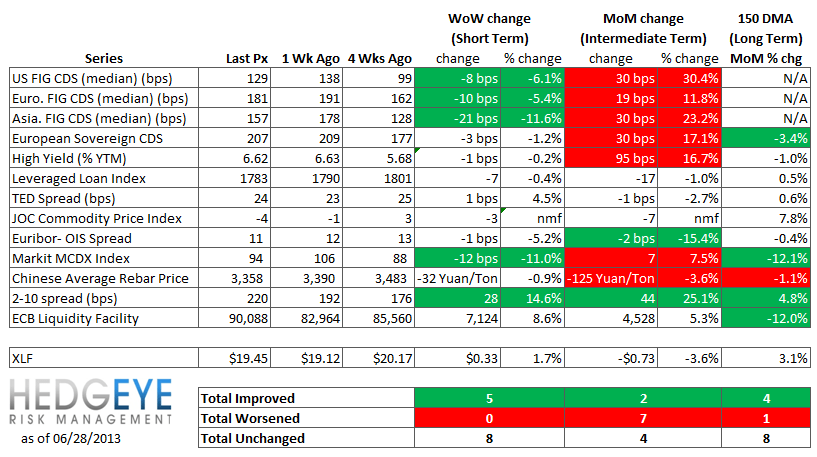

Key Takeaways:

Asia remains the most interesting focal area for global risk right now. After roughly a month of negative headlines and deteriorating conditions, China's situation has stabilized (for now). We saw a sharp reversal in Chinese bank swaps - the first since the crisis began. Meanwhile, Indian banks continue to look awful. The three major Indian banks are now all at or near 300 bps on their CDS and the rise has been remarkable. We think not enough attention is being paid to this situation. We've also been calling out High Yield as a key focal area. Fortunately, it finally settled out this past week, but it's less-often mentioned cousin, levered loans, continues to sell off.

* Asian Financial CDS - China & India divergence continues to grow. Chinese bank swaps reversed course last week, tightening significantly WoW, while Indian bank swaps continue to blow out. India's three major banks are all now above or near the 300 bps "Lehman line". Japanese banks were relatively uneventful on the week, posting small average increases.

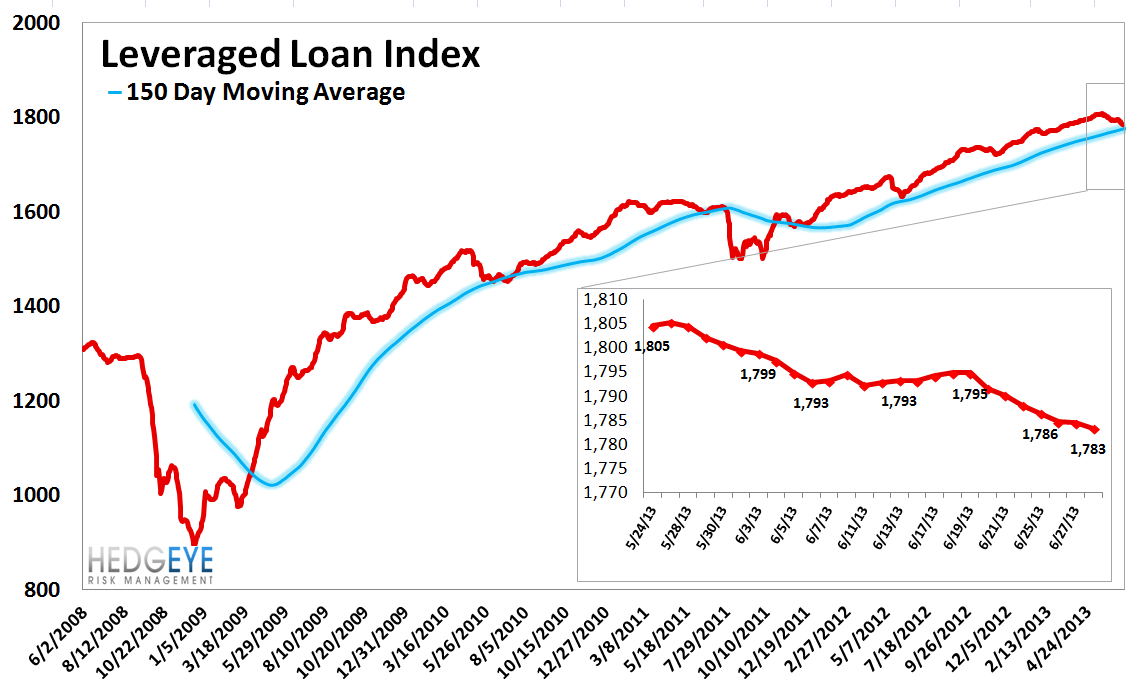

* Leveraged Loan Index Monitor – The Leveraged Loan Index fell -6.8 points last week, ending at 1783.36.

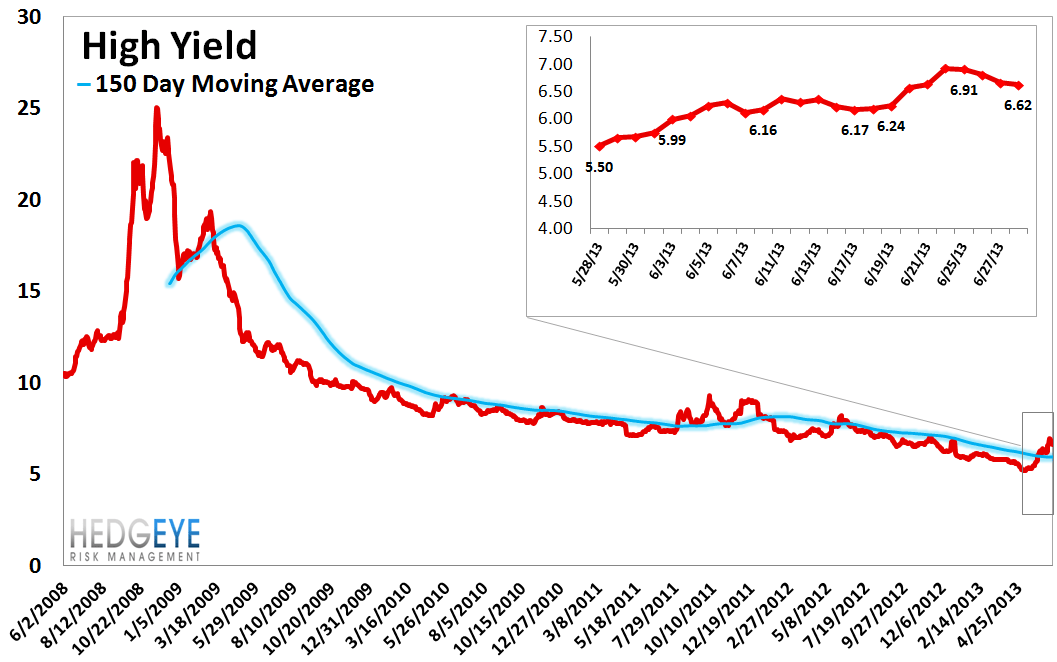

* High Yield (YTM) Monitor – High Yield rates fell 1.3 bps last week, ending the week at 6.62% versus 6.63% the prior week.

* 2-10 Spread – Last week the 2-10 spread widened 28 bps to 220 bps.

* XLF Macro Quantitative Setup – Our Macro team’s quantitative setup in the XLF shows 2.6% upside to TRADE resistance and 0.7% downside to TRADE support.

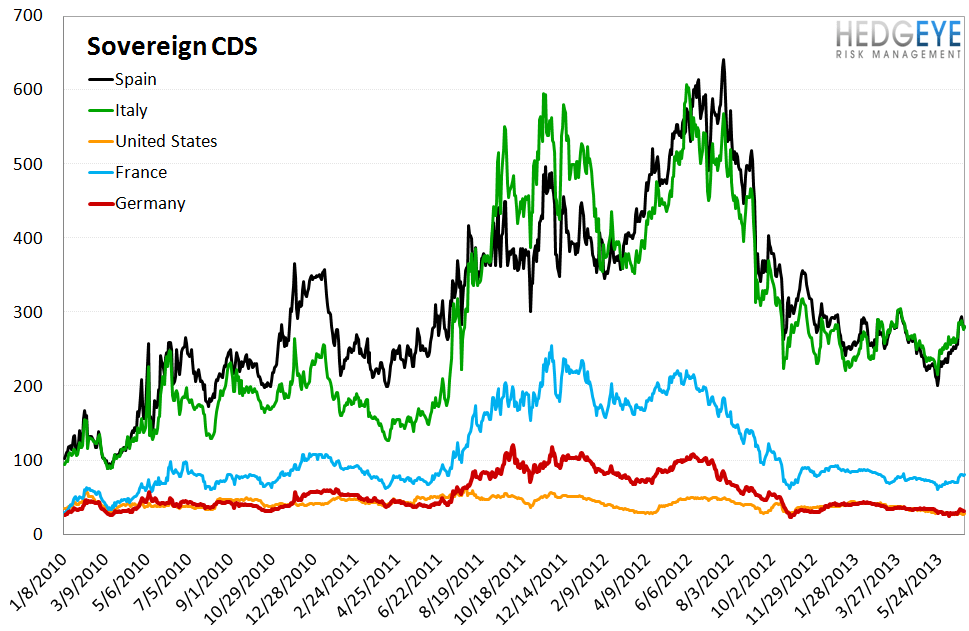

* Sovereign CDS – Sovereign swaps globally last week, with the exception of France, which saw its swaps widen 2 bps to 80 bps. Germany was unchanged at 32 bps. Japan tightened by 8 bps to 78 bps.

Financial Risk Monitor Summary

• Short-term(WoW): Positive / 5 of 13 improved / 0 out of 13 worsened / 8 of 13 unchanged

• Intermediate-term(WoW): Negative / 2 of 13 improved / 7 out of 13 worsened / 4 of 13 unchanged

• Long-term(WoW): Positive / 4 of 13 improved / 1 out of 13 worsened / 8 of 13 unchanged

1. U.S. Financial CDS - It was a mixed week for U.S. Financials, although overall more reference entities tightened than widened. On balance, swaps tightened for 21 out of 27 domestic financial institutions we track. The large cap U.S. banks were largely uneventful with the largest move coming from MS (-7 bps).

Tightened the most WoW: PRU, MET, MMC

Widened the most WoW: AGO, MTG, JPM

Widened the least WoW: MMC, SLM, MET

Widened the most MoM: MBI, RDN, GS

2. European Financial CDS - Swaps were generally tighter among European banks last week, mirroring the trend we saw in EU sovereigns. We've been calling out Sberbank of Russia as a laggard in recent weeks with the commodity crack-up casting a shadow over its outlook. Last week we saw some reprieve for Russia's largest bank with swaps tightening 27 bps to 250 bps.

3. Asian Financial CDS - China & India divergence continues to grow. Chinese bank swaps reversed course last week, tightening significantly WoW, while Indian bank swaps continued to blow out. India's three major banks are all now above or near the 300 bps "Lehman line". Japanese banks were relatively uneventful on the week, posting small average increases.

4. Sovereign CDS – Sovereign swaps globally last week, with the exception of France, which saw its swaps widen 2 bps to 80 bps. Germany was unchanged at 32 bps. Japan tightened by 8 bps to 78 bps.

5. High Yield (YTM) Monitor – High Yield rates fell 1.3 bps last week, ending the week at 6.62% versus 6.63% the prior week.

6. Leveraged Loan Index Monitor – The Leveraged Loan Index fell -6.8 points last week, ending at 1783.36.

7. TED Spread Monitor – The TED spread rose 1.0 basis points last week, ending the week at 24.01 bps this week versus last week’s print of 22.975 bps.

8. Journal of Commerce Commodity Price Index – The JOC index fell -3.1 points, ending the week at -4.43 versus -1.4 the prior week.

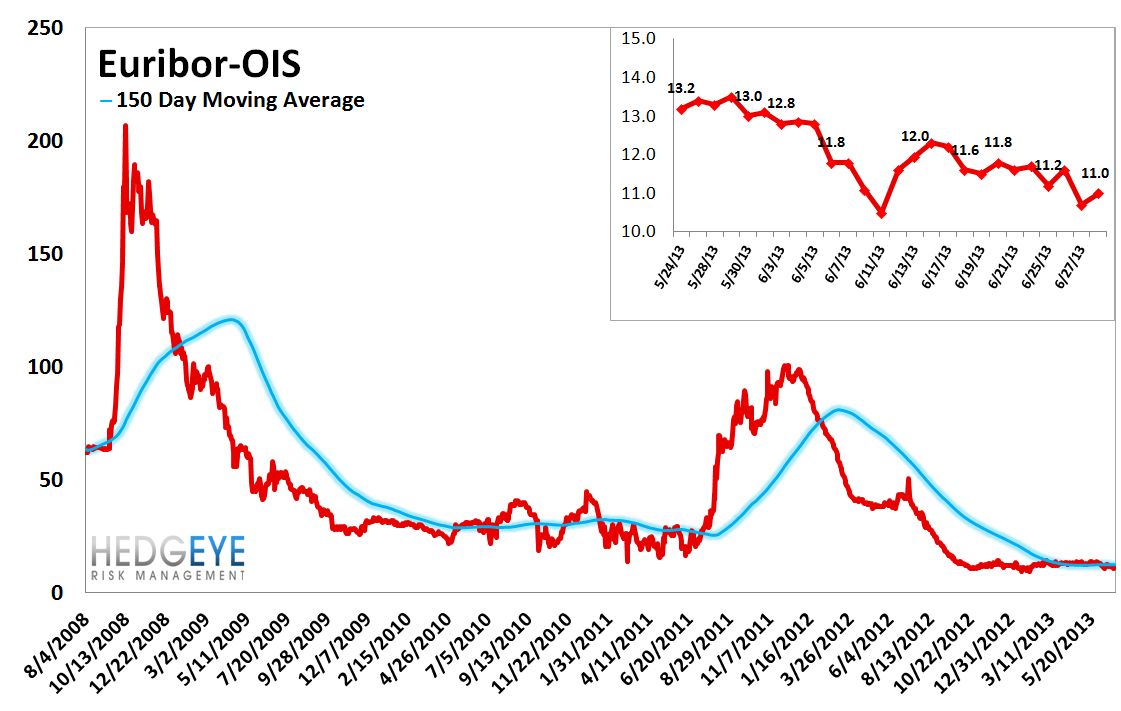

9. Euribor-OIS Spread – The Euribor-OIS spread tightened by 1 bp to 11 bps. The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk.

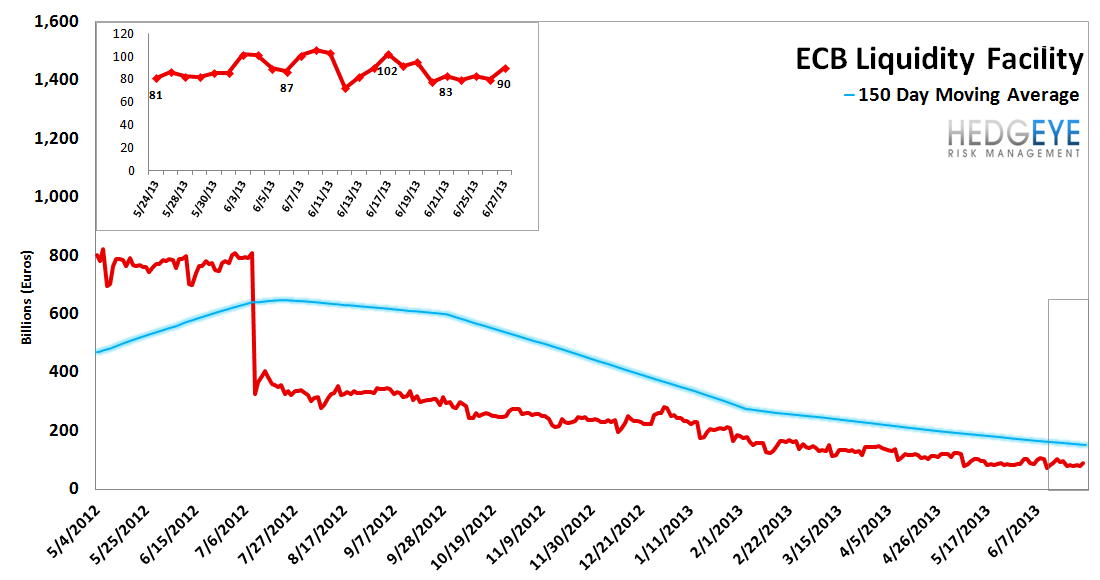

10. ECB Liquidity Recourse to the Deposit Facility – Overnight deposits rose 7.1 billion Euros last week. The ECB Liquidity Recourse to the Deposit Facility measures banks’ overnight deposits with the ECB. Taken in conjunction with excess reserves, the ECB deposit facility measures excess liquidity in the Euro banking system. An increase in this metric shows that banks are borrowing from the ECB. In other words, the deposit facility measures one element of the ECB response to the crisis.

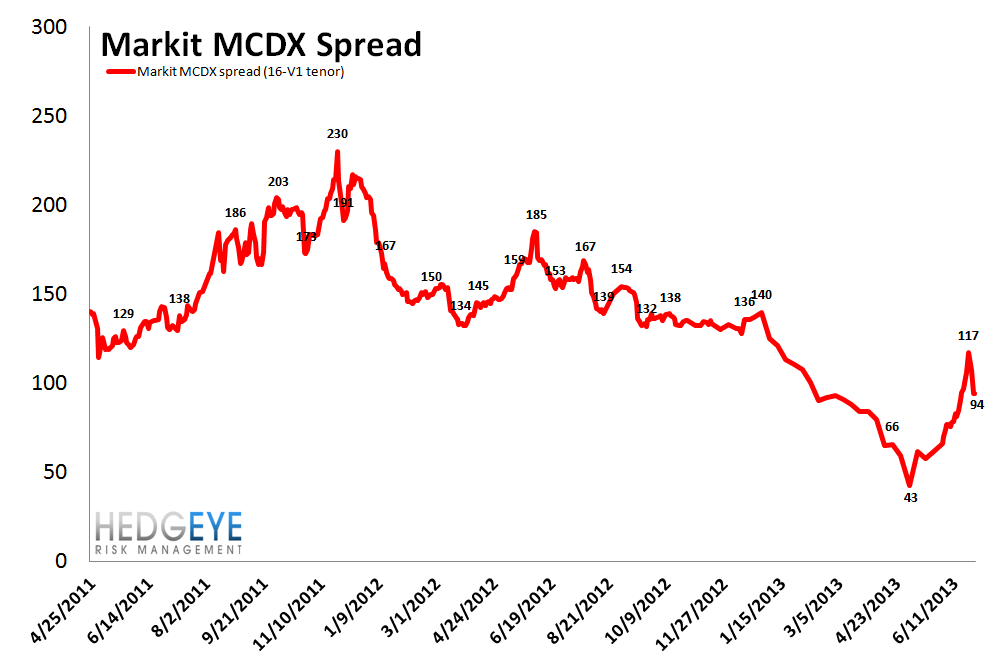

11. Markit MCDX Index Monitor – Last week spreads tightened 12 bps, ending the week at 94.3 bps versus 106 bps the prior week. The Markit MCDX is a measure of municipal credit default swaps. We believe this index is a useful indicator of pressure in state and local governments. Markit publishes index values daily on six 5-year tenor baskets including 50 reference entities each. Each basket includes a diversified pool of revenue and GO bonds from a broad array of states. We track the 16-V1.

12. Chinese Steel – Steel prices in China fell 0.9% last week, or 32 yuan/ton, to 3358 yuan/ton. We use Chinese steel rebar prices to gauge Chinese construction activity, and, by extension, the health of the Chinese economy.

13. 2-10 Spread – Last week the 2-10 spread widened 28 bps to 220 bps. We track the 2-10 spread as an indicator of bank margin pressure.

14. XLF Macro Quantitative Setup – Our Macro team’s quantitative setup in the XLF shows 2.6% upside to TRADE resistance and 0.7% downside to TRADE support.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT