Either everyone is at the beach… Everyone is waiting for our Central-Planner-In-Chief's latest messaging ("To Taper, Or Not To Taper") signal tomorrow… or everyone’s waiting for the guy next to them to make the first move.

But any way you slice it, it looks like no one has any real conviction on either side at these levels.

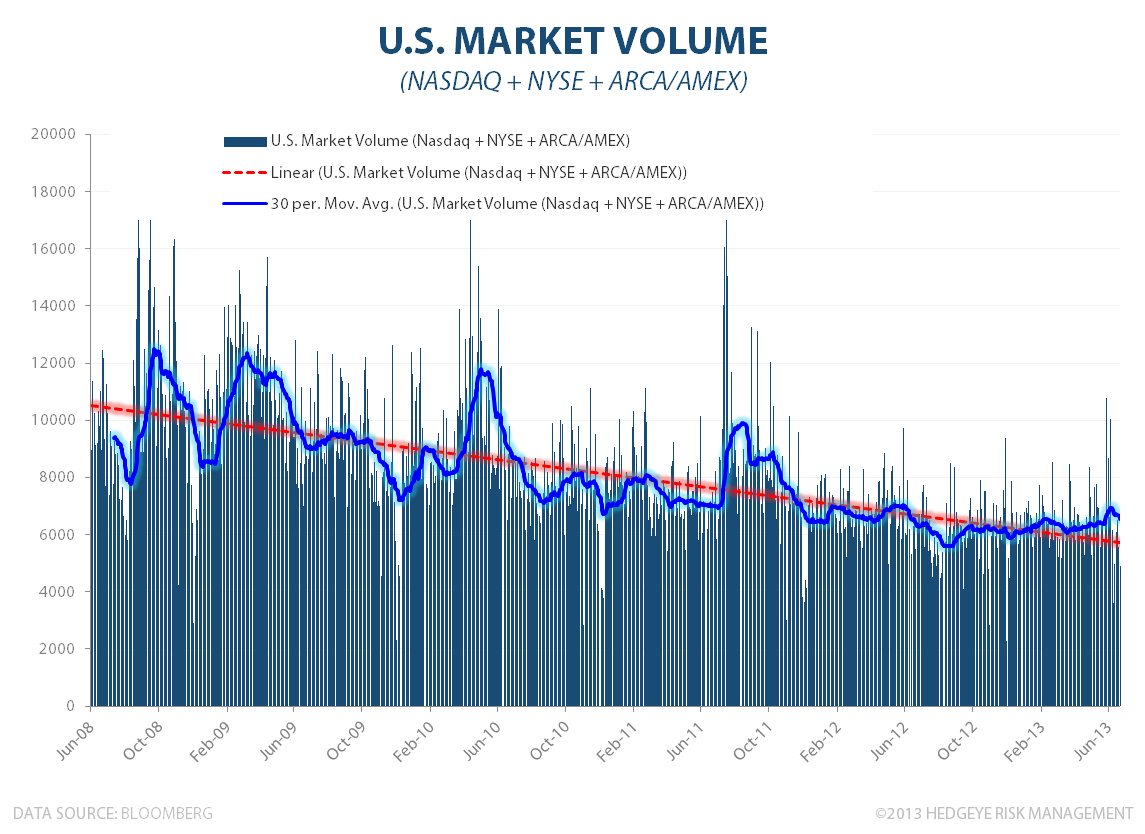

Of course, depressed volume is not a new phenomenon as the trend in aggregate market volume has been one of decline as the 2nd chart below illustrates. Soft volume month-to-date (around the July 4th Holiday) is not particularly surprising.

That said, this ain’t the stuff convicted new market highs are made of. Keep your head up out there.