Prior to Monday’s retail sales data point, the broad restaurant macro indicators have been gradually improving and restaurant stocks have surged. As we mentioned in a post last week, casual dining sales trends look more like the recent retail sales print – very disappointing. CMG will report on Thursday and give the street a more relevant look into the how the industry is faring.

Overall, consensus estimates indicate the expectation of a challenging quarter for Chipotle. Consensus is looking for a 16% increase in revenues and only a 10.5% increase in EPS, numbers similar to 4Q12 when the company had little leverage in its business model. Over the past three months, the consensus estimates for 2Q13 have remained relatively stable, while the stock has returned 14.6% versus the S&P 500’s 8.2% gain.

The street remains on the bearish side of CMG, but this trend has been improving. Short interest is currently at 9.09% of the float, the lowest it has been in a year, as valuation appears rich but not excessive. We continue to believe that Chipotle is one of the best positioned growth companies in the restaurant industry.

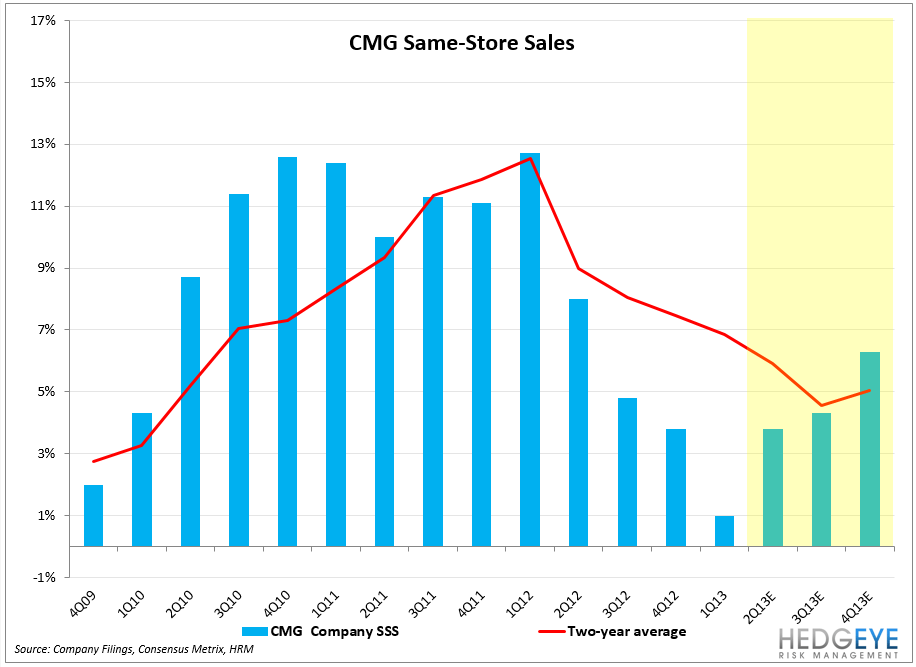

SALES TRENDS

Coming into 2Q13 earnings, management has guided to flat to low-single digits same-store sales before the impact of any future menu prices increases. In the second quarter, the company lost 70bps of price, but was able to pick up an incremental trading day due to Easter’s impact on 1Q13 results.

The street is looking for a sequential improvement in same-store sales of 3.8% in 2Q13 versus 1.0% in 1Q13. The 2Q13 number is slightly better than the implied 3% run rate the company had previously alluded to as the trend line at the conclusion of 1Q13. Overall, this implies a 100bps slowdown in the two-year trend to 5.9%.

The potential for an upside surprise to the 2Q13 same-store sales estimates could be driven by a significant increase in marketing spending over the course of the quarter. In 2Q13, CMG likely spent 2% of sales on marketing, up from 0.7% in 2Q12.

HEDGEYE – We believe the street’s estimate for 3.8% same-store sales growth in 2Q13 is conservative.

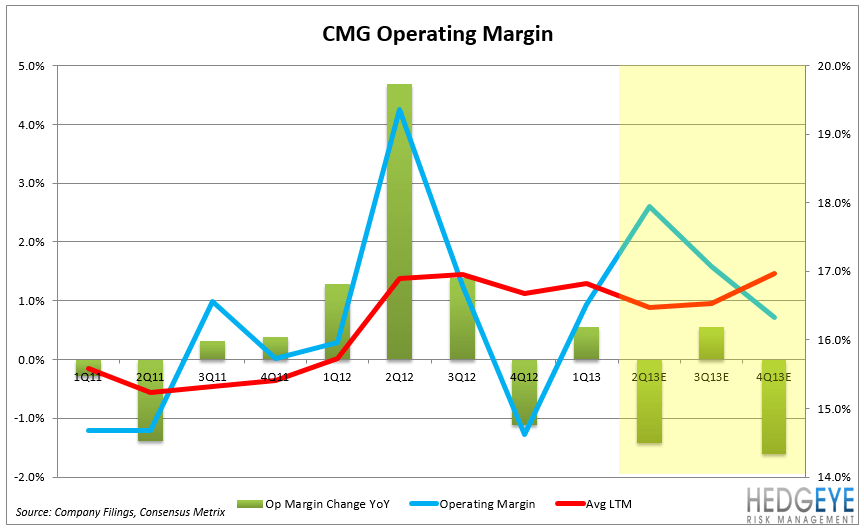

MARGINS

Restaurant level margins decreased 110bps in 1Q13, primarily driven by higher food and occupancy costs. During the first quarter, CMG was able to leverage G&A by 160bps in order to drive operating margins higher by 60bps to 16.5%. Management noted that 1Q12 included a one-time cost of $5.6 million for long-term incentive performance shares that were issued in 2010. We believe Chipotle is likely to see a more significant decline in operating margins in 2Q13. We expect to see a 2bps and 140bps decline in restaurant and operating margins, respectively.

HEDGEYE – We expect that CMG’s margin trends in 2Q13 will look slightly worse than in 1Q13. We believe that an increase in food costs and other operating expenses will drive restaurant level margins down 160bps versus 103bps in 1Q13. With little G&A leverage, we could see operating margins decline by 142bps.

FOOD COST TRENDS

Food costs were 32.9% in 1Q13, up 72bps year-over-year, due to inflation in salsas, produce, chicken and dairy. However, food costs were down 53bps sequentially from 4Q12, primarily driven by lower avocado and dairy costs.

Looking at 2Q13, we expect food costs to be relatively stable and remain around 33%. The company is at risk for an increase in beef prices and seasonally higher avocado costs. Currently, CMG is seeing inflation around 3-5%; if that accelerates from here, we would expect to see the company raise prices.

HEDGEYE – Chipotle is lapping against an 85bps decline in 2Q12 food costs. At 33%, food costs seem quite reasonable, however, we believe there is an upward bias to this number. Food cost trends remain a wild card for CMG.

LABOR COST TRENDS

Labor costs declined 10bps to 23.6% in 1Q13, driven by higher sales volumes (higher menu prices) and efficiencies. The company typically believes it can leverage its labor costs when generating 3% same-store sales. The street is modeling labor costs of 23.1% for 2Q13, down 0.05% year-over-year.

HEDGEYE – With the street modeling 3.8% same-store sales growth, there is little confidence that management will be able to leverage labor costs. We believe there is room for an upside surprise to labor costs this quarter.

OTHER OPERATING TRENDS

Other operating expenses were 17.1% in 1Q13, up 45bps year over year. In 2Q13, other restaurant expenses are expected to be 16.4%, or down 71bps sequentially. Management has indicated that CMG ramped up their marketing expenses significantly in 2Q13, up to 2% in 2Q13 versus 0.7% in 1Q13.

HEDGEYE – We believe the increase in marketing expenses should help drive incremental traffic during 2Q13.