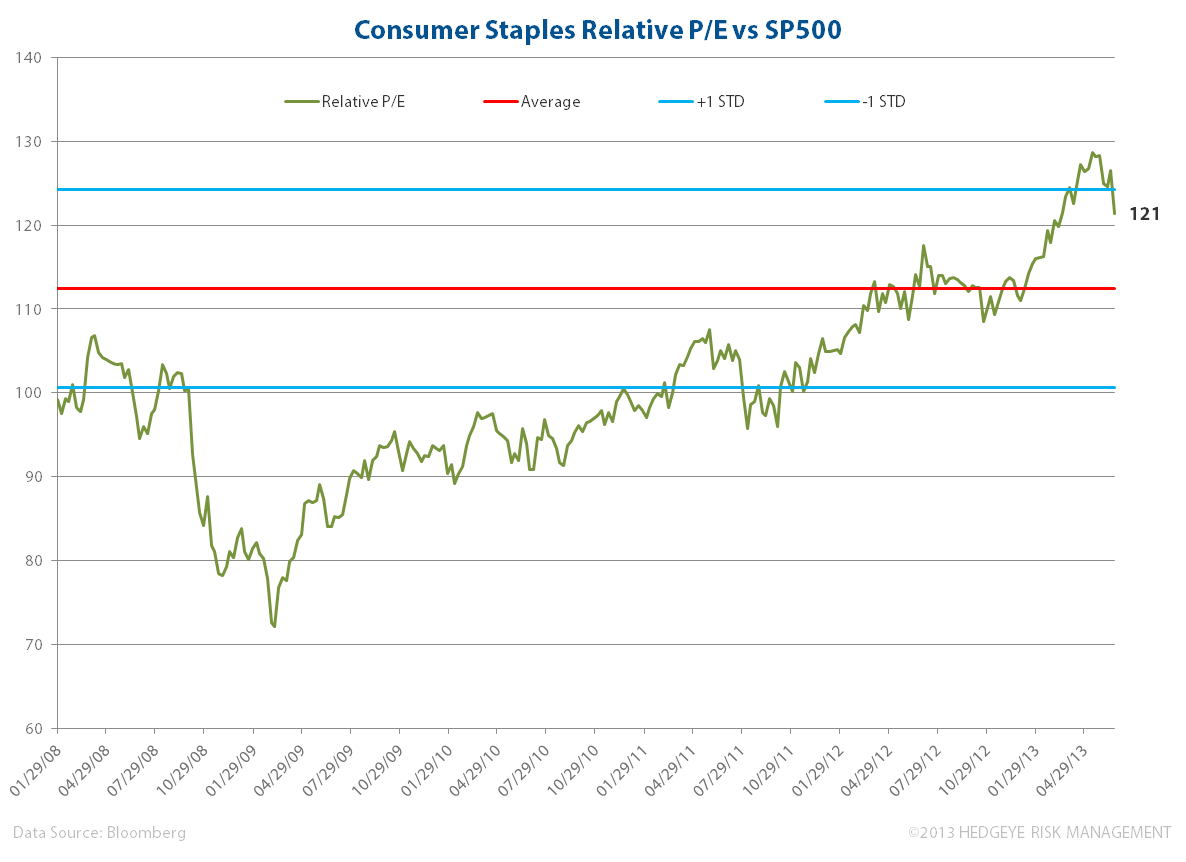

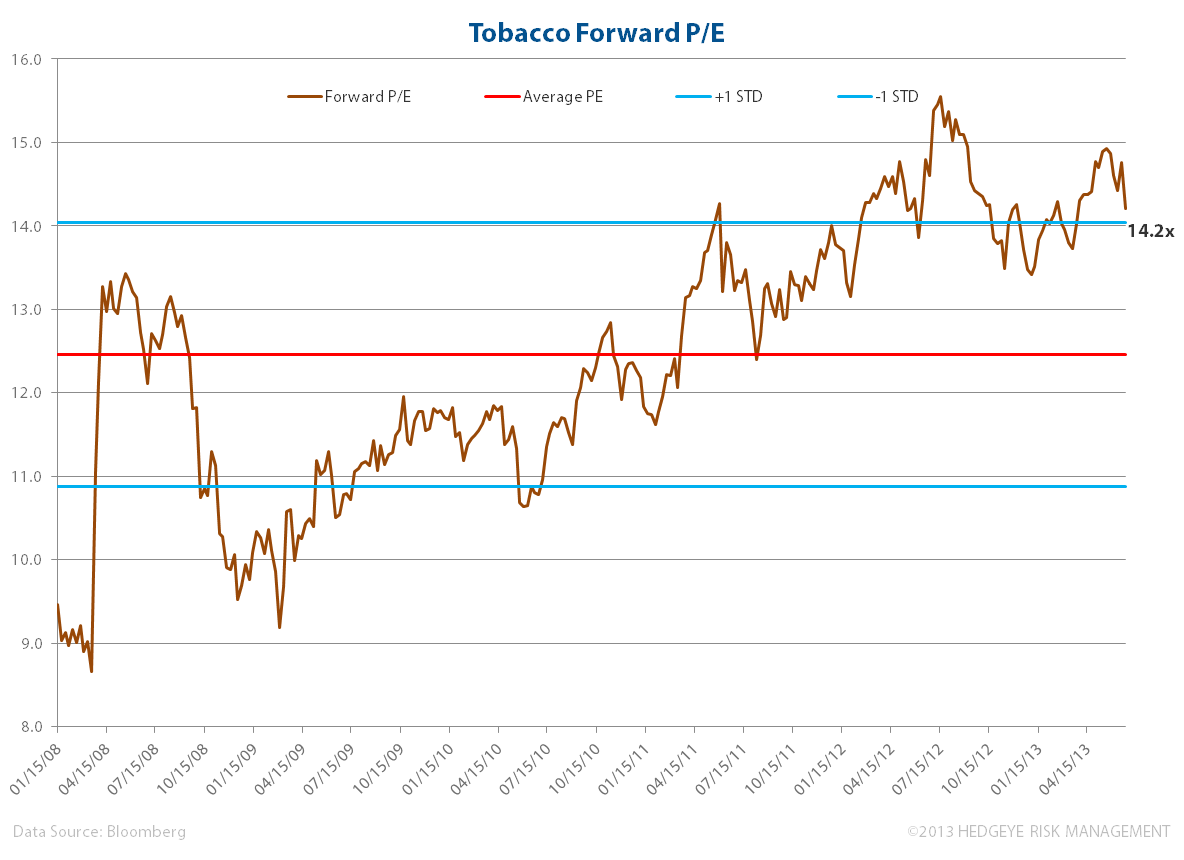

Valuation alone is never a catalyst in our investment process; however below we updated charts on forward P/Es of the consumer staples sector and its main sub sectors.

Needless to say, while valuations have come in over the last two months, they remain stretched, and cheap alone (think CPB or TAP) is not a signal for us to buy. At 17.5x, the consumer staples P/E is just under a two standard deviation move, and compares to an average of 14.5x over the last 5.5 years.

Of note is that sub sectors of HPC and Beverage have come in the most over the last ten days, yet all sub sectors are priced well over one standard deviation.

Our quantitative real-time set-up for consumer staples (etf: XLP) is bullish, trading above its intermediate term TREND line of $38.71, and we would buy it (cheaper) closer to this level.

Matthew Hedrick

Senior Analyst