We no longer see Darden as one of the most attractive longs in the space as soft traffic and confusing statements from the management team make it difficult to remain behind the stock. We are removing it from our Best Ideas list as of today. Given today's results and conference call, we can no longer defend the long case.

Conclusion

On today’s evidence, we believe that Darden’s shares have further to fall. We adopted a bullish stance on DRI in March having been bearish on the stock since July 2012. The bull case was comprised of two scenarios, either of which was sufficient, in March, to boost the stock considerably from the depressed levels it was trading at. The first was an improving economy, which implied accelerating Knapp Track comps that would most likely imply a sequential acceleration in Darden’s comps. The second was the possibility of an activist emerging to shake up management and take advantage of what we saw as a company whose equity was trading below the value of the sum of its parts. Following the earnings release and conference call today, we believe neither scenario is likely from here. The stock has appreciated handsomely since the lows of the year and we believe that management is entrenched in the company and the fundamental performance of the company suggests that further downward revisions of FY14 earnings are in play. While we have called out the deficit of leadership in Orlando, as well as the activist thesis that we see as attractive to those active in the space, it seems as though change will not be as forthcoming as we previously thought.

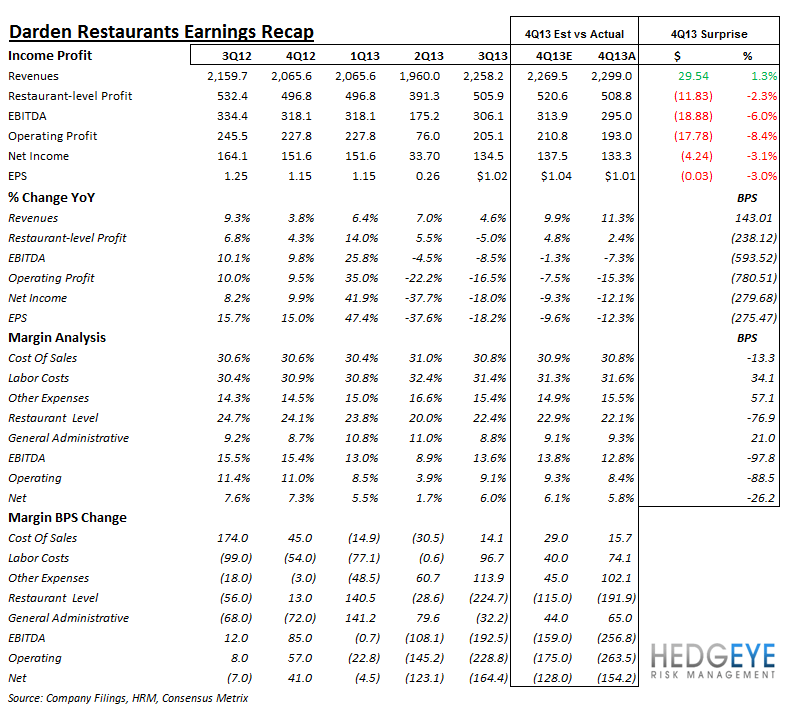

4QFY13 Recap

The primary takeaway from the quarter is that traffic trends at Olive Garden and Red Lobster remain soft and management seems to have little in its arsenal to rectify that situation. CEO Clarence Otis stated that traffic is the ultimate measure of brand health and blamed Darden’s weak comps on the macro economy, even offering a U.S. GDP growth estimate for 2013.

The company lowered FY14 EPS growth expectations and Blended “Big Three” same-restaurant sales guidance for the next four quarters.

Big Promises from the Top

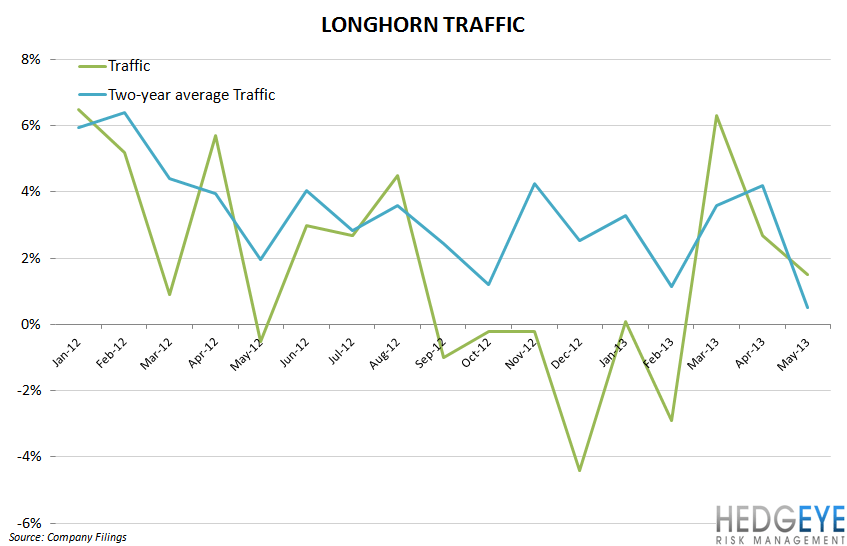

Darden’s leadership deficit continues to grow. We were surprised to hear Clarence Otis tout the company’s positive traffic growth on CNBC this morning. While the company did register positive traffic, the traffic comparison was favorable and the two-year average trend at each of the “Big Three” concepts tells a distinctly different tale to what Otis was communicating. The sequential deceleration in two-year average trends in May, despite an easier compare, suggests that the underlying trend weakened into the end of the fiscal year.

Capital Intensity a Key Point

While the capital intensity of Darden’s business model has been decreasing, what is more relevant for a restaurant company is the relationship between capex growth and EBITDA growth. In this instance, we see, below, that Darden’s EBITDA growth is decelerating precipitously. Guiding to higher FY14 cash flow from operations on lower net income is raising the bar too high, in our view.

Howard Penney

Managing Director

Rory Green

Senior Analyst