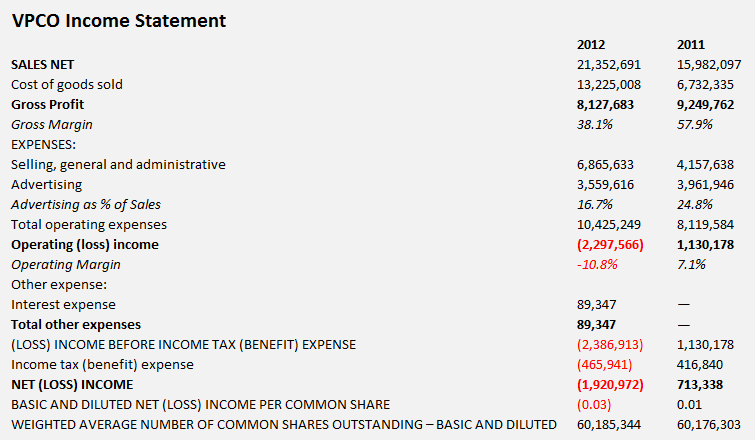

VPCO had sales of $0.51MM in 2008, $7.96MM in 2009, $10.91MM in 2010, $15.98MM in 2011, and $21.35MM in 2012. Its current distribution of sales is 75-80% through wholesalers (in a combined 60K doors) and 20% via its web and TV infomercial businesses. [It also has a private label distribution in Canada and unique agreement with an Indian tribe]. Its business is primarily focused in the U.S. and currently it has no international involvement or interests.

VPCO’s E-cigs

With about four year in the business, Vapor Corp is a 100% electronic cigarette (e-cig) company with 10 different brands, including Krave, Fifty-One, Green Puffer, Americig, Vapor-X, EZ Smoker, Alternacig, Fumare, Hookah Stix, and Smoke Star.

Its best-selling brand, Krave, is available across all retail channels and ranks as approximately the 8th top e-cig brand with around 1.2% of the dollar share or ~$4.3MM of sales (according to Nielsen data as of the 52 weeks ended 3/16/13). For reference, the NJOY brand (Privately held) remains the e-cig market leader with a 26.3% dollar share on $96.7MM of sales, ahead of the #2 player BLU (Lorillard:LO) with 24.8% share, and the #3 player Mistic (Private: Ballantyne Brands) with 17.8% share.

Its target consumer is anyone that smokes, with a sales split of disposable versus rechargeable e-cigs slightly favoring disposable. Its disposable unit has 250-500 puffs with a MSRP of $7-12/unit. Its rechargeable unit has a starter kit (battery, filter, and USB charger) that retails for $19.99 and replacement cartridges with a MSRP of ~ $2-3, per unit, with discount as the pack size increases (sold in increments of 5).

VPCO has a wide range of brands and styles of e-cigs, with different strengths and flavors. Strengths of nicotine range from 0-2.4%. VPCO has e-cigs that have 0% nicotine, including Hookah Stix that target a flavor experience. Other products have a scale of nicotine strength: low (1.4%), medium (1.8%), and high (2.4%). Flavors range from passion fruit to coffee to bubble gum, beyond traditional and menthol flavors.

The company currently sells slightly more disposable e-cigs, which are less profitable than rechargables (no specific margins were disclosed in a discussion with management) and its retail distribution is primarily to major retailers, which as a retail segment also diminishes its margins. [Note: Ballantyne Brands, maker of the e-cig Mistic, said that its gross margin for disposables is in the 40’s (%) and that rechargeable e-cigs are north of that figure, considering the consumer already purchased the battery in a starter kit].

Currently, the company cannot sell its products in the states of Maine or Oregon.

The Need For Cash

We believe the company is likely to have an ongoing need to raise fresh capital until its profitability improves, given its size and ambition to earn profitable growth while expanding its distribution. A capital injection would allow it to better fund larger volume buys from its suppliers to command a volume discount and to fund increased marketing support and distribution. As the e-cig business continues to become increasingly competitive, a key risk is the inability of a smaller player like VPCO to take price, leaving few levers (beyond volume discount buying) for VPCO to pull on its input cost line. COGs rose dramatically in FY 2012: VPCO’s gross margins went from 57.9% in 2011 down to 38.1% in 2012 as sales increased to $21.4MM from $15.9MM in 2011, or a 33.6% gain year-over-year.

Any small growth company must spend to grow, yet given the 2012 operating and income losses, the competitiveness of pricing in the e-cig market, and increased labor costs in China, an investment would allow VPCO to grow its marketing spend (which declined to 16.7% of sales in 2012 vs 24.8% in 2011), increase its distribution across retail, and allow it to better manage its COGSs.

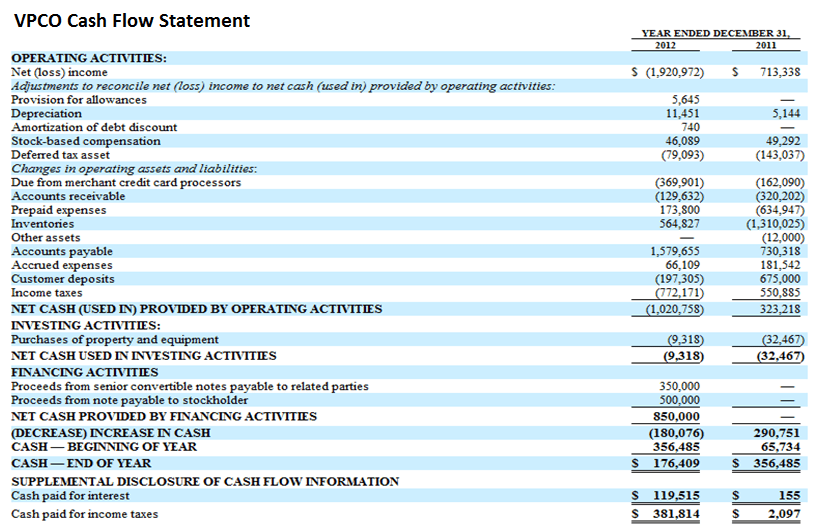

For reference we've included the balance sheet and cash flow statements at the end of this note. VPCO has total liabilities of $4.9MM as of December 2012, including long-term debt in the form of a senior notes: the company borrowed $500k on July 9, 2012 from Ralph Frija, father of CEO Kevin Frija and a less than 5% stockholder of the company, with an interest of 24% that matures on January 8, 2014. Then on 6/9/13 Ralph Frija, Jeffrey Holman, and Ms. Vaccaro in aggregate purchased the company’s existing Senior convertible notes worth $350K. These transactions suggest that the company is already tapping channels for capital; we believe the company will likely continue to seek capital to fund its operations.

Other VPCO Risks

Other risks for VPCO (and shared for most players in the industry) include general safety concerns of its product, inability to enforce quality control of its Chinese manufacturers, supply chain disruptions given its dependence on third party suppliers, and any impacts of a pending ruling from the FDA on e-cigs. As we’ve stated before, we believe the FDA will maintain that taxes be concerned at the state, not federal, level. Potentially damaging could be any restrictions from the FDA on online sales for VPCO as well as and any additional restrictions on advertising, marketing, package design, and/or where e-cigs may be smoked.

We believe the patent infringement charges brought against VPCO by Ruyan (a Chinese e-cig manufacturer that VPCO does not purchase from) are largely rear view. It settled the first claim brought against it for $12K (on 3/1/13) and management believes the court’s current “stay” on the second charge (originally filed on 6/22/12) should be overturned, or result in a diminimus fine.

We’ll be monitoring this company and may opportunistically add it to our real-time portfolio positions. We do not currently have a position in VPCO, but it factors bullish across our immediate and intermediate term TRADE and TREND durations (see the chart directly below).

We’ll be revisiting this name and electronic cigarettes as we increase our coverage of the tobacco industry.

Matthew Hedrick

Senior Analyst