THE MACAU METRO MONITOR, JUNE 27 2013

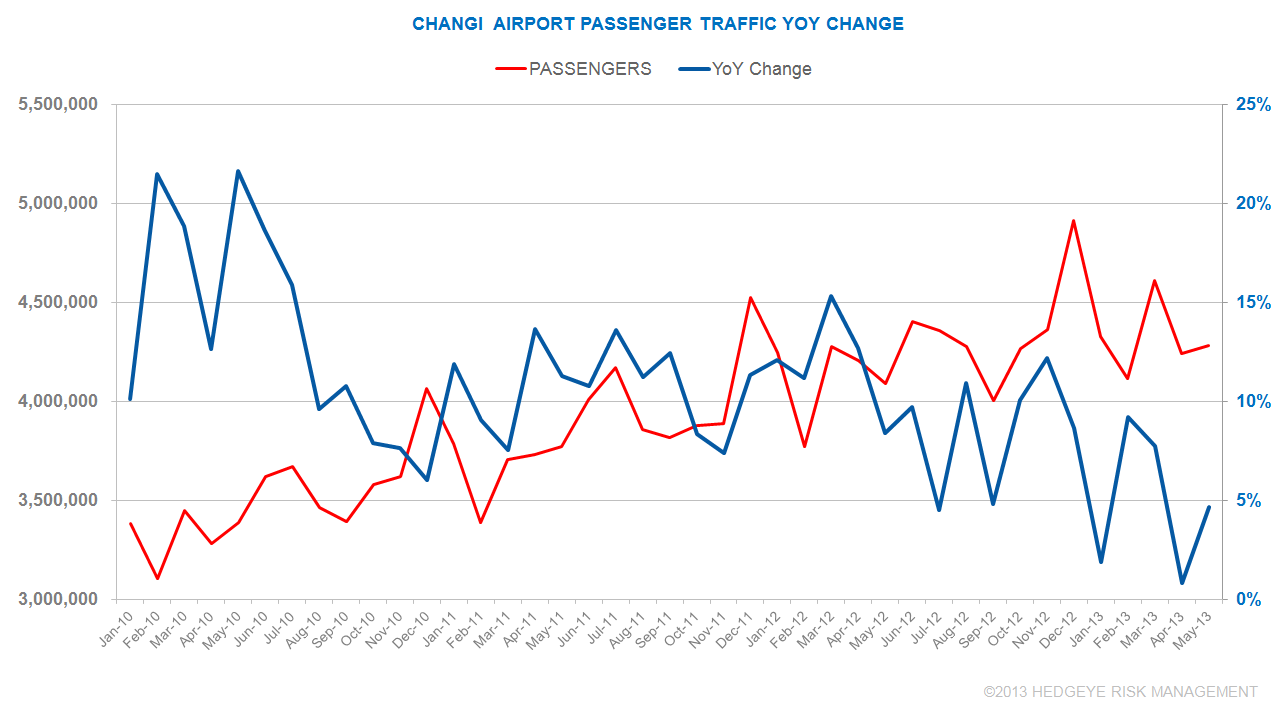

MONTHLY BREAKDOWN OF PASSENGER MOVEMENTS Changi Airport

May passenger volume at Singapore's Changi Airport rose 4.7% in May to 4,281,153.

EMPLOYMENT SURVEY FOR MARCH-MAY 2013 DSEC

The unemployment rate for March - May 2013 was 1.8%, down by 0.1% point over the previous period (February-April).