The Antichrists of Growth (Gold, Treasuries, Utilities, etc) are still underperforming.

Just to give you an idea: Utilities (XLU) are down 0.5% on the month, whereas pro-growth Consumer Discretionary (XLY) is up 3.4%. A not-so-subtle 400-basis point divergence there.

Pro-growth Financials (XLF) are up 2.67% July-to-date. Gold? Hell on earth, scorched over 25% YTD.

As for Bill Gross, his 10-Year Treasury is down about 6% in the last three months; the S&P 500 is up over 5%.

Last but not least. The Russell 2000 is breaking out to new all-time highs, notching its second consecutive record high in as many days. It’s up 19% YTD. Many would acknowledge that the Russell 2000 breaking out is probably a pro-growth signal.

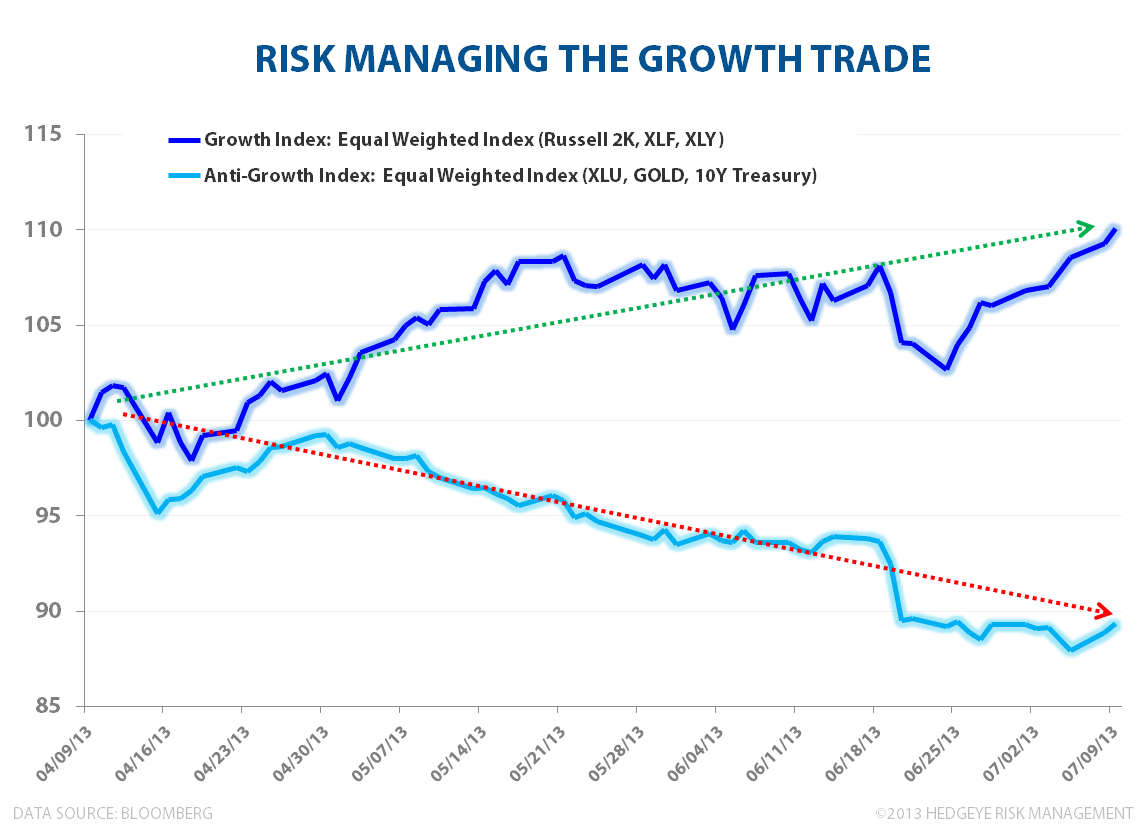

Here's another way of looking at it.

In other words, growth is getting paid.

(This is an excerpt from Hedgeye Risk Management CEO Keith McCullough's morning call. If you would like more information on our services and how Hedgeye can help you please click here.)