General Mills is on the tape with Q4 2013 and FY results. Q4 EPS was in line with consensus at $0.53 and the top-line beat at $4.41B vs $4.32B. For the FY, adjusted EPS totaled $2.69 vs $2.56 a year ago and net sales rose 7% to $17.8B. The stock is trading down to ~ $48 (nearly where it was at when it released its Q3 results) and we have concerns about its business mix and 2014 outlook.

While net sales grew 7% in for FY 2013, 6% was composed of new business acquisitions (primarily Yoki), masking weakness in its base business. Certainly 2013 was a strong year of investment, but the company did not see profitability in yogurt (Yoplait) despite heavy investment and the cereal category remains a laggard, both of which compose two of its top three business segments. We think that due to this underlying weakness, particularly in the U.S., and given its forecast for a 3% COGS headwind in FY 2014, the company will be challenged to meet and beat its expectations, as we expect only modest improvement from its yogurt segment, and are projecting a slower recovery in volumes across the entire business compounded by muted to slowing growth globally.

What we liked:

- International sales profit of +24% with growth across every region; outperformance from Latin America (+116%) despite devaluation of the Venezuela bolivar

- Net sales of Bakeries & Foodservices in FY declined -1%, but operating profit rose 10% to $315M

- 2014 to maintain 7% FCF yield; increase dividend by 15%; and buy back 2% of the stock

What we didn’t like:

- Gross Margin declined on the quarter from 37.2% to 34.8% and for the FY from 36.9% to 36.1%

- FY U.S. retail sales up a mere 1% to $10.6B, with Y/Y net sales weakness in Yoplait (-5%), Frozen Foods (-3%), and Big G (-0.2%)

- Reliance on margin management to combat 3% COGS headwind in 2014

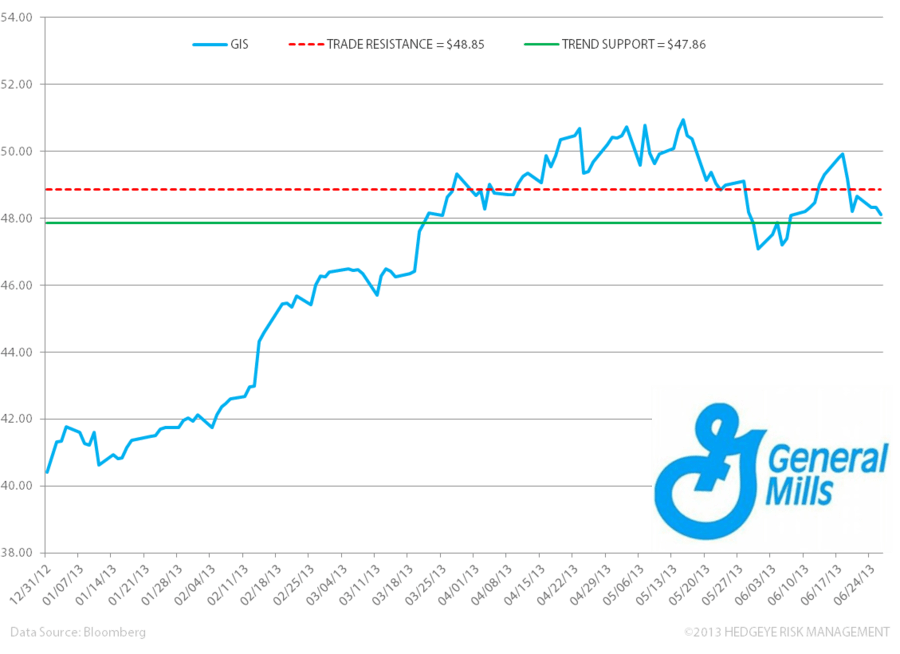

Below we outline our quantitative levels on GIS. The stock is currently trading between its immediate term TRADE and intermediate term TREND levels. We maintain a bearish bias.

Matthew Hedrick

Senior Analyst