TODAY’S S&P 500 SET-UP – July 1, 2013

As we look at today's setup for the S&P 500, the range is 60 points or 3.01% downside to 1558 and 0.73% upside to 1618.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.16 from 2.13

- VIX closed at 16.86 1 day percent change of 0.00%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:58am: Markit U.S. PMI Final, June, est. 52.4

- 10am: Construction Spending, May, est. 0.6% (prior 0.4%)

- 10am: ISM Manufacturing, June., est. 50.5 (prior 49)

- 11:30am: U.S. to sell $30b 3M bills, $25b 6M bills

- U.S. Weekly Rates Agenda

GOVERNMENT:

- House, Senate not in session

- NCUA deadline for comments on its consultation on federal credit union ownership of fixed assets

- U.S. deadline for financial institutions to stop dealing in the rial, Iran’s currency, or face sanctions

WHAT TO WATCH

- Onyx seeks suitors after rejecting $120/shr Amgen bid

- Nokia buys out Siemens in wireless gear venture for $2.2b

- Euro-area PMI contracts less than estimated

- Chinese PMIs fall as slowdown persists

- Apple seeks to trademark ’iWatch’ in Japan

- U.S. 10Y ylds belong at 2.20% as Fed too optimistic: Gross

- SAC’s Cohen said to have declined to testify for grand jury

- Russell reconstitution effective as of Friday’s close

- Final Russell 1000, 2000 membership lists posted today

- News Corp. to start trading as FOXA, NWSA

- U.S. Weekly Agendas: Finance, Industrials, Energy, Health, Consumer, Tech, Media/Ent, Real Estate, Transports

- North American M&A Agenda

- Canada Weekly Agendas: Energy, Mining

- U.S. Jobs, Iran Sanctions, Croatia, Wimbledon: Week Ahead July 1-6

EARNINGS:

- No earnings scheduled by S&P 500 cos.: Bloomberg data

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- LME Seeks to Reduce Lines at Warehouses Where Wait Is 100 Days

- Hedge Funds Cut Gold Bets as Goldman Lowers Outlook: Commodities

- Rusal Urges Further Aluminum Capacity Cuts to Bolster Prices

- WTI Crude Gains After Quarterly Drop Amid Egypt Mass Protests

- Gold Gains in London as Record Quarterly Drop May Spur Demand

- Copper Rises Before Report Seen Showing U.S. Manufacturing Gain

- ICL Falls to 19-Month Low on Corn Prices, Laws: Tel Aviv Mover

- Raw Sugar Climbs in New York Before July Delivery; Cocoa Drops

- Copper Warehouses Emptying as China Imports: Chart of the Day

- Gas Exporters to Defend Pricing System as Courts Reject Oil Link

- Bullish Natural Gas Bets Fall to Three-Month Low: Energy Markets

- Dutch Gasoline Exports to U.S. Reach 11-Month High: BI Chart

- Africa’s Richest Man Vies With China Over Nigerian Tomatoes

- Rebar Declines as Pace of Manufacturing Growth in China Slows

CURRENCIES

GLOBAL PERFORMANCE

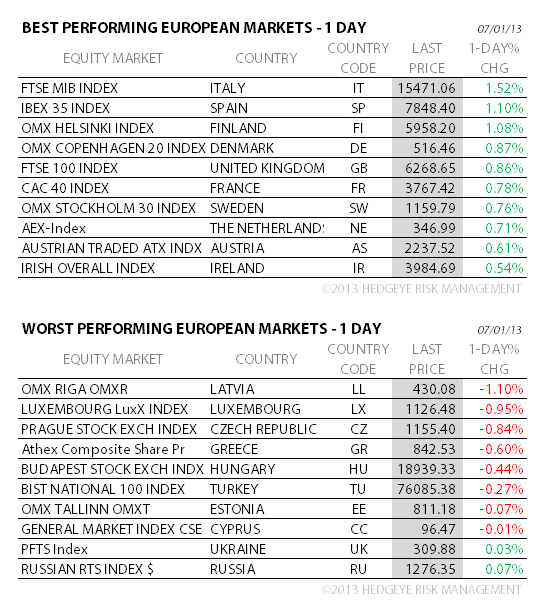

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team