This note was originally published July 11, 2013 at 10:35 in Macro

The Data & The Divergence

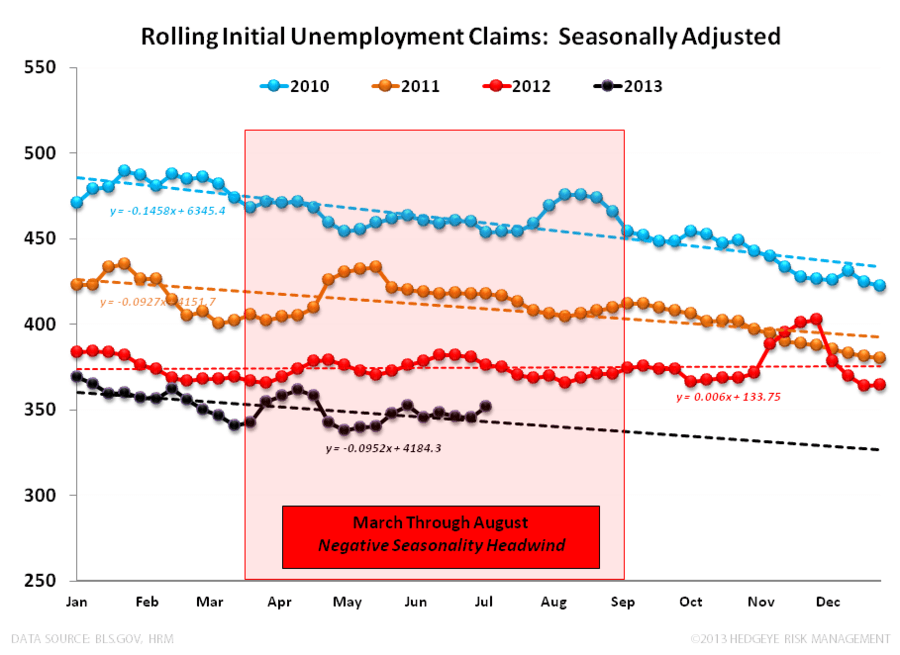

Seasonally Adjusted Claims: Headline seasonally-adjusted claims increased +17K to 360K from 343k (unrevised) the prior week with the the 4-week rolling average increasing 6K WoW to 352K.

Non-Seasonally Adjusted Claims: The 4-week rolling average of NSA claims, which we consider the more accurate reflection of underlying labor market trends, was down -9.8% YoY, a 30bps improvement vs -9.5% the prior week.

We would highlight that claims data for the week containing the July 4th holiday presents a challenge from a seasonal adjustment perspective and complicates an attempt at discerning any incremental change in the direction of labor trends. Additionally, autocompanies keeping plants open instead of implementing typical July production shutdowns this year (first time since 2008) further complicates a clean interpretation of this weeks data.

All in, the divergence between the seasonally adjusted and non-seasonally adjusted data continues to widen with the seasonal distortion driving an optical deterioration in the reported headline number while the underlying (ie. real) labor market trend remains one of accelerating improvement. In short, the TREND (inclusive of today’s data) in the labor market remains one of strength and, given the existent July 4th holiday and autoworker dynamics, we wouldn’t read too much into this or next week’s claims data in isolation.

Christian B. Drake

Senior Analyst