Earnings season for the big cap gaming operators has something for everyone.

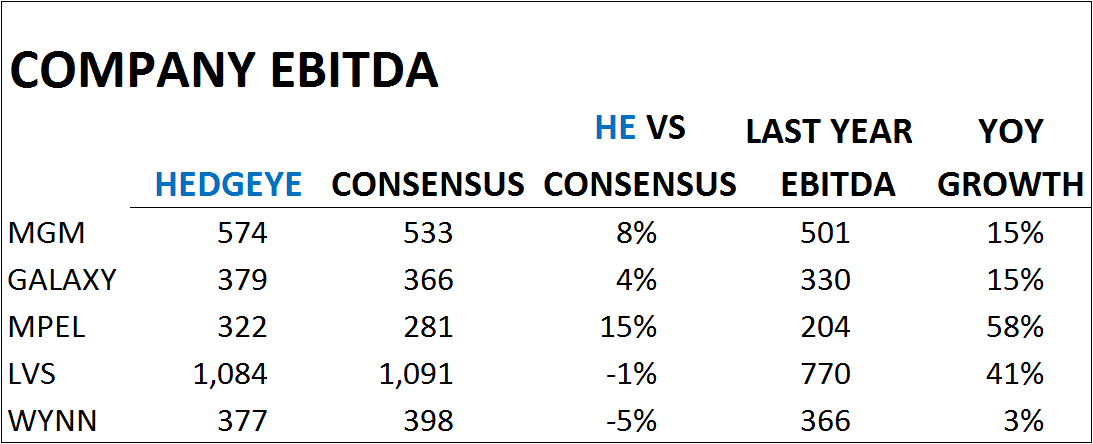

Despite the panic surrounding the China economy right now, Macau fundamentals look healthy. The health should be on display, generally, during the upcoming Q2 earnings season. We’re projecting beats for the most part and positive commentary regarding Q3 in Macau. As the chart shows, MPEL looks like the big winner in that market vs consensus followed by MGM Macau.

Not surprisingly, MPEL and MGM are our favorite gaming stocks. Both companies are projected to handily beat consensus company EBITDA estimates. We have Galaxy beating as well but WYNN could be a disappointment.

MPEL

With 100% exposure to Macau and a higher than normal VIP hold percentage, MPEL should knock the cover off the ball when they report Q2. Even on a hold adjusted basis, MPEL would handily best consensus expectations. We’re projecting $300-305 million in adjusted company EBITDA after normalizing the high VIP hold at both City of Dreams and Altira. Assuming normal hold in both periods, MPEL should grow its EBITDA around 50% YoY in Q2. And this management team deserves a huge valuation discount to the group? We think not!

MGM

May Las Vegas numbers should come out today and we think the Strip will be a blowout – up mid-teens on a hold-adjusted basis. We have MGM beating in Macau by a wide margin as seen in the chart above. More surprisingly, we actually think they will beat in Las Vegas as well ($324 million vs the Street at $297 million). A comprehensive beat and positive commentary about Q3 should be the fundamental fuel to boost this stock through the technical resistance of $16. Then to the moon, Alice!

LVS

LVS looks good in general, although we think the Street has caught up to a strong quarter. We’re slightly ahead in Macau and slightly below in Las Vegas. An in-line quarter is probably not good enough but the company’s intermediate and long-term prospects are so bright, it’s hard to be negative. Look for buying opportunities here.

WYNN

We’re estimating a 5% miss in company EBITDA, driven almost exclusively by Macau. Wynn Macau posted a disappointing quarter despite overall market strength. Hold was slightly below normal but volumes were also disappointing. We’ve got flat VIP volumes and Mass revenues up only 7% vs the market at +18% and +31%, respectively. Wynn Macau should continue to lag the market and a potential earnings miss and a delay in the opening of Wynn Cotai could weigh on the stock.

GALAXY

Another Macau pure play (for the most part) that should exceed estimates, although not to the extent of MPEL and MGM, Galaxy looks attractive. The stock trades at a discount to the peer group and retains the nearest new build catalyst. The Galaxy Macau expansion should open in early 2015, a full year before Wynn Macau, MPEL’s Macau Studio City, or LVS’s Parisian may open. For Q2, Galaxy held a little high at its two properties but volumes were strong. Q2 should be a clean beat.