TODAY’S S&P 500 SET-UP – July 3, 2013

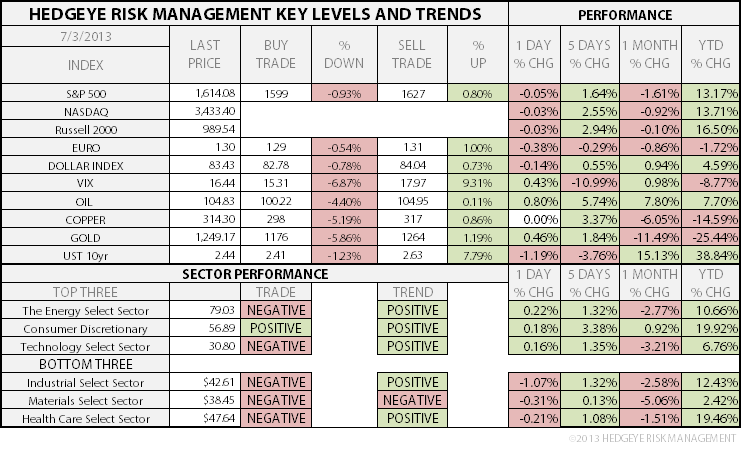

As we look at today's setup for the S&P 500, the range is 28 points or 0.93% downside to 1599 and 0.80% upside to 1627.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.10 from 2.12

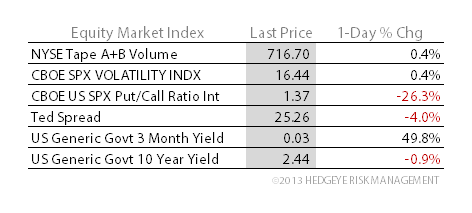

- VIX closed at 16.44 1 day percent change of 0.43%

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: MBA Mortgage Applications, June 28

- 7:30am: Challenger Job Cuts, June (prior -41.2%)

- 7:30am: RBC Consumer Outlook Index, July (prior 51.8)

- 8:15am: ADP Employment Change, June., est. 160k (prior 135k)

- 8:30am: Trade Deficit, May, est. -$40.1b (prior -$40.3b)

- 8:30am: Init Jobless Claims, June 29, est. 345k (prior 346k)

- 8:30am: Cont Claims, June 22, est. 2960k (prior 2965k)

- 9:45am: Bloomberg Consumer Comfort, June 30, prior -28.3

- 10am: ISM Non-Manuf Index, June, est. 54 (prior 53.7)

- 10am: Freddie Mac mortgage rate survey

- 10:30am: DoE weekly inventories

- 11am: Fed to buy $4.75b-$5.75b notes, 4/30/18-3/31/19 range

- Noon: EIA natural gas

- 1pm: Baker Hughes rig count

GOVERNMENT:

- House, Senate not in session

- Treasury Sec. Jack Lew speaks at naturalization ceremony ahead of July 4 natl holiday, 10am

- President Barack Obama returns from trip to Africa

WHAT TO WATCH

- U.S. stock markets mostly closing at 1pm today

- Markets closed tmw for Independence Day holiday

- Prudential is first to challenge Treasury’s risk tag

- Credit Suisse, Deutsche, Barclays ratings cut by S&P

- Biggest U.S. exchanges said to seek delay in regulations

- N.Y. state AG examing Wal-Mart, Home Depot fee system

- Softbank bid for Sprint said to win majority vote at FCC

- Gardner Denver investors say former CEO helped KKR on deal

- Yahoo buys iPhone video app maker Qwiki

- Nasdaq seeking to have Facebook suit dismissed, WSJ says

- US Airways-AMR merger is subject of antitrust lawsuit

- Apple said to near deal with Time Warner Cable

- Fmr. Yves St. Laurent CEO hired by Apple

- Michael Dell said to have not answered request to raise bid

EARNINGS:

- Intl Speedway (ISCA) 7:30am, $0.48

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- WTI Rises Above $100 on Drop in U.S. Stockpiles, Egypt Unrest

- Israel Chemicals Moves Dead Sea Salt for $1 Billion: Commodities

- Copper Gains as Traders Close Bearish Bets Amid Supply Concern

- Wheat Advances for Second Day After Egypt Purchases 180,000 Tons

- China Said to Buy U.S. Wheat With Purchases Seen at 600,000 Tons

- Gold Swings as Investors Weigh Physical Demand Against Stimulus

- Abe’s Third Arrow Seen Striking Tariffs From Pork to Beef

- Cocoa Climbs on Speculation About Crop Delays; Coffee Declines

- Japan Nears Switching on Reactors After Tepco’s Meltdown: Energy

- Paris Wheat Futures Seen Extending Decline: Technical Analysis

- Wheat-Less in the Pampas Worsens Dollar Drain: Argentina Credit

- Carbon Plan Wins EU Parliament Backing After Glut Spurs Collapse

- Nickel Inventories Ease Pace of Growth, Still at Highs: BI Chart

- Europe-to-U.S. Gasoline Arbitrage Cargoes Seen Plunging 28%

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team