An aggressive share repurchase program and strong share price momentum year-to-date has led to some discomfort for KMB bears. We would avoid the long side in this name ahead of the 7/22 2Q earnings print.

Conclusion

A bear case is emerging in this stock; a steep valuation (17.5x NTM earnings) with 3-5% top line growth and the commodity headwind stiffening. EBIT growth has largely been driven by cost savings and benefit from raw materials costs over the last year. We would not be short – yet – but believe that investors looking for longs in staples should look elsewhere. According to our macro team’s quantitative levels, the stock has climbed back above its TREND line, on low volume. A chart illustrating these levels is below.

1Q Strength Likely Faded in 2Q

We would expect 2Q results to be sequentially weaker in terms of operating leverage and sales growth as the company recently highlighted a “cautious” U.S. consumer. Slowing growth in emerging markets (over 20% of KMB revenue) is likely to weigh on consensus’ outlook on K-C International (KCI) for the balance of the year. The value of the US Dollar, over the intermediate- and long-term, is important for KMB as it looks to grow its presence in emerging markets. That said, 1Q was the most difficult compare of the year, so we will be watching EBIT growth and listening for any related commentary on how income growth is likely to trend over the balance of the year.

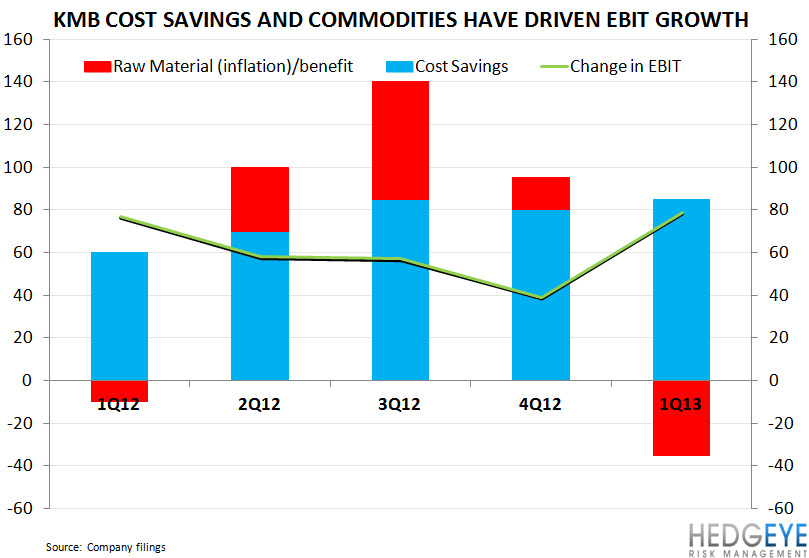

EBIT Growth Puts and Takes

Management has stated its confidence in finding cost savings in the $250-300 million range, annually, going forward. This will help the company leverage its sales growth but we believe, unlike in 2012, raw material costs are likely to offset cost savings for the remainder of the year. As we mentioned in our 6/10/13 note, “KMB – REMOVING FROM OUR BEST IDEAS LIST”, “[in February] KMB gave its planning assumption of northern bleached pulp at $890 - $910 per metric ton and oil at $90 - $100 per barrel. In total, the Company guided to $150 - $250 million in cost inflation.” With crude oil prices at $105 per barrel and NBSK Pulp steadily rising year-to-date to $947 currently, we will be interested to see if management addresses the topic of input costs on July 22nd.

The first chart, below, offers an illustration of year-over-year EBIT growth, in dollars, versus the year-to-year impact of cost savings and raw material costs on the P&L. Those line-items, in aggregate, are likely to be less of a tailwind in each of the remaining quarters.

Rory Green

Senior Analyst