This note was originally published July 09, 2013 at 15:07 in Macro

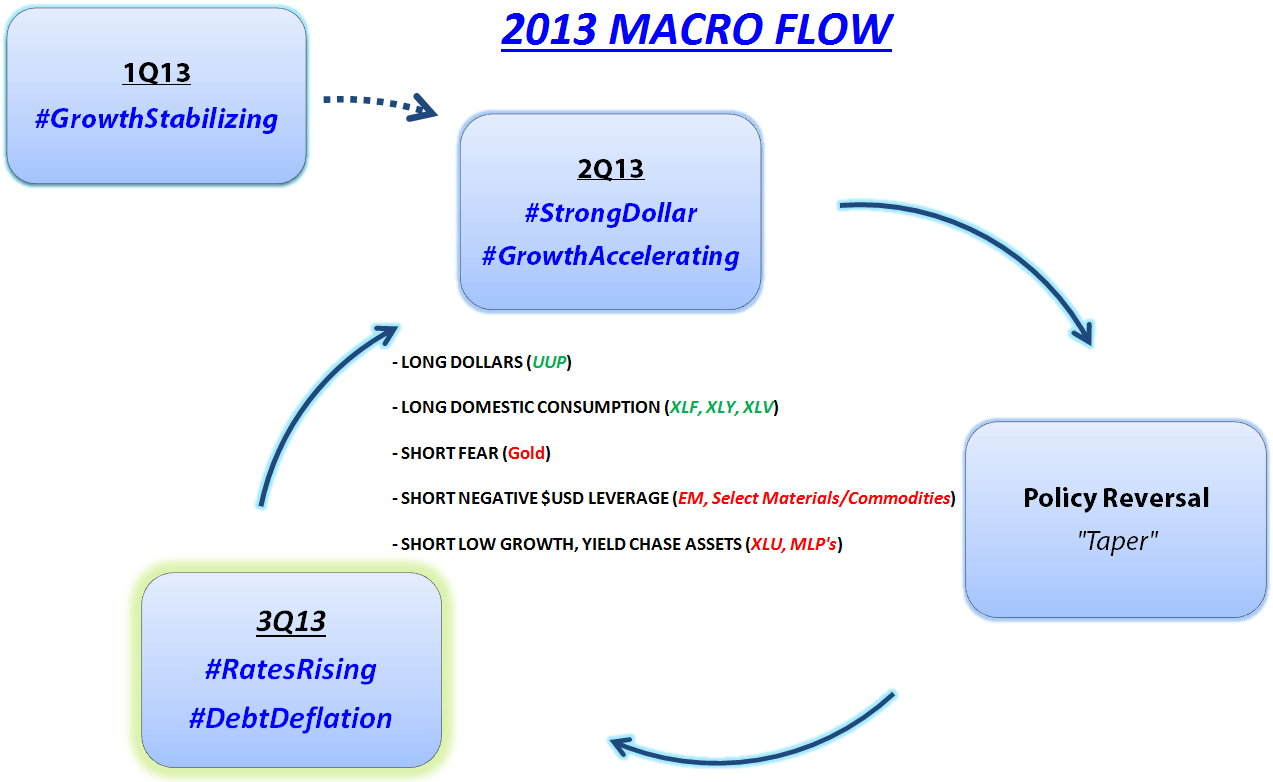

We’ll introduce our detailed view on #RatesRising and the cross-asset class implications of the reversal in the 30Y bull cycle in bonds on our 3Q13 Macro Themes call next Tuesday July 15th.

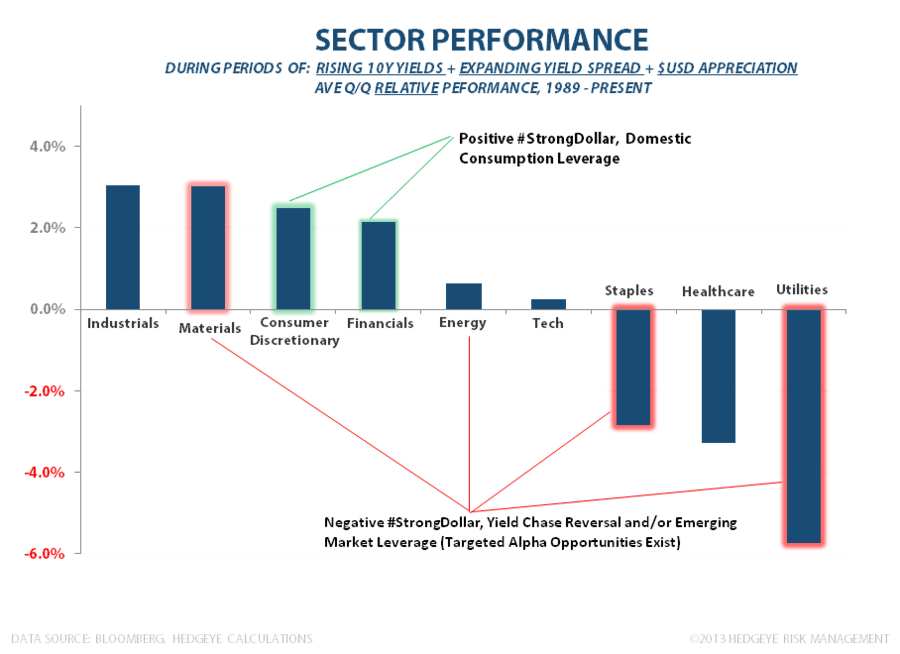

As a visual preview and for some historical context, the sector study below shows the average, relative Q/Q sector performance during periods in which the factor combination of: Rising 10Y Yields, Expanding Yield Spread, and $USD appreciation all prevailed. At n=7, the sample population isn’t overly large but we’d still view the output as instructive.

General underperformance in defensives and outperformance in cyclicals isn’t particularly surprising. Additionally, we’d note that given the policy catalyzed, positive relative performance in yield chase assets, the downside for sectors such as Utilities and Staples is likely larger than historical precedent would suggest.

Further, in the context of our #StrongDollar and Bearish China/Emerging Markets view, the relative performance risk for Materials and select Energy & Industrials is likely to the downside vs the historical mean.

In short, alongside continued TREND improvement in domestic Labor Market, Housing, Confidence and Credit metrics, we’re viewing the back-up in Treasury rates and expansion in the yield spread as a pro-growth signals.

In terms of positioning, the 1H13 playbook remains largely in-tact with Consumer Discretionary and Financials the best way to find positive $USD and domestic consumption leverage at the sector level. While equities are immediate-term overbought here (see today’s note: Overbought: SP500 Levels, Refreshed) we continue to like the absolute and relative growth setup for the U.S. and pro-growth oriented asset exposures.

Christian B. Drake

Senior Analyst