Finding a bottom is not the same thing as recovering.

RESEARCH EDGE POSITION: Short Japan via the EWJ etf...

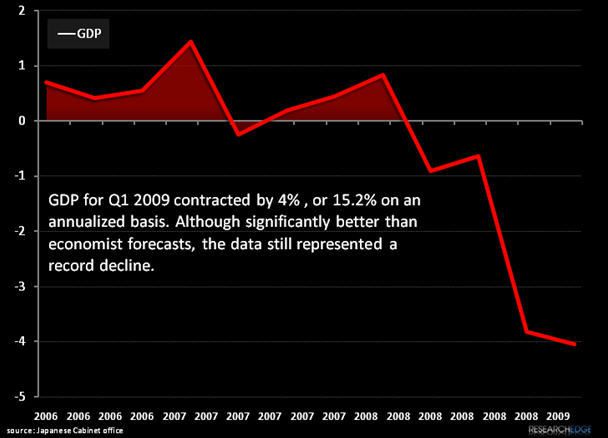

Japanese GDP data released overnight was very ugly and very anticlimactic. Q1 GDP numbers released by the cabinet office registered at an all time low, with a period decline of -4%, or -15.2% on an annualized basis. With the complete collapse of the North American export market in the trailing 5 quarters, this contraction was a foregone conclusion for most observers (in fact the number was a significantly better than most reported forecasts). The Nikkei traded up on Yen declines driven in part by the data.

If you have read our work on Japan in the past, you know that we view the Land of the Rising Sun as something of a Ponzi Economy -with a population maintaining very high savings rate whose nest eggs allow the government to borrow at ultra low interest levels in order to execute stimulus programs designed to encourage people to save less. This cycle of internal public debt accumulation (now hovering at close to 200% of GDP) is anchored to a vicious demographic curve that leaves the Japanese economy in the long-term position of a man treading water with a bowling ball in his hands.

Tactically, we trade Japanese equities in reaction to currency moves as Yen devaluation is the only short term positive catalyst there that we have identified. For us to change our longer term view on the Japanese economy, we would need to see clear evidence that the US and EU markets are rebounding to prior consumption levels (unlikely) or that new export lines are being developed and exploited in emerging Asian consumer markets -particularly China.

As the Japanese economy scrapes bottom and the governing parties scramble impotently to find solutions, the mood of the public has proven remarkably resilient. Consumer confidence levels in April registering at the fourth consecutive sequential improvement. Perhaps Japanese consumers have become accustomed to stagnation. We'll short complacency in the face of misunderstood Japanese tail risk.

Andrew Barber

Director