“If someone picks on your brother and you don’t stand up for him, don’t bother coming home.”

-Larry Bird, quoting his father (paraphrased)

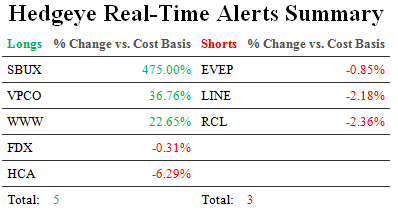

From a stock research perspective, the last couple of months at Hedgeye have been interesting. Specifically, our Senior Energy Analyst Kevin Kaiser has been knees deep in a classic battleground stock: LINN Energy. Kaiser has done an immense amount of independent work on the stock and concluded that the Company is overvalued. In fact, our fair value estimates are more than 40% lower than the current stock price.

This research has raised the ire of the Company’s management who has publicly refuted our thesis, has led to numerous ad hominem attacks from the likes of Jim “The Entertainer” Cramer, and also led to a letter to the editor of Barron’s from a large hedge funds that has accused the short sellers of LINN to be “unprincipled”. (Ironic from a hedge fund that routinely shorts securities.)

Now, admittedly, when we think we are on to something we tend to go all in. In this instance, that included presenting on the idea a couple of times, participating in the Barron’s article, and publicly defending our research and our analyst. To Larry Bird’s quote above, if you are not going to defend your ideas and your teammates, don’t bother coming back to Hedgeye headquarters.

Late last night, we were rewarded for our hard work as LINN Energy announced:

“… that they have been notified by the staff of the Securities and Exchange Commission ("SEC") that its Fort Worth Regional Office has commenced a private, non-public inquiry regarding LINN and LinnCo. The SEC has requested the preservation of documents and communications that are potentially relevant to, among other things, LinnCo's proposed merger with Berry Petroleum Company, and LINN and LinnCo's use of non-GAAP financial measures and hedging strategy.”

Now to be fair, this is America, and certainly the Company is innocent until “proven guilty” by the SEC, but nonetheless this was part of our point in warning investors that some of LINN’s practices were likely to attract the scrutiny of the SEC.

As always, though, Mr. Market will ultimately let us know if we are correct in our research on this name. After all, in the short run the stock market is a voting machine and in the long run it’s a weighing machine.

Back to the global macro grind . . .

Not surprisingly, one of our third quarter themes will be related to Asia, which has been home to much of the global equity market pin action this year. As Keith noted this morning, the Yen is down for the fourth straight day versus the U.S. dollar. In that time period, the #WeimarNikkei is up +6.4% and is once again back above our TREND line of support of 13,389.

The other noteworthy equity move in the region was from Australia. In the land down under, Aussie stocks had their largest 1-day move in the last two years, up more than 2.5%.

The Reserve Bank of Australia left rates unchanged and also indicated that they are maintaining an easing bias with a scope to cut again. So, yes in U.S. dollar terms kangaroo pelts are cheap and getting cheaper!

The data flow out of Europe this morning is also universally supportive of more easing from the ECB. First, French car sales came in at literally 20-year lows. Second, Portugal’s Finance Minister resigns due to public discord over austerity. Finally, it seems Greece may not be able to satisfy the Trioka in the next 3 days and concession will have to be reached on its next aid tranche. This later point was obviously foreshadowed by Greek equities which are down -26% since May.

On a relative basis, the actions in both Japan and Australia, and data from Europe, are supportive of our bullish view of the U.S. dollar. Currency trades on marginal moves in policy and, on the margin, the U.S. appears to be getting more hawkish as the rest of the world stays or gets more dovish. Of course, as the facts change so will we and this is a big week for incremental data with U.S. payrolls being reported on Friday and the ECB meeting on Thursday.

Coming into the year, one of the asset classes we were most negative on was gold. Primarily, this was due to expected U.S. dollar strength. This thesis has played out in spades with gold down more than -25% in the year-to-date. Currently, we have no position in gold, but continue to look for a re-entry point on the short side. Consensus is still trying to call the bottom, but the reality remains that prolonged strength in the U.S. dollar will be a major headwind for gold.

Switching gears to the U.S., we will be hosting a call next week on July 9th to introduce a new investment theme on defense spending entitled, “Torpedoes in the Water?” In summary, we are introducing a bearish view on many defense contractors, which have been outperforming industrials broadly, as we believe the earnings estimates are likely to go lower as a long term reduction in procurement spending sets in. Email if you’d like to attend.

Our immediate-term Risk Ranges are now:

SPX 1

Nikkei 131

USD 82.46-84.16

Yen 98.02-99.91

Oil 102.26-104.86

Gold 1174-1268

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research