This note was originally published at 8am on June 26, 2013 for Hedgeye subscribers.

“Nothing is certain but the unforeseen.”

-J.A. Froude

No stranger to intellectual debate, British author James Anthony Froude (1818-1894) was well-known for stirring the pot – perhaps even more so than @HedgeyeDJ (Daryl Jones, our no-holds-barred DoR) and @HedgeyeENERGY (Kevin Kaiser, our oft-controversial senior energy analyst).

Froude’s generally polemic works were often met with fierce debate and rejection among the British intellectual elite – perhaps none more so than his seminal work The Nemesis of Faith (1849), which was carefully crafted to call into question blind acceptance of the popular Christian doctrine of the time. Widespread public backlash in response to the novel ultimately cost Froude his fellowship at Oxford University.

Eventually Froude’s avoidance of institutionalized groupthink won out. Froude and his wildly contentious ideas ultimately found a permanent home when he was appointed Regius Professor of Modern History at Oxford (i.e. a really big deal) in 1892 – the very institution he was driven away from nearly a half-century prior. During his regrettably brief stint at Oxford (he died in 1894), Froude quickly earned a reputation for being among the most popular lecturers of his time.

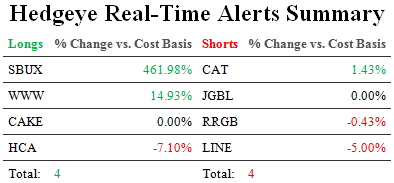

If nothing else, Froude’s journey from the top to the bottom and back again is a lesson for analysts young and old to avoid the safety and comfort of groupthink. Never is this advice more important than when a time-tested, comprehensive and repeatable research process leads one to hold a counter-consensus view. Hold the LINE [short], Kaiser!

Back to the Global Macro Grind…

Incorporating another one of Froude’s lessons, we call attention to the aforementioned quote in the context of China’s banking system woes – which, thanks to the recent spate of legacy media coverage, are now as obviously present as a 6’3”, 325lb left tackle in one of Froude’s 19th century lectures.

Specifically, anyone even tangentially following recent press will arrive at the conclusion that a growing consensus among analysts across both the buy and sell sides believes with a fair amount of certainty that China’s credit binge and alleged housing bubble are sure to cause a Western-style financial crisis.

We aren’t so sure. With less than 2% of all financial assets held by foreigners, strict capital controls have, thus far, prevented a mass exodus of liquidity through the capital account. Domestically speaking, the PBoC’s own words from yesterday should douse any hopes of a crisis:

“Financial institutions’ cash reserves stood at about 1.5 trillion yuan ($244 billion) as of June 21, compared with the 600 billion yuan or 700 billion yuan sufficient under normal circumstances to cover payment and clearing needs. The present liquidity is not insufficient.”

Indeed, by comparing China’s present-day banking woes to the early tremors of Bears Sterns or juxtaposing China’s property market – rife with “ghost cities” – with our own pre-crisis froth, consensus has undeniably fallen victim to the availability heuristic. We don’t think that’s a prudent call to make at the current juncture; the Chinese sovereign has the resources, political will and mobility to prevent any Western-style financial crisis.

We’ve become a broken record on this, but it’s critical to remember that China’s present day economic woes are actually a function of very deliberate macroprudential policies. While highly unlikely, at any given time, Chinese officials can reverse course and keep the credit bubble inflating longer than any of us short-sellers can remain solvent.

On the contrary [to consensus], we think the outlook for China’s banking sector is likely to resemble that of a slow bleed, rather than sudden cardiac death. We’ve published a ton of work recently backing our conclusions with detailed analyses, but for those of you who weren’t able to tune in until now, we’ll take this opportunity to rehash our views:

- In the face of slowing deposit growth, the confluence of rising NPLs and/or the perpetual debt rollovers of SOE borrowers on top of balance sheets clogged with long-term assets that are held to maturity is something that should remain a sustainable headwind to the abundance of liquidity across the Chinese financial system.

- From a deposit growth perspective, it’s rather unlikely that Chinese households save more at the margins – especially in the context of the Communist Party’s economic rebalancing agenda. Moreover, structural headwinds to export growth (CNY overvaluation, sluggish growth in China’s #1 export market (i.e. the EU) and SAFE’s regulatory crackdown on “fexports”) should continue to limit inflows of new external capital into the Chinese economy as well.

- All things considered, we expect credit growth to slow sharply from recent levels and remain sustainably slower for the foreseeable future. We expect that outcome to weigh on observed rates of economic growth and future growth expectations, which should reflexively perpetuate greater [unreported] NPL exposures.

- By layering on the structural NIM-compression that will be the [highly] likely result of interest rate liberalization – which the PBoC recently affirmed they are forging ahead with – we have formulated a potent three-pronged bearish thesis for Chinese financials and property developer stocks.

- As such, we anticipate a long-lasting drag on both earnings growth (not as important for Chinese equity valuations) and sentiment (very important to Chinese equity valuations) over the long-term TAIL. Equity capital raises from the banking sector and broad-based capital outflows – assuming capital account liberalization goes as planned – are not at all improbable scenarios.

- From an immediate-term TRADE perspective, however, we do think China’s cyclical banking system woes are reasonably priced in. As such, we actually expect to see some form of a relief rally at some point over the immediate-term, driven by speculators following through on yesterday’s soft backstop out of the PBoC and what may morph into USD-debauching, anti-tapering headlines out of the Federal Reserve with the UST 10Y yield showing increasing signs of convexity of late.

- We are however, inclined to fade any such strength in the event the SHCOMP approaches its immediate-term TRADE line of resistance up at 2,123. With Chinese stocks nearing full-on crash mode since their late-MAY highs, that line is approximately +8.8% higher from today’s closing price, which, for the second consecutive day, took out the near-4Y lows established last DEC.

- Alas, it remains our view that the headwinds facing China’s banking system are structural (i.e. NOT cyclical) in nature.

Please email us if you’re interested in reviewing the full compendium presentation materials and research notes backing these conclusions, and we’ll get them right over to you. We also have a list of ancillary securities and asset classes to underweight/sell/short if you’re interested in those as well.

At any rate, we urge you to embrace the uncertainty of this situation by running full speed away from anyone who tells you they know how this all ends.

In fact, the only certainly anyone can promise you regarding these risks is that the outcome is presently unforeseen and, quite possibly, hidden deep within the “shadows” of China’s financial sector.

Our immediate-term TRADE Risk Ranges are now (TREND bullish or bearish in brackets):

UST 10yr Yield 2.35-2.69% (bullish)

SPX 1560-1614 (bearish)

DAX 7619-8108 (bearish)

Nikkei 12,406-13,449 (bearish)

VIX 16.59-20.98 (bullish)

USD 82.21-83.39 (bullish)

Euro 1.30-1.32 (neutral)

Yen 96.25-99.17 (bearish)

Oil 99.18-103.39 (bearish)

NatGas 3.64-3.82 (bearish)

Gold 1226-1324 (bearish)

Copper 2.98-3.12 (bearish)

Keep your head on a swivel,

DD

Darius Dale

Senior Analyst