TODAY’S S&P 500 SET-UP – July 9, 2013

As we look at today's setup for the S&P 500, the range is 31 points or 1.31% downside to 1619 and 0.58% upside to 1650.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.29 from 2.28

- VIX closed at 14.78 1 day percent change of -0.74%

MACRO DATA POINTS (Bloomberg Estimates):

- 7:30am: NFIB Small Bus. Optim, June, est. 94.6 (prior 94.4)

- 7:45am/8:55am: ICSC/Redbook weekly retail sales

- 10am: JOLTs Job Openings, May, est. 3790k (prior 3757)

- 11am: Fed to buy $2.75b-$3.5b notes in 8/15/2020-5/15/2023

- 11:30am: U.S. to sell 4wk bills

- 12pm: DoE Short-Term Energy Outlook

- 1pm: U.S. to sell $32b 3Y notes

- 4:30pm: API crude, oil product inventories

GOVERNMENT:

- House Financial Svcs panel holds hearing with CFPB Acting Deputy Director Steven Antonakes on how CFPB collects and uses of consumer data, 10am

- FDIC board meets to consider interim final regulatory capital rules including those needed for implementation of Basel III intl banking accords, 10am

- House Financial Svcs panel holds hearing on Dodd-Frank Act, with witnesses including lawyer Boyden Gray, 2pm

- House Energy and Commerce panel meets on “Cyber Espionage and the Theft of U.S. Intellectual Property and Technology,” with CSIS’s Jim Lewis testifying, 10:15am

- NTSB holds first of two investigative hearings on 2012 New Jersey train derailment, haz-mat release, 9am

WHAT TO WATCH

- FDIC meets to vote on final capital rules of Basel III

- Glass Lewis backs Michael Dell $13.65-shr buyout offer

- BlackBerry to hold annual shareholder meeting

- China inflation stays below target; PPI falls 2.7%

- CFTC weighs delay of swaps rules, WSJ says

- U.S. apartment vacancies unchanged in 2Q, Reis says

- DirectTV, Time Warner Cable meet deadline to bid on Hulu

- Alcoa 2Q EPS, rev. beat; reaffirms 2013 aluminum outlook

- Barnes & Noble edges closer to breakup as CEO quits

- Shell names Van Beurden to succeed Voser as CEO

- U.K. manufacturing unexpectedly falls in May

- Greece wins release of $3.9b in aid from Europe

EARNINGS:

- Wolverine World Wide (WWW) 6:30am, $0.34

- Jean Coutu Group (PJC/A CN) 7am, C$0.26

- Alimentation Couche-Tard (ATD CN) 11:45am, $0.77

- Helen of Troy (HELE) After-mkt, $0.70

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

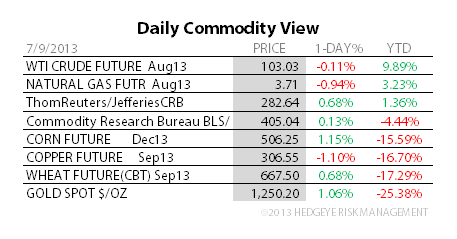

- Commodity Traders’ Buildup on Easy Money Seen as Risk in Report

- Gold Bulls Defy Price Slump as Paulson Loss Widens: Commodities

- Copper Falls as Slumping Chinese Prices Reflect Slowing Economy

- Russian Grain Harvest Seen Below Government Target After Drought

- Gold Gains to One-Week High on China Inflation, Physical Demand

- WTI Crude Trades Near 14-Month High Before U.S. Inventory Data

- Coffee Reaches One-Month High on Supply-Curb Signal; Cocoa Gains

- Gold-Dollar Deviation Signaling Shift of Faith: Chart of the Day

- Hedge Fund Crude Oil Bets Jump Amid Egypt Strife: Energy Markets

- Rebar Erases Gains to Decline as Overcapacity Damps Sentiment

- Libya Oil Output Slides as Power Cuts Mix With Protests: Energy

- Tanker Demolitions Slumping as Rupee Reaches Record Low: Freight

- Quebec Explosion Exposes Risks of Rising Urban Oil Shipments

- China’s Wheat Imports Seen Higher Than USDA Forecast After Rains

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team