(Editor’s Note: We are removing Darden (DRI) from the list of our Investing Ideas. Please see our DRI update below.)

Investing Ideas Updates:

- DRI: We are removing removed Darden as one of our Investing Ideas. Restaurants sector head Howard Penney believes that Darden’s shares have further to fall, based on evidence from Friday’s earnings report and subsequent conference call. Penney adopted a bullish stance on DRI in March having been bearish on the stock since July 2012.

The bull case was comprised of two scenarios, either of which was sufficient, in March, to boost the stock considerably from the depressed levels where it was trading. The first was an improving economy, which implied accelerating Knapp Track comps that would most likely imply a sequential acceleration in Darden’s comps.

The second was the possibility of an activist emerging to shake up management and take advantage of what we saw as a company whose equity was trading below the value of the sum of its parts. Following the earnings release and conference call Friday, Penney believes neither scenario is likely from here. The stock has appreciated handsomely since the lows of the year and Penney believes that management is entrenched in the company and the fundamental performance of the company suggests that further downward revisions of fiscal year 2014 earnings are in play.

- FDX: Industrials sector head Jay Van Sciver got what he wanted when FedEx reported fiscal fourth quarter earnings this week. “FDX needed to show Express margin progress and the company delivered,” says Van Sciver, calling this a positive set-up heading into the core of FDX’s restructuring starting in the current fiscal year. FDX management sounded more positive than they have in recent calls when discussing their International Economy service, where results indicate that an asset light approach to those services are contributing meaningfully to profit margin improvement.

The Express division has reduced capacity and increased use of commercial aircraft belly space to meet demand for lower-cost options with better economics. Van Sciver says shareholders continue to get the Express divisionessentially for free, as it is not a meaningful constituent of the market value with its current low earnings. Going forward, Van Sciver is looking less for surprises, than for validation as FDX executes on its plan to expand margins. That’s why he was comfortable, and a bit amused, that management soft-pedaled guidance for next year. “In a long- term restructuring,” says Van Sciver, “it is much more attractive to progressively raise guidance than to cut/raise/cut/raise.”

Van Sciver sees significant upside in FDX and continues to believe it represents one of the best long-term investment opportunities in Industrials. (Please click here to see the latest Stock Report on FDX.)

- HCA: Health Care sector head Tom Tobin saw managed care stocks rise this week in the face of reports that May was a slow month for physician utilization. He says not to put undue emphasis on any single report, especially since the series of data that he tracks collectively suggests the opposite; signaling a “modest positive acceleration,” which should continue to be good for companies like HCA Holdings. On the Macro side, Tobin says “the relationship between the Fed’s tapering and the highly-indebted hospital stocks remains loose and uninteresting.”

In other words, the demographic shift towards more health care – driven by a gradually improving economy, improving employment trends, and accelerating new household formation and births – is a meaningful Macro factor and likely to lead to improving revenue and volume trends moving forward. Near-term market mayhem should not hamper this trend, even if it means slightly higher borrowing costs for hospitals down the road. (Please click here to see the latest Stock Report on HCA.)

- HOLX: Health Care sector head Tom Tobin has no update on Hologic this week. (Please click here to see the latest Stock Report on HOLX.)

- MPEL: Gaming, Leisure & Lodging sector head Todd Jordan remains bullish on Melco International Entertainment shares as average daily revenues at the Macau gaming tables jumped an unexpected 45% over the same period a year ago (and 39% week over week). Jordan says this latest report confirms a higher growth trend, and he now sees year over year growth that could hit 20% for June for industry wide gross revenues. And July looks like another strong month, so the momentum seems to be in place.

MPEL reaffirmed that it is on track to open its $1 billion Philippine casino operation by the middle of next year. Saying the project is already fully funded, MPEL says they will take advantage of all their connections in the region – including their “VIP database” of high rollers to make sure the opening of their Manila operation is a success. Jordan continues to like MPEL on current industry strength, and for significant expansion as its new operations come on line. (Please click here to see the latest Stock Report on MPEL.)

- NSM: Recent weakness in Nationstar can be attributed squarely to the back-up in interest rates, reflecting rising expectations for the Fed to taper. Is this justified? A substantial portion of NSM’s earnings come from mortgage origination, most of which is refinancing-driven. Traditionally, rising rates spell disaster for refinancing volume, so it’s not surprising to see Nationstar shares weak in the short-term.

The reasons we’re not overly concerned fundamentally are twofold. First, most of Nationstar’s refinancing business isn’t traditional refinancing at all, it’s HARP refinancing. HARP refinancing entails borrowers who are underwater and cannot refinance through conventional means because their LTV, or loan-to-value, ratios are too high to meet traditional underwriting criteria. The thing about HARP refinancing volume is that it is far less rate-sensitive than traditional refi volume.

That’s because a) these borrowers have no real options and b) many of these borrowers are at rates way above market rates anyway, so a 50-75 bps back-up in rates doesn’t sufficiently offset the kind of savings they can achieve by participating in HARP. Also, it’s important to realize that HARP activity has been quite low in the servicing portfolios that Nationstar has acquired, namely the Bank of America book.

Second, there is a benefit to mortgage servicers from rising rates. Mortgage accounting can be a bit confusing, but here’s a simple way of thinking about it. Mortgage servicing rights, or the MSR, are recorded as an asset on the balance sheet. The MSR is the present value of the future stream of income from servicing the portfolio of mortgages under contract. There are several things that can cause the value of this asset to fluctuate, one of which is interest rates. Rising rates make the asset more valuable because they reduce refinancing volume, which is the same as extending the life of the asset. Mortgage companies recognize changes in the value of the MSR asset as income or loss each quarter. As such, this rise in rates late in the quarter is likely to trigger a sizeable MSR write-up (that is, more income) for Nationstar.

Over the intermediate term we’ll get 2Q earnings results in just over a month and Steiner thinks it will be increasingly clear that NSM is less exposed to rising rates than the market thinks. (Please click here to see the latest Stock Report on NSM.)

- WWW: Retail sector head Brian McGough followed-up with management of top pick Wolverine Worldwide to discuss the status of its current business transformation. The quick takeaway – which should surprise no one – is that there is still a ways to go before the acquisitions are fully digested, before all the cost efficiencies are realized, and before the company can state definitively how close to their original profitability targets the consolidated operation will be. That said, the company appears on track to implement SAP into its newly-acquired brands, which is an important milestone WWW should hit this summer and will be the base upon which it can scale International expansion.

Certain uncontrollable factors affect their growth – two years of horrible weather in Europe hurt sales, and the self- inflicted slip in sales in Merrell’s Active Lifestyle division. But McGough says WWW continues to make the right kind of progress where it counts, restructuring their Merrill division by outdoor activity category, rather than gender, for example, in response to clear consumer preferences.

And they are just starting on realizing manufacturing efficiencies from the consolidation of a broad range of brands. McGough says the transition will take time, and that working through it will be a drag on results for the balance of 2013. Twelve to 18 months out, says McGough, the numbers should reflect a whole new reality, and ultimately, McGough thinks estimates are too low. WWW remains a top pick in the Retail space. (Please click here to see the latest Stock Report on WWW.)

Macro Theme of the Week: Bernanke Leads, Follows, and Gets Out of the Way

Ben Bernanke’s already stayed a lot longer than he wanted or he was supposed to.

- President Obama

Scientists observing bird flight patterns tell us the lead goose in the migratory V-pattern switches back and forth between looking ahead, and looking back. It constantly checks the formation behind and adjusts its position to make sure it remains at the point of the flock. Periodically, the lead goose swerves out and another moves up to replace it, going through the same drill of lead, reposition, lead, and reposition.

President Obama made noises this week about Bernanke’s future, comments which are being read as a clear signal that Bernanke will leave the Fed when his current term expires. Hot speculation was set off when President Obama said Bernanke has been on the job “longer than he was supposed to.” Will Bernanke be fired? Will he be allowed to serve out his term? Is he in the Presidential dog house? Commentators are furiously connecting the dots as pundits smack themselves on the forehead saying, We shoulda known when Bernanke failed to show at this year’s global central bank confab at Jackson Hole, Wyoming. What could all this mean?

Bernanke’s term as Fed Chairman runs through January 31, 2014. His term as a member of the Federal Reserve Board ends January 31, 2020. Speculation aside, there seems little point in letting him go at this juncture (“Maybe President Obama didn’t look at his teleprompter when he made that remark,” one commentator mused.) President Obama is not up for re-election, and with the wheels of the economy grinding, it’s too late for someone else to step in and take either credit or blame.

Of course there are those who wish he’d never gotten the appointment in the first place. Hedgeye has taken exception with Bernanke’s policies from the beginning – starting well before him. Bernanke is in many respects not a leader, but rather a follower of the Greenspan-Henry Paulson-Tim Geithner school of coddling the rich. We have been firmly in favor of a Volcker-like jolt, one that pushes all the pain into a short time frame, then gets it out of the way. At the same time we wish to state for the record that we have tremendous admiration for Mr. Bernanke’s intelligence, for his dedication, and for the profound commitment he has brought to his stint in public service. Serving as the appointed Head of Bloody Everything is a damned-if-you-do / damned-if-you-don’t proposition under the best of circumstances. It does not take a Princeton PhD to recognize that Mr. Bernanke has not been faced with the Best of Circumstances.

The question remains, though, how much of that is his fault?

Bernanke’s approach has been to stimulate the financial markets, and with them the major banking and financial firms. It is not clear to us that Bernanke ever believed the multiple trillions of dollars in guarantees, free profits on Treasury spreads, and actual cash handouts were ever going to turn into actual loans to America’s businesses. Bernanke’s read of the Great Depression – a topic on which he is famously a world-renowned expert – is that the government did not do nearly enough. And history may in fact judge him in a positive light. In a society with so many freedoms tugging at the strings of policy – and with such a compromised and conflicted process driving both legislation and the regulatory process – it can’t be simple to manage the economy from the top down.

Or can it?

As Hedgeye CEO Keith McCullough has repeatedly observed, the most predictable and constant effect of government intervention is to increase volatility in the marketplace by accelerating economic cycles, rather than letting things play out in their own time. We do not know how one measures societal pain, but we have always been of the opinion that a Volcker-like short, sharp shock to the system would have been far healthier than the extended malaise we have lived through over nearly three presidencies.

We think the next president may want to consider a substantive shift in policy. The Fed does not need an economist to run it. It may not even need someone with a deep understanding of the financial markets. Increasingly, as our elected government has abdicated its responsibility for decision making, the nuts and bolts of running the economy has been handed over to appointed experts. Perhaps the Fed needs to be run like a business. Perhaps the Fed needs someone with experience meeting operating budgets, hiring and managing employees, and tracking flows in the economy to stay on budget. We never need to stay within a budget as long as we have unlimited access to the printing press. Maybe the next Fed chair should be the owner of a major plumbing supply house or a machine-tool shop.

Mr. Bernanke’s task has been made more difficult by the fact that major economies’ central banks are all pushing on the same accelerator. From Japan to Europe, printing presses are running ‘round the clock to create liquidity, in hopes it will stimulate the global economy. This has had the effect of making Bernanke’s QE “To Infinity and Beyond” what folks in the hedge fund world call a “crowded trade.” When one smart person buys a cheap stock, they can make money with it. When everyone piles into the same “smart idea,” two things happen: first, it drives the price to levels where there is no more profit to be made by the next buyer, and it sucks the liquidity out of the market, leaving holders with no one to sell to. In the ultimate Crowded Trade, the profits vanish and the next move is down. Usually way down. Usually with a thud.

In his testimony this week, Bernanke expressed himself as “surprised” that interest rates have edged up recently. This is not occurring in a vacuum. This week Keith writes “The last of the central planning bubbles left in the world is now popping. It’s called the bubble in super sovereign debt.” May we flatter ourselves to point out that Mr. Bernanke should have been subscribed to Hedgeye’s research?

The impenetrable aspect of the Fed policy game is that we don’t actually know what Chairman Bernanke thinks. The game is played as much with carefully-selected public utterances as with actual open market transactions to add liquidity. (We know there is also a theoretical policy option to decrease liquidity, but it has long been treated as hypothetical. Mr. Bernanke is like a driver who never learned that cars have brakes.)

Our take on Bernanke’s performance is that he acknowledges the markets are moving away from his ability to control them. QE or not QE is no longer the question. Having led from the front, checking market reactions assiduously along the way – and having apparently followed Americans’ most ardent policy desire by focusing on employment and housing – Mr. Bernanke is now trying to get out of the way gradually enough that the entire edifice does not collapse like a ten-story building into a vast sinkhole.

How Mean is the Mean?

Why all the fuss about a correction in the Treasurys market? We can be cynical (trust us, we’re good at it) or we can take news at face value.

Taking news at face value, the public policy read-through on Bernanke’s concern over rising rates is a blow to consumer confidence. Mortgage rates will edge up, they say, and people will be afraid to buy new homes, which will derail the economic recovery. Home ownership is one of two key psychological metrics of this nation’s health – the other being employment. An increase in Treasury rates flows directly through to the mortgage market, so the fear is that buying a home becomes more of a challenge.

In fact, a mild increase in rates will likely slow down some marginal home buying – private equity firms have already bought all the distressed housing stock they need, but some people who were considering trading up to better homes at bargain rates will probably defer those purchases.

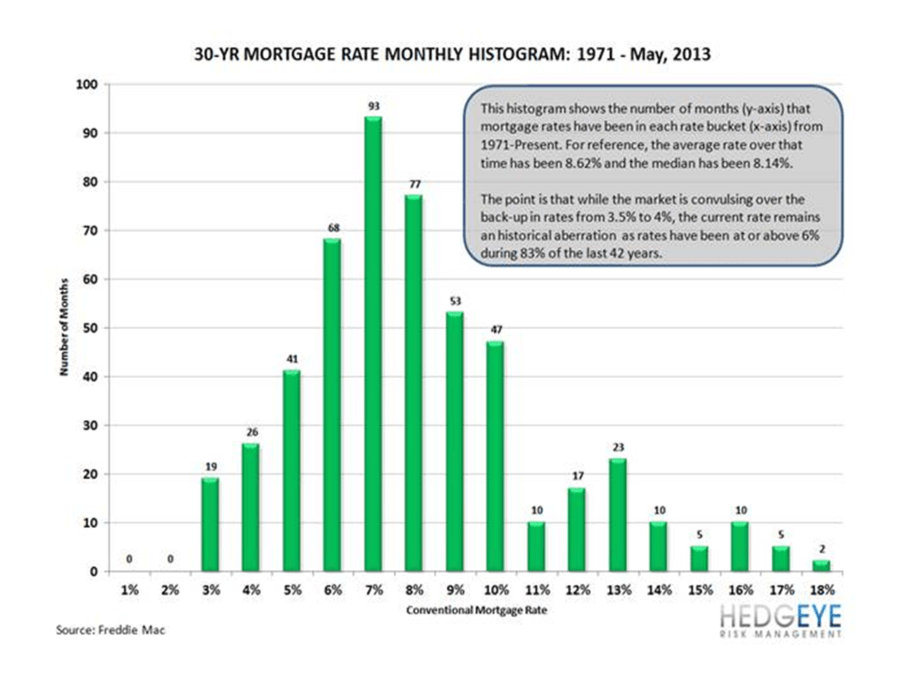

But our Financials sector head says the latest Census Bureau data on new household formation supports his thesis that the rate of new home construction could double to keep pace with rising demand. Steiner foresees a need for two million or more new starts per year, and while new families need to be frugal, they will not be deterred from buying their first home by 4%, or even 4.5% mortgage rates.

Selecting one number at random, here are comparable 30-year fixed-rate mortgage rates going back forty years:

May 1973 – 7.65%

May 1983 – 12.63%

May 1993 – 7.48%

May 2003 – 5.74%

May 2013 – 3.71%

Steiner provides a slide of average rates going back to 1971, the period covered in the Fed’s mortgage database.

The short takeaway is that, even with panic in the markets, the economy looks like it is recovering solidly, if slowly – and we keep reminding ourselves that the Stock Market is not the Economy. It wasn’t the economy when the market was on the way to all-time highs, and it still isn’t the economy now that it’s dropping in panic.

Reversion to the Mean, as we believe we are seeing in mortgage rates, is one of the most powerful forces we know and appears to be one of the few mathematical rules that actually keep happening over and over again. Economies are driven by human factors, but are understood through mathematics. Societal memory runs deep and occasionally surfaces when we pause for perspective. After the dust clears, today’s 30-year fixed rate mortgage at 4% will be seen as a bargain.

Fair or foul, what happens on Bernanke’s watch will become his legacy. Our guess is that, when the history of current economic policy is written, Mr. Bernanke will be credited with the positives that Hedgeye has been signaling of late: resumption of growth, strengthening of the dollar, newfound strength in the housing market, and a significant decline in unemployment. By the time Chairman Bernanke returns to the world of academia, our Health Care sector head Tom Tobin’s read on an upturn in the birth rate may have become common wisdom, so Bernanke will also get credit for a boost in confidence in the American Way of Life. Not a bad review.

Oh, and by the way…

Silly us! We almost forgot to give you the cynical view.

Chairman Bernanke seems genuinely perplexed that rates are edging up – some folks are criticizing him for being too up front about his confusion. Unless he’s acting. Since no one on Wall Street ever stops to ponder the possible consequences of their actions, markets are crashing left and right. Talk about a Crowded Trade, everybody is selling everything.

Mortgage rates at 4.24% have people concerned that the banks “need” more QE. Far be it from us to accuse an appointed official of pandering to Washington’s appetite for campaign contributions from Big Finance. As we go to press, economists are projecting the Fed will reduce QE from $85 billion a month to $65 billion in September – though with bond prices coming down, those dollars will buy more. You may accuse us of a lack of perspective but for our money – and it is our money – that’s still a lot. And Bernanke said they will re-invest what’s already on their books, which we read as a signal that the Fed balance sheet will not shrink and will remain with the risks of its gigantic mortgages portfolio. Bernanke continues to run the world’s largest long-only hedge fund.

Either way, nobody remembers anything on Wall Street. As we are seeing yet again, this produces constant opportunities for panic. And when you panic, two things happen: you lose money in your portfolio, and your banker gets paid.

Cynical enough for you?

Sector Spotlight: Slumdog Ex-Billionaire

Hedgeye senior Macro analyst Darius Dale did an in-depth presentation earlier this year sounding the alarm on the billions invested in Emerging Markets. If you are an Emerging Markets investor, we sincerely hope you were paying attention in April.

Bloomberg reports $3.9 trillion has been invested in Emerging Markets in the past four years. Talk about a Crowded Trade! (See “Investors are pulling money from emerging markets at the fastest pace in two years”) Needless to say, unrest in Turkey and Brazil is making matters much worse, much faster. When EM trades get crowded, they get really crowded. Brazil’s entire Bovespa equities market has a total capitalization of around one trillion $US, which leaves precious little liquidity for investors fleeing for the exits.

EM managers anticipate “crisis-like price actions without having a crisis.” This was the crux of Dale’s presentation: there is a difference between an “Investment Opportunity” and an “Opportunistic Investment.”

An Investment Opportunity is associated with strong fundamentals as investors look for that company with the “sweet spot” combination of a well-wrought business plan, outstanding management, a product or service with an identified need – in short, that Harvard B-School thingy called Competitive Advantage. The “Opportunity” is to ride the Up elevator as the company succeeds. The “Investment” bit is that the company is solid enough in all fundamental respects to make it worth the risk of holding it in your portfolio while waiting for the payoff.

In an Opportunistic Investment, an investor finds a company with a single distinct advantage in a product or service that is clearly cheaper than it normally is in the world market – usually something not of their own making, like a natural resource or a vast pool of low-paid labor. This was the case of all those billions invested in Brazilian oil and mining companies, and it was almost the entire case for China (all those people, and none of them have iPhones yet!)

Opportunistic Investing in the Emerging Markets has focused on cartels, many of them driven by what we would consider government corruption, and on state-managed capitalism. The relatively cheap price of such natural resources as oil – both onshore (Russia) and inaccessibly offshore (Brazil) – of iron ore (Brazil, as long as China was a willing buyer), and of the projected consumer power of lots and lots of people who haven’t yet attained even the minimum of the American standard of living (China, India). These investment have largely been made with minimal regard for the robustness of the companies’ management teams, internal processes, or finances – and still less concern over the ability of the local market to sustain stress through a robust democratic political structure, protection of minority rights, freedom of the press and the encouragement of popular debate and dissent.

A front-page case in point today is Brazil, where a million people are demonstrating over increasing prices and irresponsible government spending. To put this in perspective: Brazilians are so used to widespread corruption in both government and business that they are surprised when someone is not on the take. Brazilians tend to be jaded and passive about the widespread problems in their society, rather than outraged and motivated. Trust us, the demonstrations in the streets of over 100 Brazilian cities are a major event.

This signals that the concerns Emerging Market investors have largely ignored are now erupting with full force. Not least among these is the range of damaging economic effects of corruption and a society that, despite tremendous advances in the last twenty years, remains one of the most economically unequal on the planet. Officially, the Central Bank is struggling to keep inflation within its target range, capped at 6.5%. Unofficially – in figures not sent to overseas investors – the basket of consumer staples, including basic foodstuffs and public transportation, has inflated at rates between 10% and18% in Brazil’s major urban centers. Officially, Brazil is a free and open society that promotes equality. Unofficially, two million children aged 5-17 (more than 1% of the population of Brazil) work in unsafe and unsanitary jobs under conditions condemned by the ILO. Women earn significantly less than men, and dark-skinned Brazilians of African descent earn still less – while the indigenous earn essentially nothing at all.

Brazil has a free press, but on average one news reporter is murdered every year – the majority by professional killers or policemen – for investigating local corruption. The murderers are not often convicted – not least because police officers have also murdered judges assigned to corruption cases. Senior government officials – including members of congress and a member of the military joint chiefs of staff – have been directly tied to Brazil’s extensive network of drug traffickers.

On a less terrifying level, Brazil is hosting the 2014 soccer World Cup and the 2016 Olympic Games. It is woefully unprepared for either. Rio’s Maracana stadium, the proposed centerpiece of the global soccer tournament, was not completely ready when it opened this week for the Confederations Cup, the international competition that is the undercard for next year’s World Cup. Cost overruns took the budget for the Maracana renovation to one billion reais ($US 440 million). And even if FIFA does not cancel next year’s World Cup, Brazil’s airports and highways don’t have the capacity to accommodate the more than 500,000 foreigners expected to attend.

As of this writing, Brazilian president Dilma Rousseff is in meetings with cabinet officials, while bomb threats are being called in around government buildings. How’s your Opportunistic Investment working out?

By the way, in Turkey things are a lot worse.

Which brings us back to Chairman Bernanke, whose timing was perhaps dead on. With the darlings of the EM world imploding, America’s markets – even in a panic correction downdraft – look immeasurably better than any alternative. America may still be a long way from being a prime property, but we are still the best house in a bad neighborhood.

Investing Term: Yield Curve

The most common Yield Curve plots yields on 3-month, 2-year, 5-year and 30-year Treasury debt. For a simple definition, the Yield Curve measures interest rates over time for the same debt instrument, and the shape of the curve is a barometer for market sentiment. (Treasury debt issued with one year maturity or less are called Treasury Bills, or T-Bills. Treasury Notes have two to ten years’ maturity, while longer maturities are called Treasury Bonds.)

A Normal yield curve depicts lower yields demanded for short-term bills and notes, and higher returns for bonds. This implies that investors are concerned about the time value of future streams of interest payments, assuming an equal perception of risk across the maturities.

An Inverted yield curve has short-term yields higher than longer term ones. This happens when investors are selling their short-term debt (which drives the price down and the yield up) and buying longer term debt (which drives the price up, and the yield down). This means they don’t want to be in the market now, but are willing to predict today that the market will be safer in the future.

A Flat yield curve has rates very close together other across the range of maturities. This indicates general uncertainty and is seen as signaling a transition, though perhaps not a panic.

Financial theory has different ways of analyzing the Yield Curve.

The Pure Expectations hypothesis assumes that bonds, notes and bills are fungible – that is, they are equally substitutable for each other. This means they will be equally desirable across the range of maturities, and the difference in pricing reflects a consensus of expectations about future interest rates.

Opposite this are a range of theories that add a future liquidity premium to the time value of money calculation. At the end of the spectrum, market segmentation theories say that, even though the curve depicts yields on the same underlying security, demand for the security is unrelated at different maturities. This means the buyer of a two-year note does not consider a 30-year bond as a substitute for the note – the buyers of each maturity have a distinct set of needs that include return over time and future liquidity.

The yield curve is a guide for bond buyers, indicating current market sentiment about the bonds they are contemplating adding to their portfolio. Using the yield curve, you can calculate the projected future market price of the bonds you own today, to determine whether there is a projected capital gain, for example, or whether you should expect volatility in your portfolio.

And economists use the yield curve to make predictions about the economy. According to the National Bureau for Economic Research, every recession in the US between 1 has been preceded by an inverted yield curve – and every inverted yield curve has been followed by a recession.

This 1.000 batting average begs the question of whether the inverted yield curve has become a self-fulfilling prophecy, leading economists to push recessionary policy moves. Confusing, huh? You might as well ask whether Mr. Bernanke says what he says because it moves the markets, or the markets move because Mr. Bernanke says what he says.