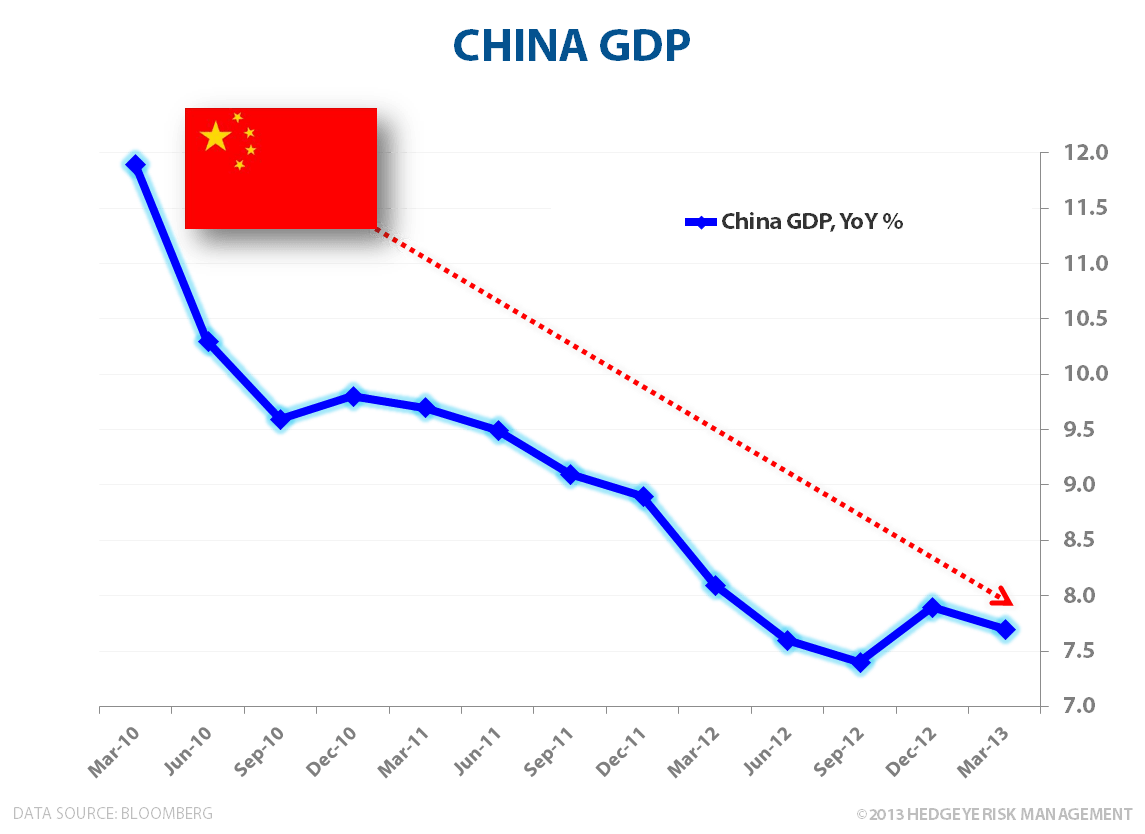

We still don’t like China. We’ve been clear on that. What’s going on there isn’t good.

Despite US equities rallying last week and into the close on Friday, Chinese equities were down another 2.4% overnight and are down 12% for the year. The Hang Seng also failed to bounce, down another 1.3% after failing at its immediate term TRADE line resistance. Indonesia was down 3.2%; Thailand down 2.4%. The only market above its TREND line in all of Asia is Japan. There are some big bad moves going on over in Asia.

So, is Asian growth slowing? Yes, that’s already happening.

Looking more closely at China, the Politburo (via President Xi), the PBoC (via Governor Zhou) and the State Council all came out at varying times last week and talked down market expectations for GDP growth and credit expansion going forward. With Manufacturing PMI hitting a 4-month low and Services PMI hitting a 9-month low in June, this does not bode well for China’s TREND duration growth outlook.

Meanwhile, Bloomberg reports that President Xi Jinping said officials shouldn't be judged solely on their record in boosting GDP, the latest signal that policymakers are prepared to tolerate slower growth.

More to be revealed.