TODAY’S S&P 500 SET-UP – July 15, 2013

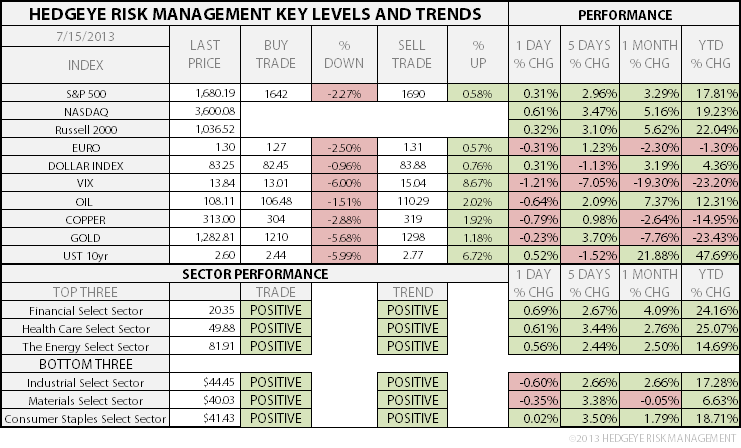

As we look at today's setup for the S&P 500, the range is 48 points or 2.27% downside to 1642 and 0.58% upside to 1690.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.25 from 2.24

- VIX closed at 13.84 1 day percent change of -1.21%

MACRO DATA POINTS (Bloomberg Estimates):

- 8am: Fed’s Tarullo speaks on banking regulation in D.C.

- 8:30am: Empire Manufacturing, July, est. 5 (prior 7.84)

- 8:30am: Advance Retail Sales, June, est. 0.7% (prior 0.6%)

- 10am: Business Inventories, May, est. 0.2% (prior 0.3%)

- 11am: Fed to purchase $750m-$1b in 2023-2031 sector

- 11:30am: U.S. to sell $30b 3M bills, $25b 6M bills

- U.S. Weekly Rates Agenda

GOVERNMENT:

- Fed Governor Tarullo speaks on Dodd-Frank law’s implementation, Basel III rules and possible further measures to bolster requirements for largest U.S. banks, 8am

- House will likely vote this week on bill that would let states implement minimum federal standards for disposing coal ash generated by power plants, giving EPA a secondary regulatory role

- Senate Homeland Security and Governmental Affairs Cmte holds hearing on “Strategic Sourcing: Leveraging the Government’s Buying Power to Save Billions,” 3pm

- FHFA deadline for comments on proposed rule on Golden Parachute and Indemnification payments

- President George W. Bush, with his wife Laura Bush, returns to White House for Point of Light award

- Under Secretary for Intl Affairs Lael Brainard will preview meeting of G20 finance ministers, central bank governors in Russia and discuss the U.S.-China Strategic and Economic Dialogue, 4pm

WHAT TO WATCH

- AT&T’s $1.2b Leap deal puts pressure on smaller rivals to pair up

- MB Financial agrees to acquire Taylor Capital for $22/share

- Boeing 787 fire in London unrelated to battery, U.K. says

- China’s economy slowed to up 7.5% in 2Q, matching ests.

- China almost doubles foreign funds’ access to capital markets

- Vivus invites First Manhattan to have 3 nominees join board

- Citigroup, BofA, others report charge-offs, delinquencies

- Microsoft cuts Surface tablet prices by as much as 30%

- GE weighs Invensys bid after Schneider offer, Times reports

- “Despicable Me 2” edges out Sandler comedy in weekend

- Goldman’s Fabrice Tourre set to face SEC fraud trial today

- Health-care spending in U.S. seen as starting to flatten: WSJ

- U.S. Weekly Agendas: Finance, Industrials, Energy, Health, Consumer, Tech, Media/Ent, Real Estate, Transports

- North American M&A Agenda

- Canada Weekly Agendas: Energy, Mining

- Retail sales probably climbed: U.S. Economy Weekly Preview

- Bernanke, G-20, Dell, China GDP, Google: Wk Ahead July 13-20

EARNINGS:

- Citigroup (C) 8am, $1.18 - Preview

- JB Hunt Transport (JBHT) 4pm, $0.74

- Brown & Brown (BRO) 4:15pm, $0.35

- Healthcare Services (HCSG) 4:15pm, $0.19

- Cintas (CTAS) 4:15pm, $0.70

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- WTI Crude Falls After Third Weekly Gain as Chinese Growth Slows

- Hedge Funds Bought Gold in Biggest Rally Since 2011: Commodities

- Refined Palm Imports by India Seen at Record High on Lower Taxes

- Gold Is Little Changed After Best Week Since 2011 on Stimulus

- Copper Falls as Weakening Chinese Economy Fuels Demand Concern

- Corn Extends July’s Biggest Slump on Improving Outlook in U.S.

- Cocoa Rebounds After European Processing Data; Coffee Retreats

- China June Crude Steel Output Falls to Four-Month Low on Prices

- Shale Skeptics Take On Pickens as Gas Fuels Policies: Energy

- Zinc 15% Capacity Loss Has Miners Struggling to Fill Supply Gap

- Crude Bets Jump to Two-Year High as Demand Soars: Energy Markets

- Citigroup Says Not Yet Time for ‘Bottom-Fishing’ in Commodities

- Milk Price War Pits California Dairy Farms Against Cheesemakers

- Palm Oil Drops to Two-Month Low as Chinese Demand Seen Falling

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team