Darden is being mismanaged, plain and simple.

The earnings call on Friday underscored our argument that Darden needs a shakeup in the C-Suite. $1 billion in operating cash (annually) is not being put to productive use and statements from the company’s leadership on Friday did not demonstrate an ability to turn the company around. There was a mea culpa, of sorts, at the beginning of the call where management acknowledged the detrimental impact of operational reorganization and margin pressure from promotional strategies. That said, we believe that the past five years’ performance has been indicative of a mismanaged business. The sum of the parts is greater than the whole, at Darden, and we believe there is a striking opportunity for an activist to enter the fray, unlock value, and benefit holders of the company’s stock.

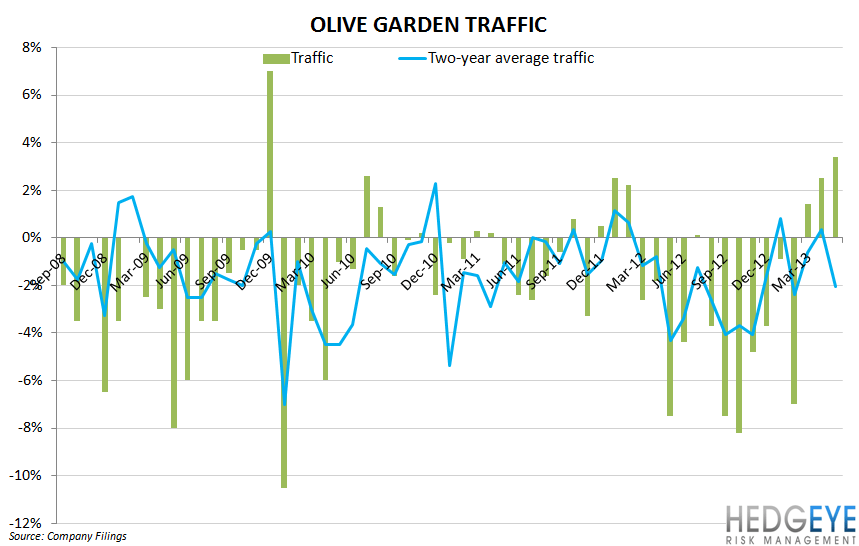

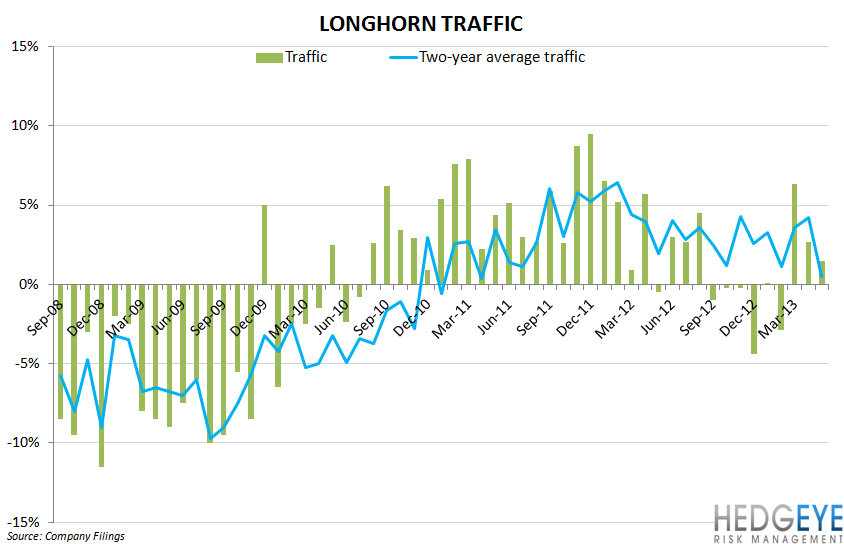

Too Big To Move Traffic

“Now as fiscal 2013 unfolded, I think many of you know that we moved with added urgency to address the same restaurant traffic erosion we'd been experiencing since the recession started. First, we began to match the competitive promotional intensity around affordability. And that included being more aggressive with our offers and our advertising messages and with our use of tactical support like daily and weekly digital specials. Second, we began to more aggressively address affordability in our core menus. And that included launching, with some heavy media support, a new Red Lobster core menu that has a significant affordability component, and then also accelerating introduction of new more affordable core menu offerings at both Olive Garden and LongHorn Steakhouse. And then third, we increased the resources dedicated to reshaping our guest experiences to respond to what guests want beyond affordability. And that meant reorganizing our marketing and operations groups, and ramping up investment in better digital and other capabilities.”

We would guess that management’s commentary on traffic did not sit well with many of the investors listening to the earnings call on Friday. Two-year average traffic has been negative for much of the past year as the company has struggled to regain customers lost during the Great Recession. Management has delivered different plans of action, with sporadically successful promotions being the most common focus. Without a reliable means to drive traffic, however, comps at the most important concepts have been highly disappointing on a two-year average basis.

The reality is this: it has been evident for some time that the company has had a traffic problem. Given the CEO’s comment during Friday’s earnings, call, that traffic is the “best measure of brand health”, the lack of urgency in attacking the problem has been striking. Traffic has been an issue at Darden since 2008. The company generates a billion dollars in operating cash flow, annually. Like McDonald’s, the company should be able to out-muscle the competition over the long-term. Instead, the company has been a long-term under-performer; we believe that shareholders are likely at the limit of their collective patience. The charts below show little evidence of “urgent action” on the part of management.

Statistics and Statistics

“And so we talked about the period from fiscal 2008, our fiscal 2008 through fiscal 2012, with industry decline cumulatively of 20%; and our brands declining about half that, 10%. And that's an issue we've got to address. And so we need to do what we need to do from a guest experience perspective, both affordability and the things that we're delivering, to really reverse that.”

In the investment research business, half-truth and bias are prevalent in narratives presented by parties of all kinds – management teams not excluded! During Friday’s earnings call, DRI highlighted that during the period FY08-FY12, the company’s brand’s experienced a cumulative decline of roughly 10% versus the industry decline of 20%. While this statistic is true, we don’t believe that FY08-FY12 is the only period over which Darden’s performance should be judged. Firstly, the recession is not the sole factor in Darden losing traffic over the past five-to-six years. A diminishing value proposition at Olive Garden is just one of the other factors to consider, as well as an over-reliance of promotions at Red Lobster which has led to wildly inconsistent results. The company has released data through FY13 that, depending on the date range one indexes it over, can tell a wide variety of stories.

A clearer indication of most recent traffic trends at Darden, and across the industry, is arrived at by considering two-year average trends. As the charts, above, illustrate, traffic at Darden’s most important two brands (80% of revenue) are stagnating in negative territory on a two-year average basis. We encourage investors to be wary of the notion that Darden’s core concepts have seen a traffic recovery, as some of the questions from the sell-side implied during the earnings call.

The False Promise of the Portfolio Restaurant Company

“We're confident that the Specialty Restaurant Group is working on the right things to achieve our long range growth targets, and we're well-positioned to take full advantage of all of Darden has to offer, including robust supply chain, information technology, consumer insights, finance and other capabilities, and make significant contributions to Darden's sales and earnings growth.”

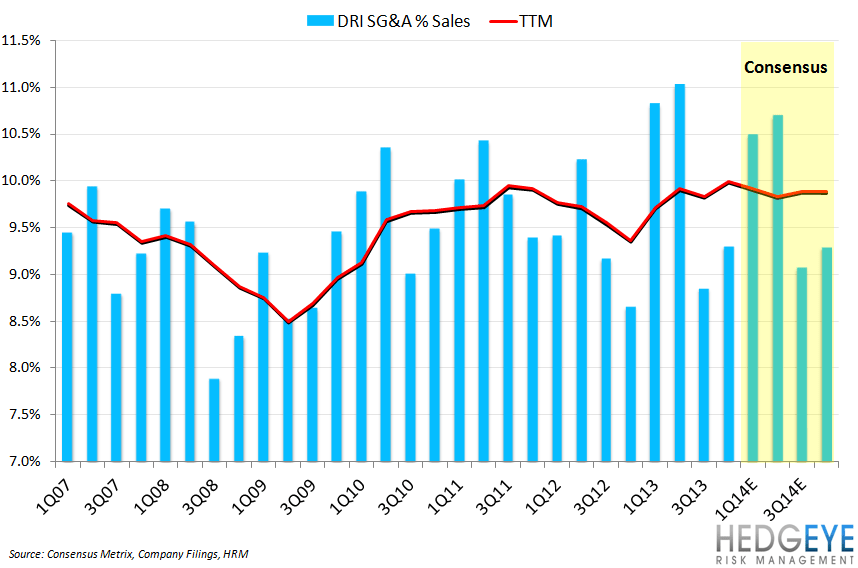

Darden’s management team has, for years, been describing the supposed virtues of the “portfolio” business model. We believe that the best test of that idea is the company’s stock price, which has underperformed rival stock Brinker and the broader XLY since it began its “diversification” strategy in August 2007, when it acquired LongHorn Steakhouse parent RARE Hospitality International.

Comparing Darden’s and Brinker’s respective operating margins also tells a story. Brinker has simplified its portfolio as Darden has added to its own. Despite the general belief that “scale” and “a robust supply chain” will improve profitability, we see below that the opposite may actually be true. Darden’s G&A expense, as a percentage of sales, has not demonstrated the leverage over time that believers in the “portfolio” business model would expect.

Payout Ratio

“Given the diluted net EPS, we expect in fiscal 2014, which I'll talk more about later, this equates to a payout ratio on a forward basis of approximately 70%. While this is above the 40% to 50% payout range we've discussed before, we're in the process of reviewing our target range and will likely take it higher sometime later this year.”

The prudent company raises dividends in line with earnings growth to maintain a stable dividend payout ratio. From 2008 to 2010, DRI was able to grow its dividend at an accelerated rate to play catch up with a more appropriate payout ratio. For the past two years, we are unsure as to why DRI continued to raise the dividend at a rate inconsistent with the fundamentals of the company. Now management wants to change its target dividend payout range. Why did management feel the need to raise the dividend given the deceleration in earnings growth?

What message is management sending to shareholders and the rating agencies? There is no creditable evidence that management has fixed the business and is on a path of improving the multi-year decline in traffic. As a result, the company’s margins and returns are in a decline.

Given the secular decline in the fundamentals of the company, Darden cannot responsibly maintain a payout ratio of 70%. Doing so is, to us, a sign of weakness not strength. Given the company’s significant capital spending needs, Darden is expected to generate only $80 million in free cash flow in FY14. A meaningful deceleration in comps and margins could lower that number substantially, possibly impeding the company from generating enough cash flow to cover the dividend.

Howard Penney

Managing Director

Rory Green

Senior Analyst