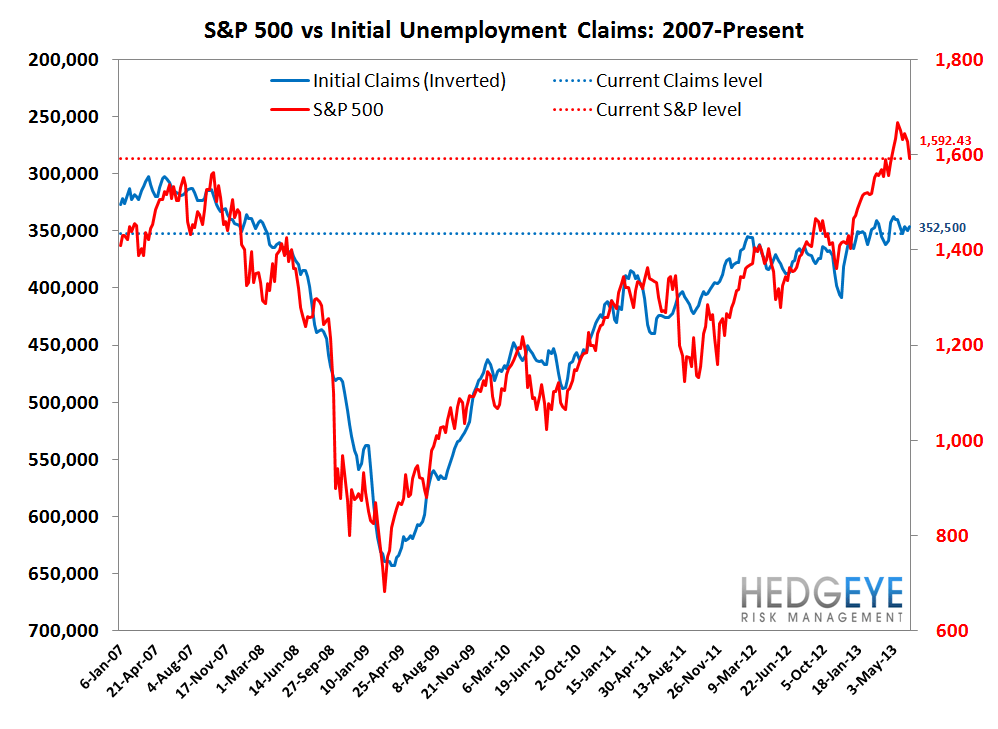

A Steadily Widening Divergence

No real change this week vs. the trend we've been seeing over the last several weeks in claims. NSA data continues to improve at an accelerating YoY rate, on both a 1-week and 4-week rolling-average basis. NSA claims were 9.6% better than at this time last year, and, by coincidence, the 4-week moving average was also better by 9.6%. These represent sequential improvements vs. 7.7% and 9.1% YoY changes, respectively. The bottom line is that the accelerating improvement we've been seeing for the last few months continued last week. We continue to hypothesize that one contributing factor is Obamacare, which is causing high-employment, relatively low-wage industries like restaurants and hospitality to replace 3 full-time employees with 4 part-time employees to stay underneath the 30-hour ACA cutoff. We've been seeing and hearing a fair amount of anecdotal evidence in support of this idea.

On the seasonally-adjusted side, the data wasn't bad, but it wasn't great either. Essentially rolling SA claims went sideways again this week - a growing divergence vs. the trend in the NSA data - consistent with prior years. This trend should continue for two more months, when it peaks in August. Thereafter, we'll begin to see the reversal - SA claims data will begin to appear stronger than NSA data and the sector should be very strong in response.

The Data

Prior to revision, initial jobless claims fell 8k to 346k from 354k WoW, as the prior week's number was revised up by 1k to 355k.

The headline (unrevised) number shows claims were lower by 9k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims fell -2.75k WoW to 346.75k.

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -9.6% lower YoY, which is a sequential improvement versus the previous week's YoY change of -9.1%

<chart19>

Yield Spreads

The 2-10 spread rose 11.8 basis points WoW to 217 bps. 2Q13TD, the 2-10 spread is averaging 169 bps, which is higher by 2 bps relative to 1Q13.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT