WWW's 2Q print was spot-on with what we needed to see to remain confident in our call that this is a $100 stock over 2-years. We think that the revenue hammer is cocked to add $1bn in sales over three years. This is accentuated by the margin story that reared its head meaningfully in 2Q and will get return on capital moving in the right direction after a 2-year decline.

One thing that became abundantly clear to us in listening to the conference call is how bifurcated the perception is on this name. We all know that Wall Street is naturally short-sighted, but easily 80% of the time on this marathon 80-minute call was allocated to near-term puts and takes that have no real bearing on what we think is relevant to the appropriate money-making thesis.

There were two factors in particular that were a big focus (and shouldn’t be). 1) The lack of guidance, and 2) Commentary around accretion of the PLG brands.

- WWW bowed out of the quarterly earnings game, and simply reaffirmed an annual revenue range while upping annual EPS guidance by a dime after a $0.13 EPS beat Q2. Combined with unidentified/unauditable expenses that were supposedly pushed out, and unquantified revenue that was pulled forward, WWW succeeded in spooking the Street into keeping back half estimates low. We're at $2.86 vs. a consensus range for the year between $2.60-$2.75.

- PLG Accretion. Here's one where we've got to call a spade a spade. Either the company's forecast accuracy as it relates to acquisition accretion is simply horrendous, or they've artfully sandbagged the Street's expectations on a consistent basis. Consider the progression of expected accretion/dilution vs. actual results. Going into the year, WWW guided to Modest Accretion in 1Q, Slight Dilution in 2Q, and $0.35-$0.50 per share in accretion for the year. It ended up earning $0.34ps and $0.24ps in 1Q and 2Q, respectively, from PLG, or $0.58 combined. Now, even though at the beginning of the year it called for accretion in both 3Q and 4Q, it is taking down expectations for zero back half accretion. Perhaps we'll fall victim to thinking there's a sandbag when one does not exist, but given the momentum of Sperry and Keds, we find it very difficult to get to a loss in 2H.

The near-term factor that mattered most, in our opinion, was the fact that the Performance division went from +8% in 1Q to -4.8% in 2Q. Simply put, Merrell, WWW's largest division, tanked. We can talk all day about how a product like M-Connect is up double digits, but the reality is that Merrell has a huge division called Outdoor Lifestyle that sells the non-performance product in the portfolio. We think that it was ignored immediately following the PLG acquisition, which is less than optimal given that it accounts for about 40% of the Merrell portfolio. The good news is that the company made organizational changes over the past 3-6 months, and the order backlog for the brand in aggregate turned up to the point where management noted that it can grow low single digits for the year. We have no reason to believe that they're lying about order levels, and the channel is lean enough that we don't forsee outsized cancellation levels. In other words, we're going to give them the benefit of the doubt on this one.

Even better is that the full benefit of the Merrell reorganization will be seen at the beginning of 2014, which is also when we start to see a greater impact from the company scaling Sperry and Keds over the existing International infrastructure. From a timing perspective, this is when we think people will really start to realize that WWW is much growthier than they otherwise think.

OUR THESIS

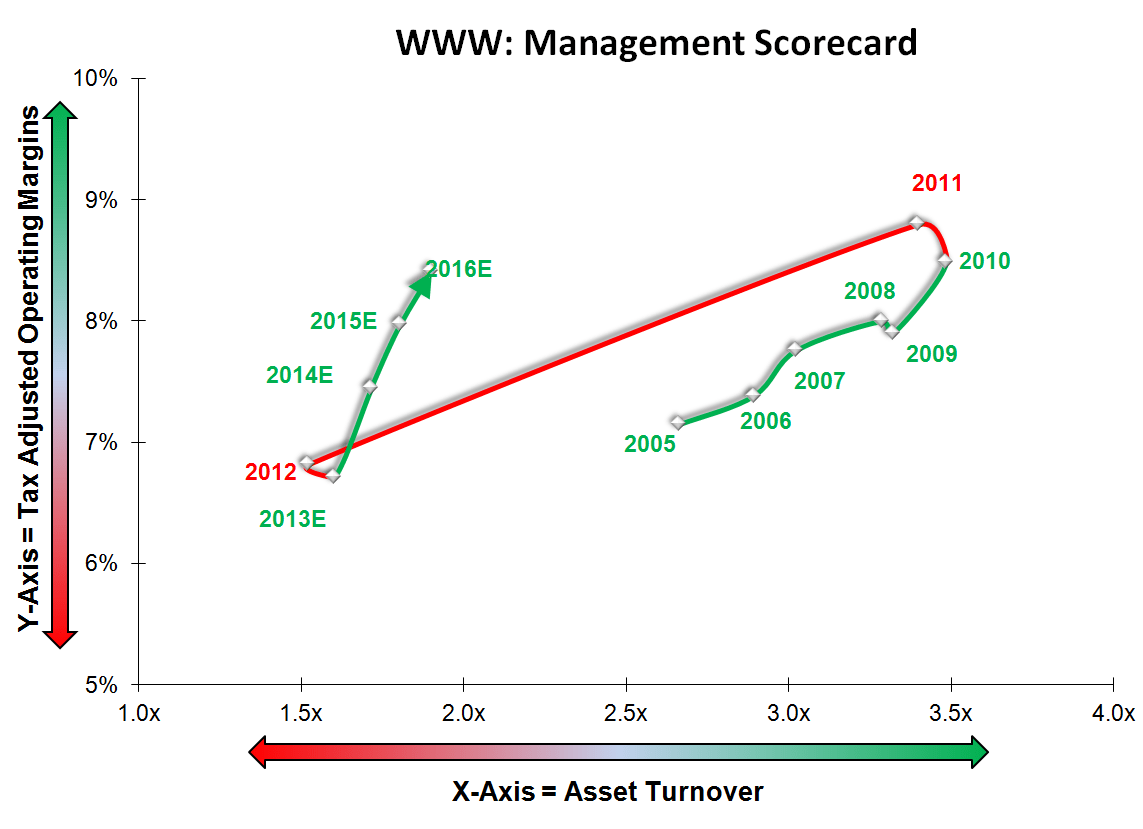

The Street is grossly underestimating the revenue growth opportunity as the legacy WWW scales its recently acquired brands over its global infrastructure. We think WWW can and will add $1bn in sales to its $2.7bn base over 3-years. Under its former owner, Sperry, Keds, Saucony and Stride-Rite only generated 5% of its sales outside of the US, and most of that was in Mexico and Canada. Legacy WWW, on the other hand, is the most global footwear company in the world (yes, even more so than NKE and AdiBok), with 65% of units sold outside the US through an elaborate network of seamlessly-integrated third-party distributors. Given that the infrastructure is already in place, the incremental sales should be brought on close to a 20% incremental margin, versus 8% margin today. Similarly, minimal capital is needed on the balance sheet to grow these brands, making the growth trajectory over the next 3-5 years very ROIC accretive. The stock might look expensive at 20x earnings and 12x cash flow, but the street’s numbers are low by an incremental 10% per year. We're at $5.75 to the Street's $4.25 three years out. We’d buy aggressively on a pullback, but are not so sure that will happen. We think WWW is a double over 2-3 years.

WWW PROFITABILLITY ROADMAP (Components of RNOA)