We are adding short Breitburn Energy Partners (BBEP, $18.42/unit, $1.8B market cap) to our "Best Ideas" list.

Breitburn Energy Partners (BBEP) is LINN Energy junior. Perhaps the CFO’s have been comparing notes, because BBEP plays many of the same accounting games that LINN does with the intention of giving undue benefit to non-GAAP financial measures - adjusted EBITDA and distributable cash flow (DCF). We imagine that BBEP’s management team doesn't feel too good this morning reading about the SEC's informal investigation into LINN's use of non-GAAP financial measures and hedging strategy... We continue to be amazed by what we are finding in this upstream MLP sector. Analysts and investors have been either asleep at the wheel or willfully blind, allowing these companies to get away with egregious accounting practices that inflate non-GAAP financial measures far beyond the economic reality of the underlying business and assets. As is the case with LINN Energy, we believe that BBEP’s distribution is largely a mirage, funded with capital raises that are disguised with a variety of creative accounting schemes. We believe fair value for BBEP is between $2 - $8 /unit, ~70% below the current unit price.

There’s a lot not to like. Here are the key issues we've identified so far:

- Non-GAAP financial measures far from economic reality (actual EBITDA, net income, free cash flow);

- Derivatives accounting methodology (realized gain = cash settlement);

- History of manipulating the hedge book (terminating contracts early);

- Acquisition of in-the-money derivatives, the cost of which is not deducted from DCF;

- Inappropriate adjustments to non-GAAP measures (unit-based compensation, acquired cash flow from acquisitions, non-cash interest expense);

- History of changing or removing key disclosures in 10-K’s and 10-Q’s;

- Poor maintenance capex and distributable cash flow disclosure in regulatory filings;

- Poor reserve report disclosure in the 10-K's;

- High cost producer;

- Significantly understated maintenance capex;

- Awful record of organic reserve replacement and drill bit capital efficiency (organic F&D cost +$40/boe in 2012);

- Deep in-the-money natural gas swaps rolling off in 2013 (realized gains were ~66% of distributions paid in 2012, but that will shift to a realized loss by 2014);

- Over-levered (BBEP is flirting with its total leverage covenant of 4.75x debt/TTM adjusted EBITDA);

- Large equity raise (we estimate ~$300MM) needed in 3Q13 to avoid breaching total leverage covenant;

- Poor corporate governance;

- Significantly over-valued. We believe that there’s ~70% downside to a fair value equity price of ~$5.00/unit. BBEP was almost a 0 in 2009 – that could easily happen again.

Background

Breitburn Energy Partners LP (BBEP) is an upstream MLP with oil and natural gas production in multiple US onshore basins. Provident Energy Trust (formerly PVE CN) spun out BBEP in a 2006 IPO. “Breitburn GP” is the general partner, but it has no economic interest in the LP after BBEP acquired the entire GP interest from Provident and the founders (Randall Breitenbach and Halbert Washburn) in 2008.

Key assets for BBEP are the Antrim Shale in Michigan (35% of total proved reserves at YE12), legacy oil fields in Wyoming, heavy oil fields in California (Kern County), the Permian Basin, and oil fields in Florida.

In June 2013, BBEP announced that it had acquired Whiting’s (WLL) EOR assets in Oklahoma for ~$800MM (excluding acquired hedges and associated midstream assets). Pro forma this transaction, production will be ~34,000 boe/d (63% liquids, 37% natural gas), and proved reserves will be 184 MMboe.

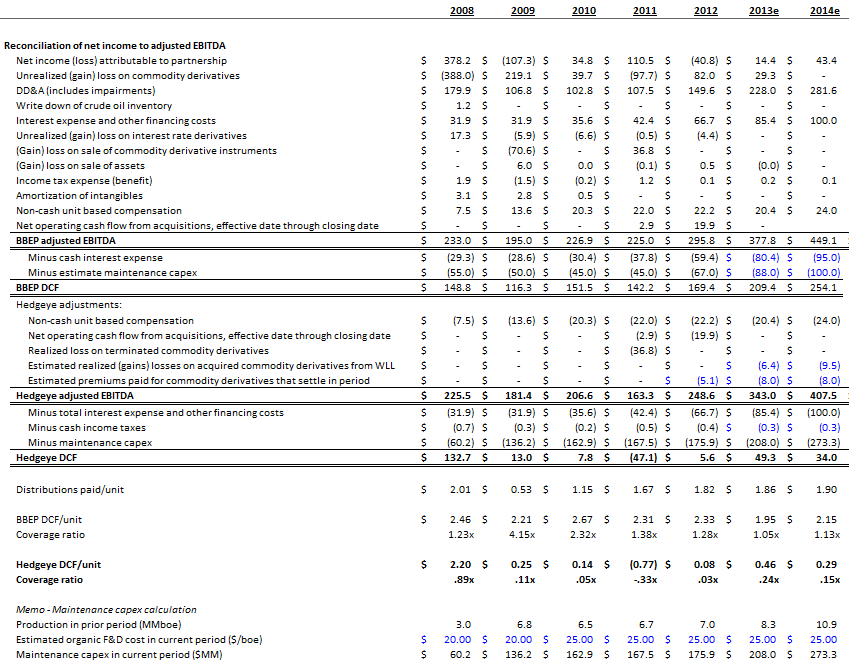

Reconciliation of BBEP's Non-GAAP Financials to Reality

According to BBEP, it generated $2.33/unit of DCF in 2012 for 1.38x coverage. But our calculation of DCF suggests that BBEP only generated $0.08/unit of DCF in 2012 for 0.03x coverage. We estimate that BBEP will generate only $0.46/unit of DCF in 2013 and $0.29/unit in 2014. These figures are in-line with our forward EPU estimates, as they should be.

We discuss the adjustments we make to BBEP's non-GAAP measures in detail below, including the most significant adjustment, maintenance capex. Here is the complete reconciliation:

Aggressive Derivatives Accounting and Games with the Hedge Book

We thought that LINN Energy was the only company that considered a “realized gain” equivalent to a “cash settlement.” We thought wrong. It appears to us that BBEP started doing the same thing in April 2012. And changes in disclosure in the latest 10-Q suggests that management may now be trying to hide it, likely as a result of LINN Energy getting called out on this exact issue in a very public way (and we now know that the SEC is looking into LINN's hedging strategy).

In 2012, BBEP spent $30.0MM on premiums for commodity derivatives (puts, swaps, and swaptions). There is no line item for “premiums paid” in the BBEP’s cash flow statement or reconciliations to adjusted EBITDA; we believe that the premiums paid are considered an unrealized loss.

So, BBEP pays $10 for a derivative, sells it for $11, and accounts for that transactions as:

- $11 realized gain

- $10 unrealized loss

- $1 total gain

- $11 adjusted EBITDA

- $11 distributable cash flow

In our view, this is a ponzi mechanism. Unrealized gains/losses are added back to adjusted EBITDA and DCF; including the premiums paid in unrealized losses is a clever way of excluding those cash costs from adjusted EBITDA and DCF. It is just a way of flowing cash in one door and paying it back out of another as a distribution. How can the SEC be okay with this? How can you have an unrealized loss on a settled derivative?

------

The term “premiums” appears 7 times in the 3Q12 10-Q (filed 10/25/2012). Here is an excerpt with our emphasis:

“Included in the above table are natural gas swaps and put options we entered into in June 2012, hedging a total of 18,628 BBtu from January 1, 2014 to December 31, 2016 at a weighted average Henry Hub price of $4.30 per MMBtu, for which we paid premiums of approximately $7.0 million, and crude oil option contracts we entered into in August 2012, hedging a total of 182,500 barrels from January 1, 2013 to December 31, 2013, at a weighted average NYMEX price of $90.00 per barrel, for which we paid premiums of approximately $1.3 million.

In July 2012, we exercised contracts and paid premiums of $2.5 million for swaption contracts entered into in April 2012 that provided options to hedge a total of 510,168 barrels of future crude oil production associated with the NiMin Energy Corp. ("NiMin") acquisition at then-current NYMEX WTI market prices, ranging from $104.80 per barrel in 2012 to $88.45 per barrel in 2017. In July 2012, we also exercised contracts and paid premiums of $2.6 million for swaption contracts entered into in May 2012 that provided options to hedge a total of 634,485 barrels of future crude oil production associated with the Element Petroleum, LP ("Element") and CrownRock, L.P. ("CrownRock") acquisitions at then-current NYMEX WTI market prices, ranging from $98.35 per barrel in 2012 to $87.80 per barrel in 2017.”

The term “premiums” appears 8 times in the 2012 10-K (filed 2/28/2013). Here is an excerpt with our emphasis:

“Operating activities. Our cash flow from operating activities in 2012 was $191.8 million compared to $128.5 million in 2011. The increase in cash flow from operating activities was primarily due to higher crude oil sales revenue and higher realized gains on commodity derivatives, partially offset by higher operating costs and higher interest expense. We paid $30.0 million in premiums on commodity derivative contracts in 2012 and paid $2.5 million to terminate an interest rate contract. See Note 5 to the consolidated financial statements in this report for more information regarding our derivatives.”

The term “premiums” appears 0 times in the 1Q13 10-Q (filed on 5/3/2013).

Perhaps BBEP didn’t pay any premiums in 1Q13, or perhaps they did and didn’t disclose it? Why doesn’t BBEP want to talk about premiums paid anymore? Regardless, this accounting “trick” will result in $30MM of “fake DCF,” with most of it hitting between 2012 and 2016, by our estimates. It’s not that material, but it probably would’ve gotten material had LINN Energy not been called out on it. The SEC should make BBEP disclose the premiums paid for commodity derivatives that settle in every period for which it purchased them, including future periods. The SEC has already forced LINN Energy to increase disclosure around this issue, we imagine that it will do the same to BBEP.

This is a desperate measure from BBEP. In our view, it is a good indication that the current distribution is divorced from BBEP’s economic reality, and the situation is getting dire, forcing BBEP’s management to get more and more aggressive with its accounting standards.

------

BBEP took it on the chin in the financial crisis. The unit price fell more than 85% from the mid-$30’s in 2007 to $5 in late 2008. In January 2009, it terminated 2011 and 2012 derivatives for a realized gain of $45.6MM, which it used “to pay down debt,” and entered into swaps at lower (market) prices. BBEP terminated oil swaps that were struck up near $90/bbl and entered into new swaps at $63/bbl. BBEP did the same thing again in June 2009, realized a gain of $25MM, and used the proceeds to pay down more debt.

In 2009, in addition to monetizing in-the-money swaps to pay off debt, BBEP adopted a poison pill, suspended making distributions, cut its capital budget by 75%, sold assets, and laid off employees.

------

In 4Q2011, BBEP terminated WTI-linked oil swaps for a “termination cost” of $36.8MM and entered into new Brent-linked swaps, “in order to improve the effectiveness of [its] hedge portfolio.” BBEP took a realized loss of $36.8MM on the termination; however, BBEP added that loss back to adjusted EBITDA.

Recall that BBEP sold its 2011 and 2012 derivatives in 2009 to pay down debt, and re-hedged the oil volumes in the low $60’s. Well BBEP didn’t really want to deal with those underwater hedges…

Oil prices were strong in late 2011 – the WTI 2012 swap was trading ~$100/bbl and the 2013 swap ~$95/bbl, with Brent at a $5 - $10/bbl premium. As of 9/30/2011, BBEP was swapped out at WTI $77/bbl for 2012 and WTI $81/bbl for 2013. Realized losses were coming… So what does BBEP do? It terminates some of the 2012, 2013, and 2014 underwater swaps and takes a realized loss of $36.8MM in 4Q12, adds it back to adjusted EBITDA, and resets its hedge book to strip prices (WTI and Brent). BBEP added some new Brent swaps, which, in our view, was just to make it look like a strategic repositioning of the hedge book. But, really, BBEP was staring at an underwater hedge book, and wanted out of it.

It must be nice to include realized gains in non-GAAP measures like adjusted EBITDA and DCF, and if realized losses are imminent, just terminate the positions, add back the realized losses to adjusted EBITDA and DCF, and pretend like nothing really happened… That add back was 16% of adjusted EBITDA and 36% of the distributions paid in 2011.

Hedge book as of 9/30/2011:

Hedge book as of 12/31/2011:

------

Along with BBEP’s recent acquisition of WLL’s Postle Field, it also bought in-the-money oil swaps from WLL. What BBEP paid WLL for these swaps was not disclosed, but WLL disclosed that the hedges cost them $44.9MM. We estimate that BBEP paid WLL ~$40MM for the swaps, which management confirmed on the deal conference call. And despite the acquisition not scheduled to close until 7/31/2013, BBEP will realize the economics of the hedges starting on 4/1/2013.

BBEP could have just hedged out these volumes on its own at current strip prices at little-to-no cash cost. But buying these hedges from WLL it just another way for BBEP to “buy DCF.” The cost of these derivatives is not included in realized gains/losses, adjusted EBITDA or DCF; it’s essentially paying cash for cash and paying it back out to unitholders as DCF.

The hedges acquired include 6,100 bbl/d from 4/1/13 through 12/31/13 at WTI $98.50; by our estimates, that’s good for ~$6.4MM of incremental DCF in 2013. We estimate that at current strip prices, acquired realized gains will be $10MM in 2014, $17MM in 2015, and $4MM in 2016. If one puts an 8% yield target on that 2014 number, that’s $125MM ($1.25/unit) of “value” for this “strategy.”

------

BBEP is getting more and more aggressive with its hedge book and derivatives accounting because the writing is on the wall. It entered into high priced natural gas swaps back in 2009 when the 2013 strip was above $6.00/MMBtu, but 2013 is the last year when it will really have that benefit of those high-priced gas swaps. BBEP has 58.1 MMMBtu/d swapped at an average price of $5.87/MMBtu for 2013, but that falls off to 46.1 MMMBtu/d swapped at an average price of $5.08/MMBtu in 2014.

In 2012, realized gains on derivatives were $87.6MM (66% of distributions paid); we estimate that realized gains will be only $23MM in 2013, and BBEP will take a realized loss of -$11MM in 2014 (we adjust realized gains/losses to properly account for premiums paid, which we flat line at $7.5MM per year from 2013 through 2016). That’s a painful swing, and BBEP is trying to avoid it.

Inadequate Non-GAAP Disclosures

Analysts and investors primarily value BBEP using DCF/unit and a yield target. However, BBEP does not publish a reconciliation of any measures to DCF in its 10-K's, 10-Q's, or press releases. In fact, the terms "distributable cash flow," "DCF," and "maintenance capex" do not even show up in these filings. Occasionally, management will announce these results on quarterly conference calls (in 2009 it did not). Management defines DCF = adjusted EBITDA minus cash interest expense and estimated maintenance capex. Management will also provide forward-looking guidance on these figures, but never publishes an actual reconciliation to DCF.

Understated Maintenance Capex

BBEP is one of the more cryptic companies with respect to “maintenance capex.” BBEP does not define it in 10-K’s or 10-Q’s and they don’t even publish the number in quarterly press releases. Sometimes management will give the number on the quarterly conference call, but sometimes not. This is very strange given its importance in calculating DCF.

On the 5/3/2013 conference call, management said, “We define maintenance capital as that amount of annual investment required to keep production approximately flat year-over-year.” They went on to say, “When we look at maintenance capital, we're looking out five years and we're looking at our reserve report and our capital plans for that five-year period and we feel comfortable with the 23% of EBITDA, 20% to 25% range.”

In the latest BBEP investor presentation, a footnote reads, “Maintenance capital is defined as the estimated amount of investment in capital projects and obligatory spending on existing facilities and operations needed to hold production approximately constant for the period.”

On the 3/9/2011 conference call, BBEP said that, “Our approach to estimating maintenance capital requirements is very rigorous and based on our reserve data, as well as our long range financial plans.”

As far as we can tell, BBEP does not have a consistent, explicit definition of maintenance capex. We have no idea what goes into this calculation; and we would love to data behind see this “very rigorous” approach, because we just don’t buy it. We think that this slide from BBEP’s 6/19/13 investor presentation shows about how rigorous BBEP is in estimating maintenance capex:

23% of EBITDA! Voila!

------

BBEP’s drill bit performance is so bad that we are wondering what exactly it spends its money on. It is one the worst record of organic reserve replacement that we have seen from an onshore E&P. We presume that BBEP recognizes this, which is why they stopped disclosing the amount of organic reserve adds (extensions, discoveries, infill drilling, recompletions, etc) after 2009. In its reserve report, BBEP’s line item is only “revisions,” which groups together extensions, discoveries, infill drilling, recompletions, technical revisions, price revisions, and timing revisions. This makes it very difficult to assess BBEP’s performance with the drill bit, as price revisions account for the majority of the total revisions.

In 2012, total revisions were -27.1 MMboe “primarily related to a decrease in natural gas prices.” BBEP also tells us that, “The decrease in 2012 was primarily the result of a 30.9 MMboe (185.6 Bcf) decrease in natural gas reserves driven primarily by a decrease in natural gas prices. Price related reserve revisions were partially offset by drilling, recompletions, workovers, addition of new drilling locations and revised estimates of existing reserves.” This implies that organic reserve adds in 2012 were 3.8 MMboe. In 2012, total costs incurred excluding proved acquisition costs were $253MM, implying an organic F&D cost of $66.54/boe. If we back out unproved acquisition costs of $88MM from costs incurred, the organic F&D cost was $42.92.

Total “revisions” over the past 3 years are -7.2 MMboe, and over the past 5 years are -23.8 MMboe, for an organic reserve replacement ratio of -33% and -67%, respectively. Because of scant disclosure, we are not able to back out the price revisions and calculate an average organic F&D number over the periods. But consider that over the past 5 years, BBEP has aggregate costs incurred (excluding proved acquisition costs) of $609MM and organic reserve replacement was negative (revisions of -23.8 MMboe vs. production of 35.4 MMboe). Said another way, BBEP needed to find and develop another 59 MMboe of proved reserves with the drill bit over that period for organic reserve replacement to be 100%. Assuming an F&D cost of $20/boe (generous for BBEP), that’s an incremental $1.2 billion of capital.

We estimate that maintenance capex over the last 5 years was ~$262MM, or $7/boe produced. It’s difficult to know for sure because it’s not actually a statistic that BBEP makes readily available on a consistent basis. During 2009, maintenance capex was an uncomfortable topic, and management stopped giving the data on the conference calls.

------

Strangely, BBEP’s historic PUD conversion cost has been quite good, especially relative to the capital efficiency of its total capital program. The 3 and 5 year average PUD conversion costs were $11.07/boe and $10.53/boe, respectively. Unfortunately for BBEP, the capital spent converting PUDs was only 9% of total costs incurred in 2012 (excluding proved acquisition costs), and BBEP only has 29.7 MMboe of PUD reserves as of YE12, 20% of total proved reserves.

BBEP’s 3 and 5 year all-in FD&A cost was $24.95/boe and $41.26/boe, respectively. Still a poor result, especially for an E&P that produces a lot of natural gas (56% of total production in 2012).

As BBEP has grown via acquisition over the last three years, the capex budget has skyrocketed, though the maintenance capex budget has not kept pace. We believe that BBEP is getting more and more aggressive with its maintenance capex budget; at this point, the maintenance capex rate of ~$8/boe produced is ridiculously low, and not supported at all by prior period drill bit performance.

In 2010, maintenance capex was 67% of total capex; BBEP’s guidance suggests that it will only be ~30% in 2013. Implied growth capex has grown at a 22% CAGR between 2008 and 2013, while maintenance capex grew only at a 10% CAGR. The decline in capital efficiency is notable, particularly for implied growth capex. In 2013, total capex per boe produced will be ~$27/boe (up from $16/boe in 2012). BBEP’s growth capex per boe produced will be ~$19/boe (up from $8/boe in 2012), while maintenance capex will be $8/boe (flat from 2012). BBEP's maintenance capex is more than twice as efficient as its growth capex, which is convenient for a company that deducts only maintenance capex from DCF.

How understated is maintenance capex? Well in 2012 BBEP incurred $152MM of “development costs” and added 3.8 MMboe of proved reserves, for a per boe rate of $40.21 (this is generous to not include any of the capital BBEP spent on land and asset retirement obligations). Production was 7.0 MMboe in 2012, so to keep the reserve base flat in 2013 BBEP would need to add 7.0MMboe of reserves with the drill bit. $40.21/boe x 7.0 MMboe = $281MM. Compare that to BBEP’s 2013 maintenance capex guidance of $88MM. This suggests that maintenance capex for 2013 is understated by $193MM, which is equal to 100% of the forecasted distribution.

Even if we given BBEP some benefit of doubt and assume an organic F&D cost of $25/boe – which is not even in the ball park of BBEP’s actual results – that would imply $176MM of maintenance capex, double BBEP’s guide.

Aggressive Adjustments to Non-GAAP Financial Measures

BBEP backdates the effective date of an acquisition, and adds “net operating cash flow from acquisitions, effective date through closing date” to adjusted EBITDA. The purchase price is adjusted higher for the amount of “net operating cash flow” acquired between the effective date and the closing date, so this runs through the “property acquisitions” line in the cash flow statement. Again – this is paying cash for cash, and calling it distributable cash flow. Further – as far as we can tell – BBEP does not assign any “maintenance capex” to the acquired operating cash flows. This adjustment was $2.9MM in 2011 (3% of distributions paid) and $19.9MM in 2012 (15% of distributions paid).

BBEP’s recent Postle Field acquisition has an expected closing date of 7/31/13 and an effective date of 4/1/13, so BBEP is acquiring 4 months of “net operating cash flow” from WLL. We estimate that the Postle Field generates ~$10MM of EBITDA per month at current prices; acquired “net operating cash flow” from this deal alone could be ~$40MM...However – it appears that management has recently “got religion” (from the 6/24/13 deal conference call):

<Q - Analyst>: “Okay. Thanks. And just last question from me, just as a point of clarification, will you be realizing an add-back in the second quarter for the cash flow from this acquisition between the effective date and closing date?”

<A –BBEP CFO James G. Jackson>: “Praneeth, it's Jim. We won't be doing that.”

Why not? BBEP used to make this adjustment, now they think it's a bad idea?

------

BBEP adds back unit-based compensation to adjusted EBITDA. Imagine how profitable BBEP would be if it paid all of its employees and contractors in equity! EBITDA does not = non-cash. Unit-based compensation is an economic expense, and it is aggressive, in our view, to add it back to adjusted EBITDA and DCF. In 2012, the adjustment was $22.2MM, or 8% of adjusted EBITDA and 17% of distributions paid.

BBEP deducts “cash interest expense” from adjusted EBITDA to arrive at DCF, not total interest expense and other financing fees. In 2012, the difference was $7.3MM, or 6% of distributions paid.

BBEP does not deduct cash taxes from adjusted EBITDA to arrive at DCF, despite BBEP being subject to some federal and states taxes. BBEP has paid cash income taxes between $0.2MM and $0.5MM in each of the last three years.

In total, we estimate that these adjustments boosted DCF in 2012 by $50MM, or 38% of distributions paid.

Dangerously Over-Levered; Large Equity Raise is Imminent

BBEP has levered up in a big way pro forma this $890MM Postle Field acquisition that it has funded entirely with debt (up until now anyway). We believe that BBEP will breach its amended total leverage covenant of 4.75x debt/TTM adjusted EBITDA (using BBEP’s aggressive definition of adjusted EBITDA) if it does not raise ~$300MM of equity before the end of 3Q13. This could be highly dilutive; if BBEP manages to sell $300MM of equity at $17.00/unit, that would be 17.6MM new shares and ~18% dilution.

Even if BBEP manages to sell $300MM equity in 3Q13, we estimate that net debt will be back to ~$1.8B by YE14 (assuming no distribution cut and $300MM of capital spending in 2014), and total debt/TTM adjusted EBITDA will be back at 3.9x (again, using BBEP’s definition), pushing up against the leverage covenant of 4.0x. So another capital raise will likely be necessary in 2014.

Poor Corporate Governance and Little Alignment with BBEP Unitholders

We recap the following situation involving BBEP's board and executive officers because we think it is indicative of BBEP's corporate governance standards and commitment to the LP unitholders:

In September 2007, BBEP acquired natural gas and oil assets from Quicksilver Resources (KWK) for $1.5B, with $750MM paid in cash and $750MM in BBEP common units. KWK received 21.3MM common units at an average unit price of $35/unit; KWK became BBEP’s largest unitholder with a 32% stake, and was locked up on those shares until November 1, 2008.

Provident Energy Trust (PVE CN) held 14.4MM BBEP common units (22% of total) and a 95.55% interest in the GP stake (equivalent to 0.4MM BBEP common units) in February 2008 when it announced that it was seeking an exit from this investment.

On 6/17/08, BBEP announced that it would acquire Provident’s entire stake in the common units and its GP interest, as well as the founders’ interest in the GP (4.45%), for $345MM cash, or ~$23.25/BBEP unit. This was a 5% premium to the unit price as of the 6/16/08 close. BBEP funded the deal with a draw on the credit facility.

In late 2008, BBEP’s unit price collapsed to $5/unit in a solvency/liquidity crisis. In 2009, BBEP suspended the distribution, cut capex 75%, monetized in-the-money swap contracts, and sold off assets. It was not a good situation.

KWK took a bath on its BBEP shares, as the equity that it was locked up on fell from ~$750MM in value in September 2007 to ~$100MM in value in December 2008. Provident Energy Trust and BBEP’s founders made out nicely with their exit at $23/unit. But BBEP unitholders got killed as this transaction, in part, nearly put BBEP into bankruptcy.

As you can imagine, in October 2008, KWK filed a fairly scathing lawsuit against Breitburn Energy Partners LP, Provident Energy, and individuals on the board of BBEP, including the founders Randall Breitenbach and Halbert Washburn.

In December 2009, KWK settled with BBEP and a third party for $18.0MM cash, along with conditions for KWK to put two directors on the board of the GP, and BBEP to resume paying the quarterly distribution. Over the course of 2010 and 2011, KWK sold all of its BBEP common units for estimated proceeds of ~$275MM (~$13/unit).

------

All directors and executive officers own only 2.5% of the common units outstanding, with founders Randall Breitenbach and Halbert Washburn each holding 1.0%. No other insider beneficially owns a material stake. Annual bonuses are discretionary, and it appears from the proxy that BBEP’s executive officers get paid primarily for buying assets and raising capital. BBEP does not make its performance goals public, so there is no way of knowing what they exactly are and whether or not BBEP is achieving them.

Valuation

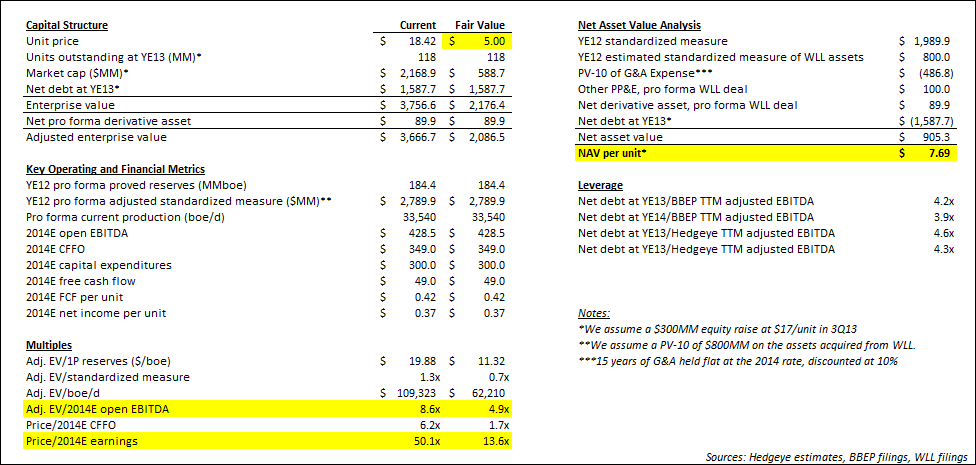

1. We believe that fair value for BBEP equity is a mid-single digit number, call is between $2 - 8/unit.

2. We estimate that BBEP will earn $0.37/unit in 2014; with the current annual distribution run rate at $1.90/unit, alarm bells should be ringing. BBEP is currently trading at +50x 2014E earnings vs. the S&P E&P Index at 12x. A market multiple implies a fair price of ~$4.00/unit, ~80% downside from the current price.

3. We estimate that BBEP will generate $430MM of open EBITDA in 2014. BBEP is currently trading at 8.4x 2014E EBITDA vs. the S&P E&P Index at 4.2x. A market multiple implies a fair price of $2.50/unit. A premium multiple of 5.0x 2014E EBITDA implies a fair price of ~$5.50/unit, ~70% downside from the current price.

4. For our net asset value calculation, we relied primarily upon the SEC standardized measure as of YE12. We assume that BBEP paid fair value for WLL's Postle Field - after all, it was on the market for a long time in a highly competitve asset acquisition market; we value the acquired oil assets at $800MM and give BBEP credit for the acquired hedges and midstream assets in other PP&E and the net derivative asset. We then assume 15 years of G&A - in line with the reserve life - at the 2014 rate, and discount it back at 10%. Our NAV is $7.70/unit, ~60% downside from the current price.

Summary

If you think short LINN Energy is a good idea, you should be short BBEP. The similarities between the two companies with respect to derivatives accounting, aggressive adjustments to non-GAAP measures, and understated maintenance capex are uncanny. BBEP's leverage situation is more desperate, with an large equity raise needed this quarter. Fair value = $5.00/unit. The distribution is little more than a figment of management's imagination and their ability to raise enough capital to fund it.

Kevin Kaiser

Senior Analyst

(o)