TODAY’S S&P 500 SET-UP – June 25, 2013

As we look at today's setup for the S&P 500, the range is 26 points or 0.45% downside to 1566 and 1.20% upside to 1592.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.13 from 2.15

- VIX closed at 20.11 1 day percent change of 6.40%

MACRO DATA POINTS (Bloomberg Estimates):

- 7:45am: ICSC weekly sales

- 8:30am: Dur Goods Orders, May, est. 3.0% (prior rev to 3.5%)

- 8:30am: Durables Ex Transportation, May, est. 0.0%

- 8:30am: Cap Goods Orders Non-Def, Ex-Aircraft, May, est. 0.5%

- 8:55am: Johnson/Redbook weekly sales

- 9am: S&P/Case Shiller 20 City M/m, April, est. 1.2%

- 9am: S&P/CS Home Price Index, April (prior 148.65)

- 9am: FHFA House Price Index, April, est. 1.1% (prior 1.3%)

- 10am: Richmond Fed Manufacturing, June, est. 1 (prior -2)

- 10am: Conference Bd Cons Conf, June, est. 75 (prior 76.2)

- 10am: New Home Sales, May, est. 460k (prior 454k)

- 10am: New Home Sales M/m, May, est. 1.3% (prior 2.3%)

- 11am: Fed to buy $1.25b-$1.75b debt in 2036-2043 sector

- 11:30am: U.S. to sell $25b 52W bills, 4W bills

- 1pm: U.S. to sell $35b 2Y notes

- 4:30pm: API weekly inventory data

GOVERNMENT:

- President Obama unveils his plan to address climate change

- Supreme court may rule at 10am on cases including:

- Calif. initiative banning same-sex marriage, law denying federal benefits to legally married gay couples

- Whether Voting Rights Act can require some states to get “preclearance” from federal government before changing voting rules

- Markey takes on Gomez in Mass. special election for U.S. Senate

- Sperling, Krueger, Biden speak on federal minimum wage

- Senate Appropriations Cmte panel marks up FY2014 Energy and Water Development Appropriations Bill, 10am

- Senate Energy and Natural Resources Cmte holds hearing on management of forests on federal lands, 10am

- Senate Appropriations Cmte Financial Svcs and General Government panel hears from CFTC Chairman Gary Gensler, SEC Chairman Mary Jo White on FY2014 budget, 3pm

- Senate Banking, Housing and Urban Affairs Cmte holds hearing on regulation of private student loans, 10am

WHAT TO WATCH

- Google may get win in case over privacy data on other websites

- U.S. senators to introduce bill to end Fannie Mae, Freddie Mac

- China money-market rate increase temporary, PBOC official says

- Benchmark rate alternatives to be studied by regulators: Carney

- U.S. said to explore possible Chinese role in Snowden leaks

- Men’s Wearhouse founder Zimmer said studying options: Reuters

- S&P mortgage ratings trial sought for Feb. 2015 by U.S.

- Ford F-150 tops Toyota Camry as No. 1 in American-made ranking

- Cerberus plan to boost Seibu control rejected by investors

- Spain sells EU3.07b bills vs EU3b maximum target

EARNINGS:

- Lennar (LEN) 6am, $0.33, preview

- Walgreen (WAG) 7:30am, $0.91

- Barnes & Noble (BKS) 8:30am, ($0.90)

- Carnival (CCL) 9:15am, $0.07

- Synnex (SNX) 4pm, $0.81

- Apollo Group (APOL) 4:01pm, $0.86

- Smith & Wesson (SWHC) 4:05pm, $0.43

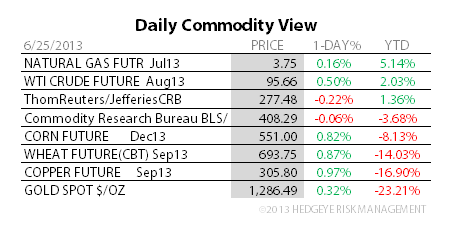

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- HKEx’s Li Targets Chinese Growth After $2.2 Billion LME Purchase

- Palm Reserves Rising Most Since 1999 After Oil Rout: Commodities

- Morgan Stanley to Goldman Cut Gold Forecasts on Fed Outlook

- Copper Advances in New York After China Comments on Money Rates

- EU Officials Said to Agree to 30% Cap on Some Farm Subsidy Cuts

- Corzine May Soon Face CFTC Lawsuit Over MF Global, NYT Reports

- Morgan Stanley Maintains 3Q, 4Q Iron Ore Price Estimates

- Iron-Ore Cargoes Double Ship Rates as China Seen Buying: Freight

- WTI Rises a Second Day on Supply Data; Goldman Sees Demand Gain

- Crude Supply Drops in Survey Amid Driving Season: Energy Markets

- Yingluck Risks Farmer Ire to Curb Fiscal Burden: Southeast Asia

- Corn Belt ’Good or Excellent’ Corn Hits Seven-year High, Week 25

- Gold’s Price Slide Seen by Credit Suisse ‘Shattering’ Confidence

- Russia, Kazakhstan Join Turkey in Raising Gold Holdings in May

CURRENCIES

GLOBAL PERFORMANCE

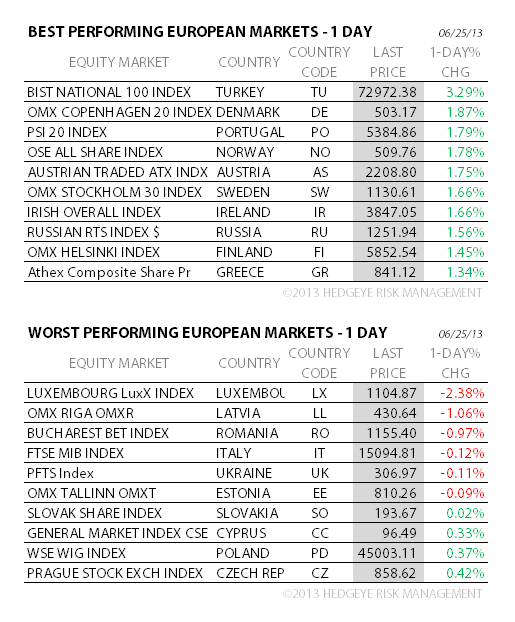

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team