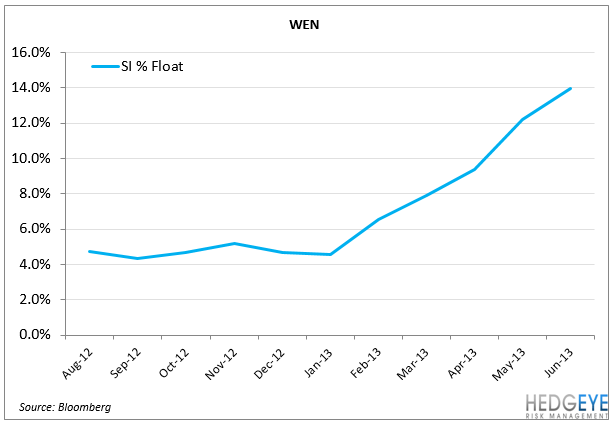

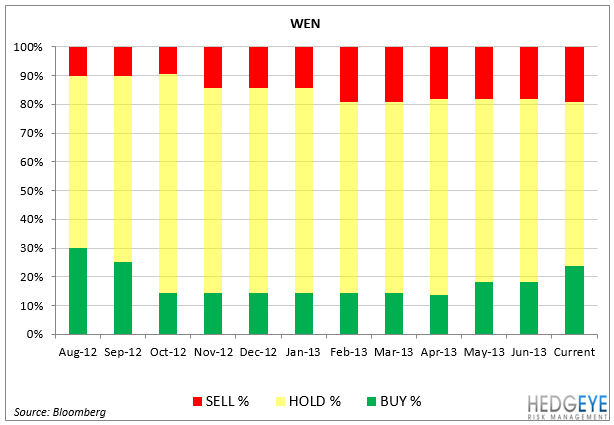

As highlighted in the two charts below, WEN short interest has risen from 7.9% at the end of 1Q13 to 13.97% today. In addition to the high short interest, 19.0% of analysts currently rate WEN a Sell compared to 23.8% of analysts that rate stock a Buy.

We were previously of the view that the run in WEN was over and the stock was likely “to take a breather,” as its price performance was largely driven by multiple expansion rather than earnings revisions. Admittedly, there are a lot of names in the restaurant industry currently trading with stretched valuations. However, our opinion on Wendy’s is changing as the new Pretzel Bacon Cheeseburger appears to be exceeding expectations. Since the July 4th launch, we are hearing that same-store sales are running well into the double digits thus far.

How much of the recent spike in the stock is due to short covering rather than new buyers remains unclear. That being said, at 13.97% short interest, we anticipate more short covering and potentially some upgrades coming out within the next few weeks.

The recent success of Wendy’s new product launch gives us more conviction that MCD continues to struggle amidst an increasingly competitive environment.

Howard Penney

Managing Director