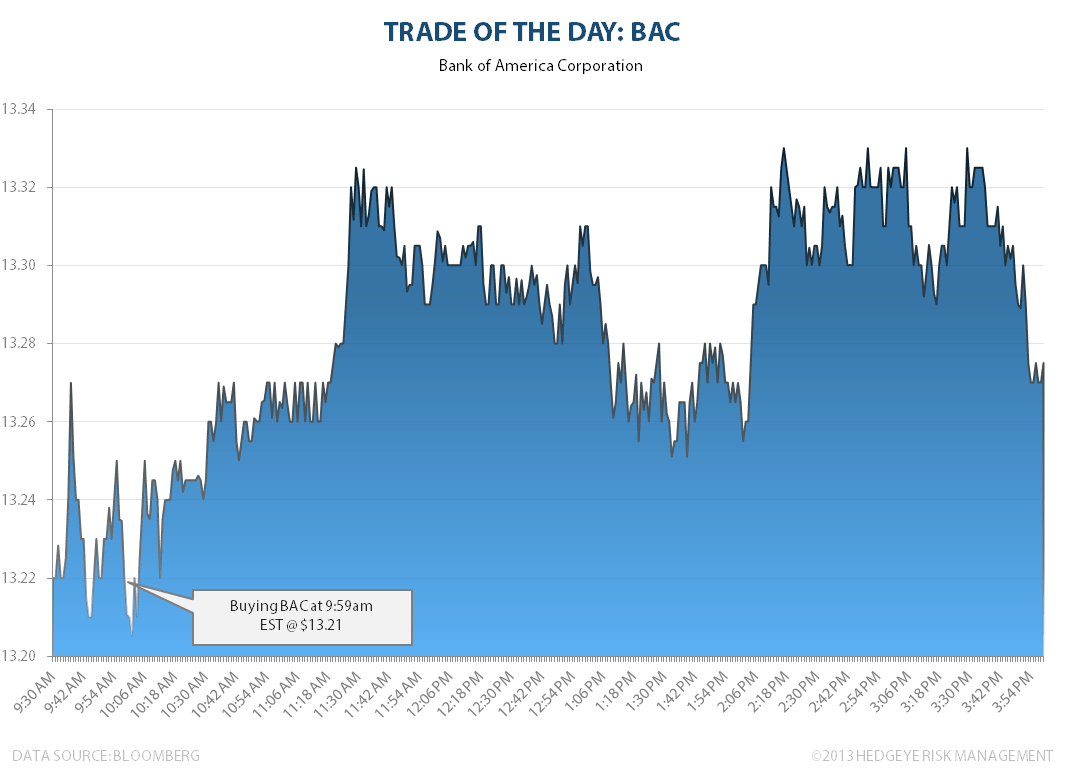

It’s tough to not buy bank stocks with the Yield Spread (10s - 2s) widening to +193 basis points wide this morning. Bank of America remains one of Hedgeye Financial Sector Head Josh Steiner's Best Ideas in 2013.

Takeaway: We bought Bank of America (BAC) at 9:59 AM at $13.21.

It’s tough to not buy bank stocks with the Yield Spread (10s - 2s) widening to +193 basis points wide this morning. Bank of America remains one of Hedgeye Financial Sector Head Josh Steiner's Best Ideas in 2013.

By joining our email marketing list you agree to receive marketing emails from Hedgeye. You may unsubscribe at any time by clicking the unsubscribe link in one of the emails.