Key Takeaways:

We've been flagging rising risk for 3 weeks now. Risk measures are showing signs of accelerating deterioration on many fronts, both by asset class and by geography. Swaps at the global sovereign and global banking level continue to go the wrong way. Interestingly, systemic banking system gauges like TED Spread and Euribor-OIS, remain benign. High Yield continues to get demolished. Keep an eye on HY - we won't see a let up in pressure until HY stabilizes.

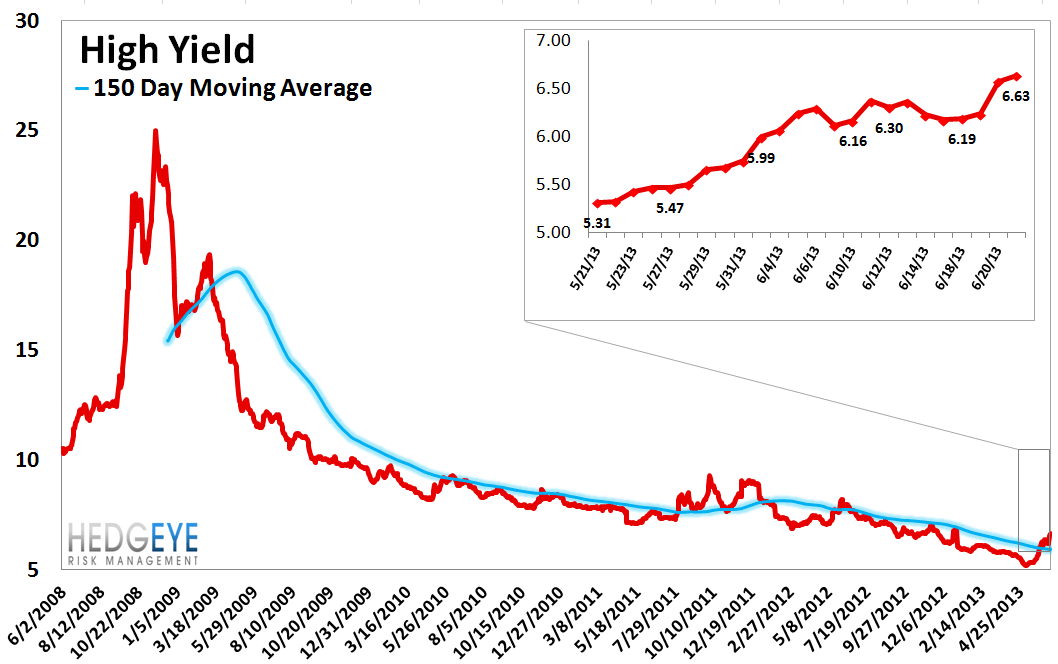

* High Yield – Still our preferred primary risk gauge, High Yield rates rose another 40.6 bps last week, ending the week at 6.63% versus 6.23% the prior week. Not only is the trend still moving higher, the rate of change is accelerating.

* Asian Financial CDS - Chinese banking horror show. The three Chinese financials we track, Export-Import Bank of China, Bank of China, and China Development Bank, all widened 67-72 bps week-over-week (a 58-62% move). While the level of swaps is still low, the size of the move is unprecedented. For reference, swaps have roughly doubled in the past month for all three of these banks. Meanwhile, over in India, the blast-off continues. State Bank of India widened a further 38 bps week-over-week, bringing the MoM move to 88 bps (+49%).

* XLF Macro Quantitative Setup – Our Macro team’s quantitative setup in the XLF shows the intermediate term TREND line of support at $18.87, which is 1.3% below Friday's close. This is a key support level to watch (which is currently being tested with the XLF at $18.79 as of 9:45).

* Markit MCDX Index – Last week spreads widened 22 bps, ending the week at 106 bps versus 84.4 bps the prior week. Muni swaps continue to widen aggressively. Swaps have now widened by 63 bps off their May 3 low of 43 bps.

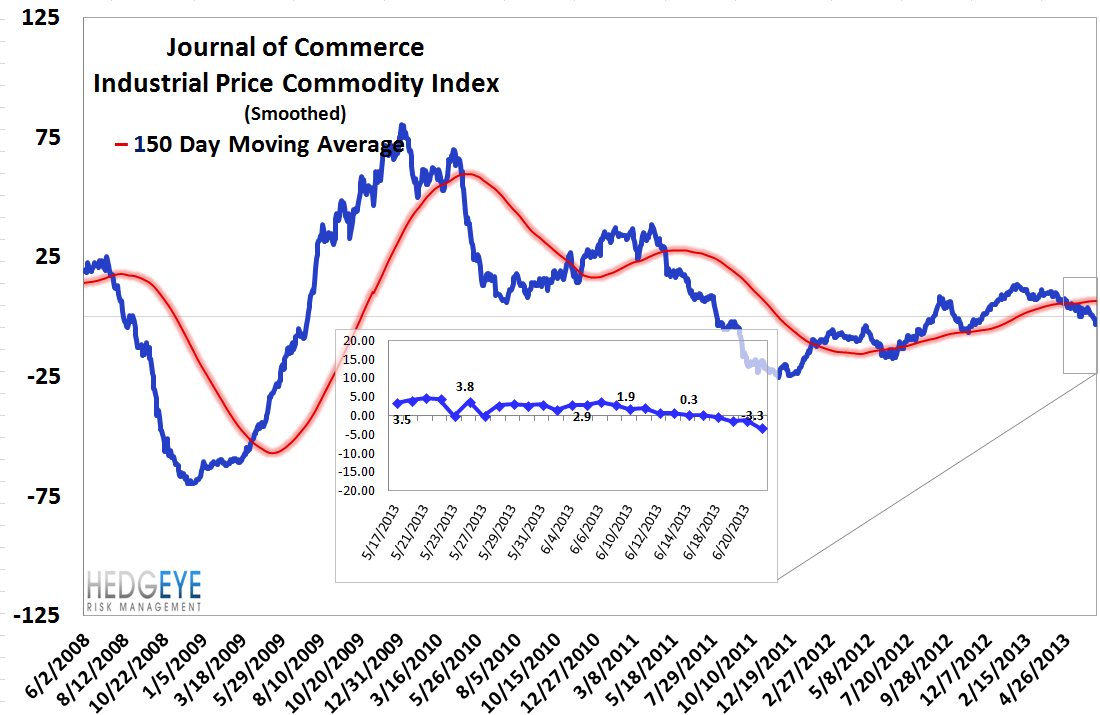

* Journal of Commerce Commodity Price Index – The JOC index fell -4.0 points, ending the week at -3.29 versus 0.8 the prior week. Commodity prices are falling at the fastest rate we've seen in a long time, both causing and reflecting the growing rout in emerging markets and China.

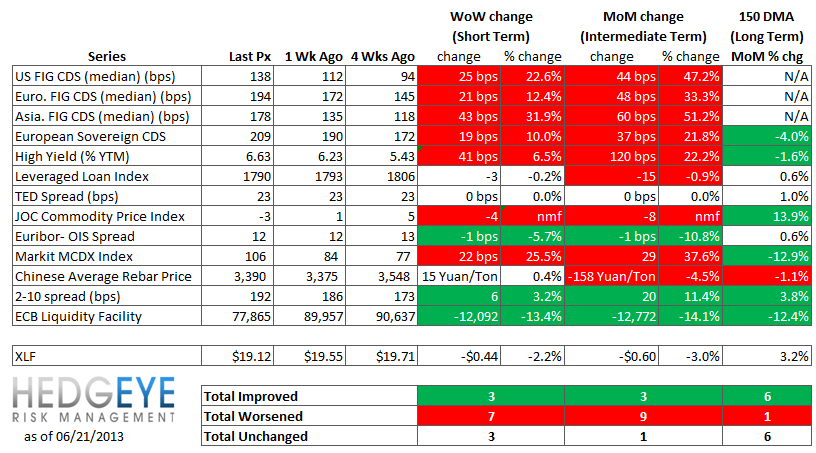

Financial Risk Monitor Summary

• Short-term(WoW): Negative / 3 of 13 improved / 7 out of 13 worsened / 3 of 13 unchanged

• Intermediate-term(WoW): Negative / 3 of 13 improved / 9 out of 13 worsened / 1 of 13 unchanged

• Long-term(WoW): Positive / 6 of 13 improved / 1 out of 13 worsened / 6 of 13 unchanged

1. U.S. Financial CDS - BBQ-central. U.S. Financial swaps are getting absolutely roasted. MS and GS widened by 37 and 31 bps, respectively, last week, followed by BofA (+27 bps). Mortgage insurers, MTG and RDN, widened by 69 and 44 bps.

Widened the least WoW: AON, SLM, RDN

Widened the most WoW: PRU, MBI, MS

Widened the least WoW: UNM, AON, WFC

Widened the most MoM: MBI, BAC, MS

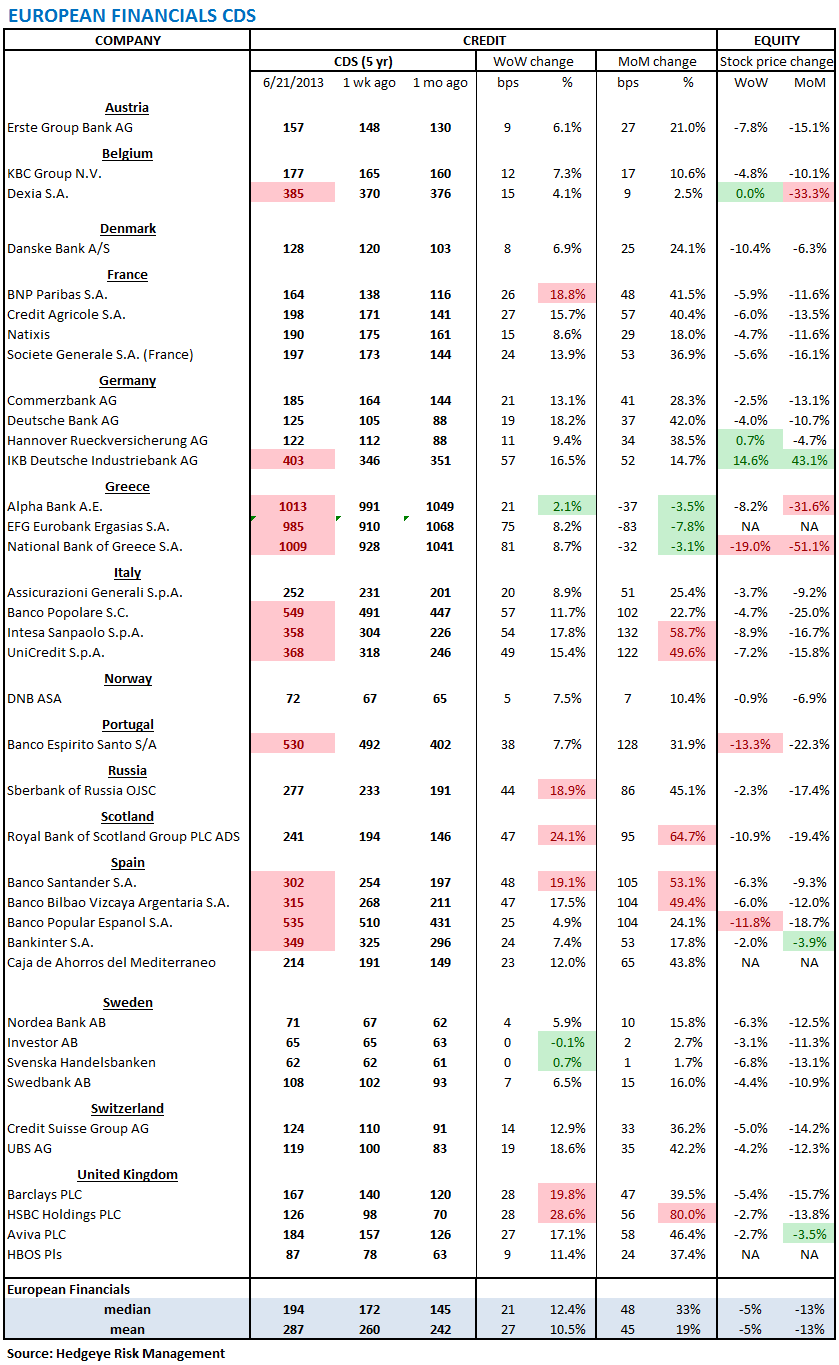

2. European Financial CDS - The good news is, the systemic gauge of EU banking system risk, Euribor-OIS, remains benign. The bad news is, individual company swaps look awful. The table below speaks for itself, but we'd call attention to Sberbank of Russia (+44 bps WoW), RBS (+47 bps WoW), and the UK banks.

3. Asian Financial CDS - Chinese banking horror show. The three Chinese financials we track, Export-Import Bank of China, Bank of China, and China Development Bank, all widened 67-72 bps week-over-week (a 58-62% move). While the level of swaps is still low, the size of the move is unprecedented. For reference, swaps have roughly doubled in the past month for all three of these banks. Meanwhile, over in India, the blast-off continues. State Bank of India widened a further 38 bps week-over-week, bringing the MoM move to 88 bps (+49%).

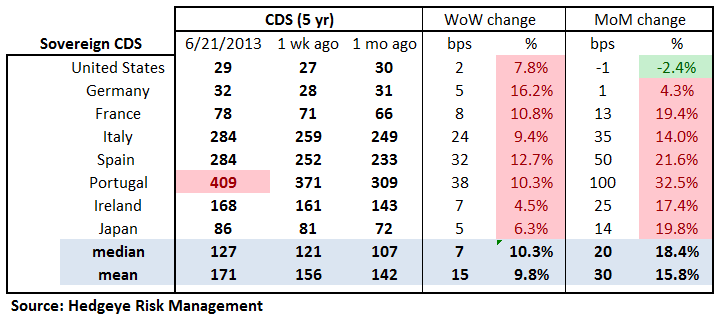

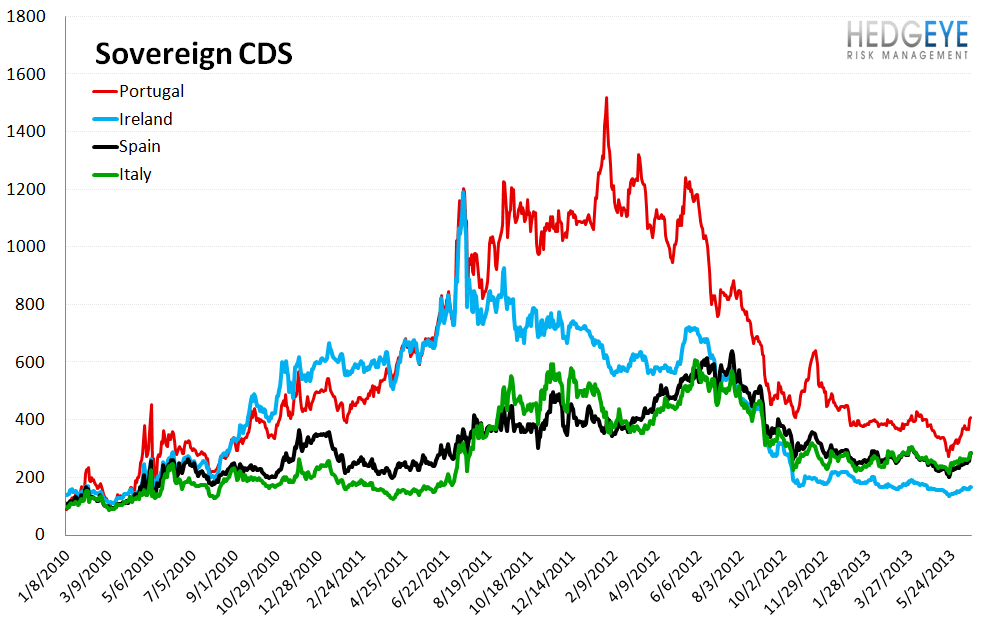

4. Sovereign CDS – Sovereign swaps widened across the board last week. Italy, Spain and Portugal blew out by 24, 32 and 38 bps, respectively to 284, 284 and 409 bps. Meanwhile, Japan widened a further 5 bps to 86 bps, Germany widened 5 bps to 32 bps and the U.S. added 2 bps to 29 bps.

5. High Yield (YTM) Monitor – High Yield rates rose 40.6 bps last week, ending the week at 6.63% versus 6.23% the prior week.

6. Leveraged Loan Index Monitor – The Leveraged Loan Index fell -3.1 points last week, ending at 1790.14.

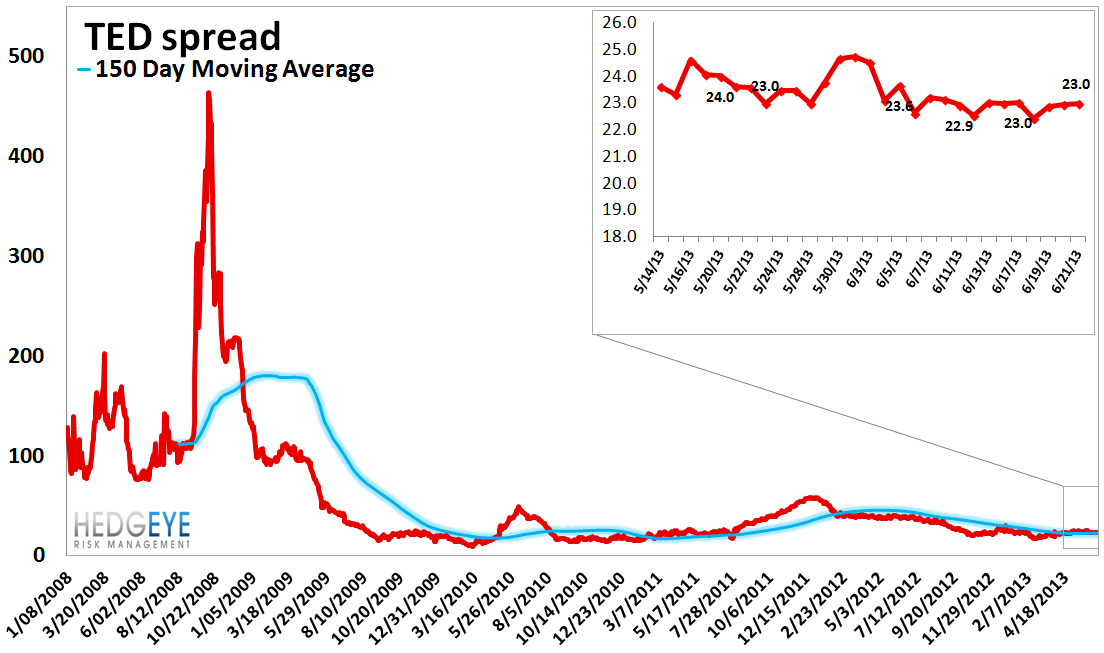

7. TED Spread Monitor – The TED spread was flat last week at 23 bps. As with Euribor-OIS, its EU cousin, systemic risk gauges for U.S. financials remain calm for now - a good thing.

8. Journal of Commerce Commodity Price Index – The JOC index fell -4.0 points, ending the week at -3.29 versus 0.8 the prior week. Commodity prices are falling at the fastest rate we've seen in a long time, both causing and reflecting the growing rout in emerging markets and China.

9. Euribor-OIS Spread – The Euribor-OIS spread tightened by 1 bps to 12 bps. This is another token silver lining to the current maelstrom. European spreads are at least contained from a systemic standpoint. The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk.

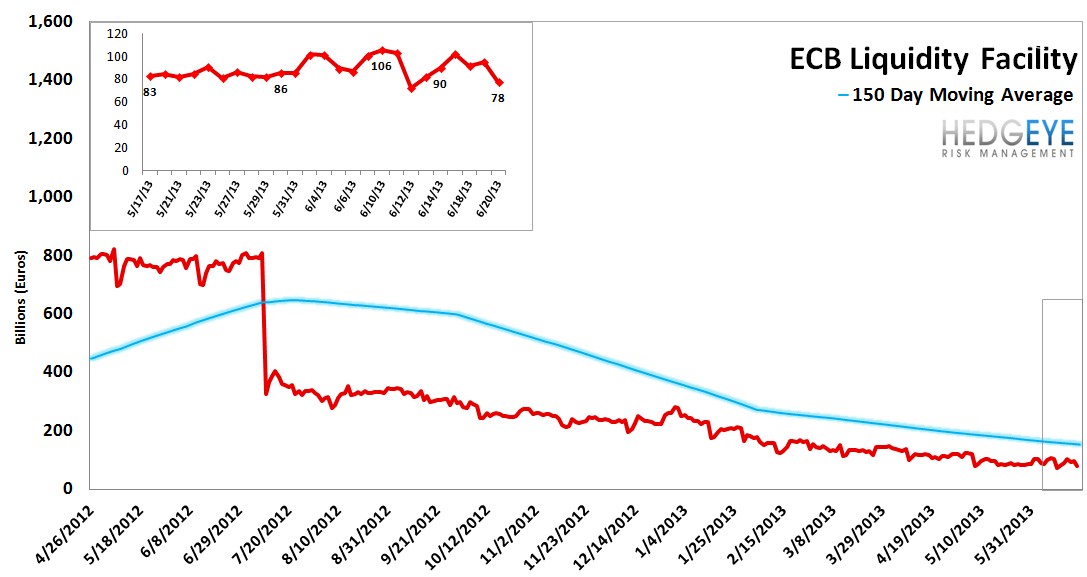

10. ECB Liquidity Recourse to the Deposit Facility – Deposits were down another 12 billion Euros last week, signaling relative calm in the European financial system (relative vs. rest of world). The ECB Liquidity Recourse to the Deposit Facility measures banks’ overnight deposits with the ECB. Taken in conjunction with excess reserves, the ECB deposit facility measures excess liquidity in the Euro banking system. An increase in this metric shows that banks are borrowing from the ECB. In other words, the deposit facility measures one element of the ECB response to the crisis.

11. Markit MCDX Index Monitor – The Markit MCDX is a measure of municipal credit default swaps. We believe this index is a useful indicator of pressure in state and local governments. Markit publishes index values daily on six 5-year tenor baskets including 50 reference entities each. Each basket includes a diversified pool of revenue and GO bonds from a broad array of states. We track the 16-V1. Last week spreads widened 22 bps, ending the week at 106 bps versus 84.4 bps the prior week.

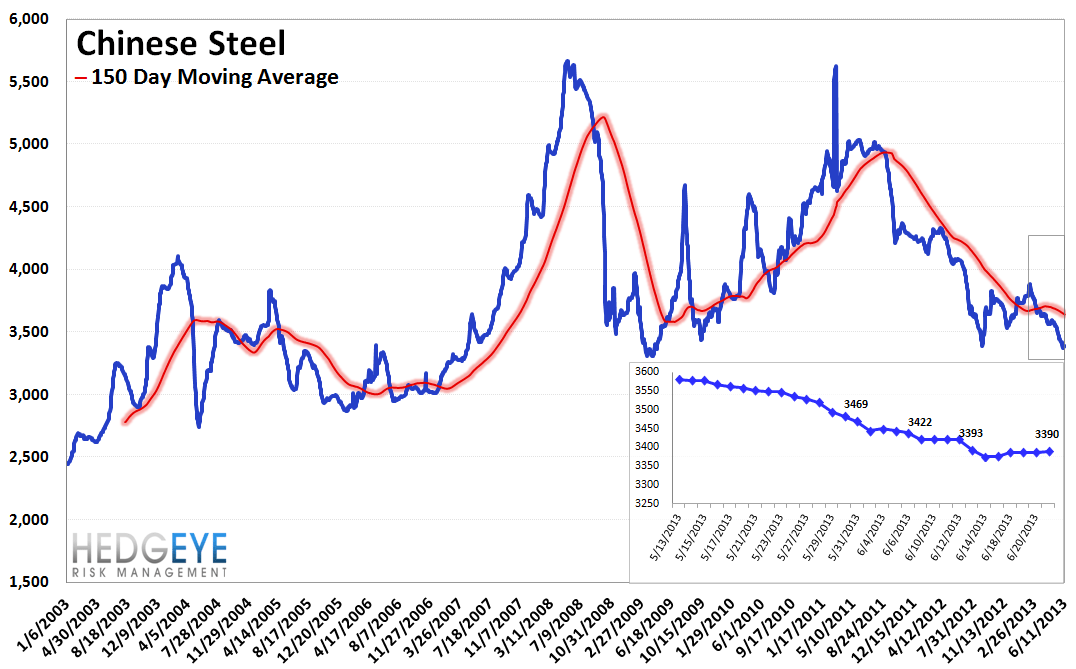

12. Chinese Steel – Steel prices in China rose 0.4% last week, or 15 yuan/ton, to 3390 yuan/ton. Notwithstanding this small week-over-week improvement, Chinese steel prices are down 4.5% in the past month and are trending steadily lower. We use Chinese steel rebar prices to gauge Chinese construction activity, and, by extension, the health of the Chinese economy.

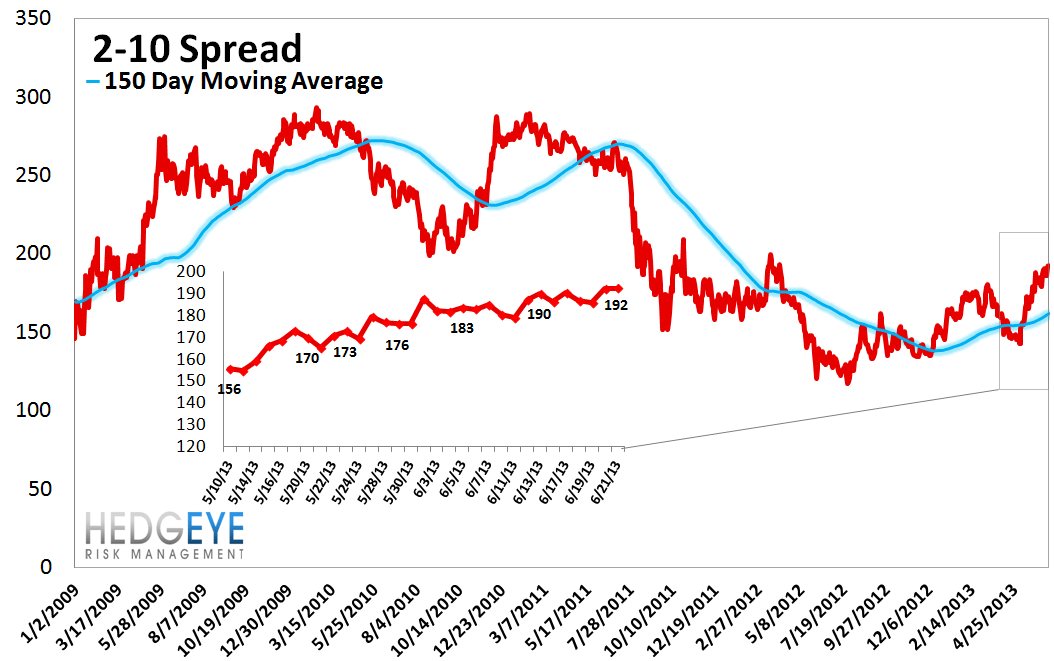

13. 2-10 Spread – Last week the 2-10 spread widened to 192 bps, 6 bps wider than a week ago. This is one of the few silver linings to the current environment. We track the 2-10 spread as an indicator of bank margin pressure.

14. XLF Macro Quantitative Setup – Our Macro team’s quantitative setup in the XLF shows the intermediate term TREND line of support at $18.87, which is 1.3% below Friday's close. This is a key support level.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT