Below is the breakdown of this morning's claims data from the Hedgeye Financials team. If you would like to setup a call with Josh or Jonathan or trial their research, please contact .

Fool Me Thrice

We've always been fond of our friend Peter Atwater's use of "The Lady or the Tiger" metaphor to contextualize different market dynamics, and the current setup in the labor market seems to us sufficiently apropos. In this case, the market thinks it's getting the Tiger, but in reality it's getting the Lady. In short, the labor market is now a total mirage.

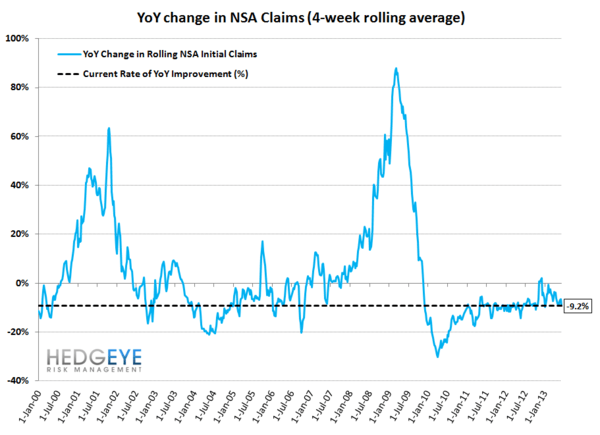

The non-seasonally adjusted data is improving at the fastest rate we've seen year-to-date. NSA 4-wk rolling initial jobless claims are today 9.2% lower than at the same point last year. To reiterate, that's the fastest rate of improvement we've seen this year. We show this in the second chart below.

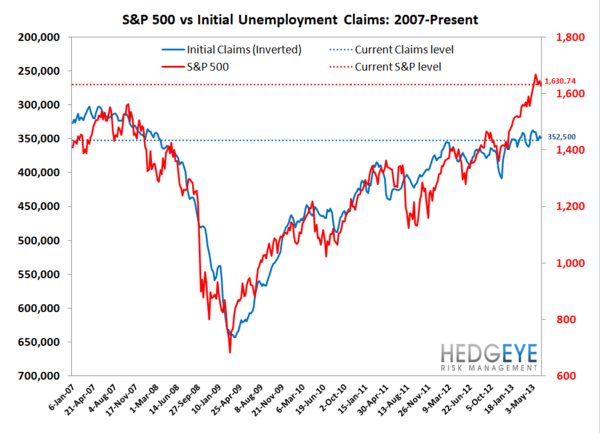

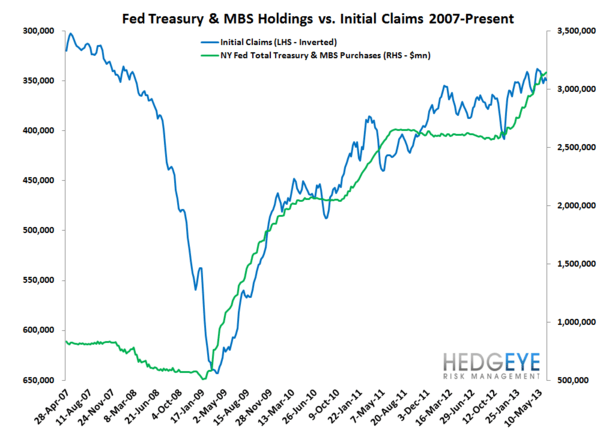

Meanwhile, the SA (seasonally-adjusted) data is showing total stagnation. The slope of the curve (the trend line) for SA claims since the start of March is now flat, as the first chart below shows. The interesting dynamic is that the labor market appears to be stagnating at the same time that the Fed is ratcheting up expectations for withdrawing support. This is almost identical to the setup we've seen in the prior three years. #PatternRecognition.

The takeaway is that over the short to intermediate term we would expect weakness in the sector to continue. As a reminder, our simple model for thinking about the [Financials] sector revolves around three core tenets: labor, housing and the Fed. All three fronts are now under seige. 1. Tapering expectations are shifting rapidly. 2. The SA labor market data (the headfake) is stagnating. 3. Housing data remains very strong, but the swift backup in rates is raising fear about the sustainability of the recovery. At a minimum, it's pointing to a deceleration in the rate of recovery.

Taking a longer-term view, we see the setup as very favorable. The labor market is indeed improving rapidly. The Fed will likely be sucked back into the market by a) the rise in rates, and b) the perceived deceleration in the labor market, and c) (most importantly) by the selloff in equities. Housing remains a Giffen, so rising prices will continue to self-reinforce.

We published a note in mid-April entitled "Beware the Ides of April", which was a sector-based risk management snapshot of how every name in the sector responded to the last go-around of perceived Fed exit/labor market deterioration. We'll be publishing a redux of that note this morning.

The Data

Prior to revision, initial jobless claims rose 20k to 354k from 334k WoW, as the prior week's number was revised up by 6k to 340k.

The headline (unrevised) number shows claims were higher by 14k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims rose 2.5k WoW to 349.25k.

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -9.2% lower YoY.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT