There were some important pieces of data out of Europe this morning that we believe are in line with our European update call titled “Where Does Europe Go From Here?” that we gave last Tuesday. (Presentation: CLICK HERE ; Podcast: CLICK HERE)

Below we’ll reiterate our presentation’s main points and reference them to today’s data:

1.) Do not discount the ECB’s intervention commitment to stoke markets and preserve the common currency.

- Draghi spoke in Jerusalem earlier this morning and reiterated his “whatever it takes” pledge to keep the euro and said the ECB has an “open mind” on non-standard monetary policy if circumstances warrant.

- >> Our outlook on the EUR/USD has not changed: the cross is being supported by Draghi’s bullish comments that the ECB will leverage its balance sheet should it need to. We think the Bank is in a wait-and-watch mode as it forecasts a “gradual recovery” in growth in the back half of the year. We expect Draghi’s rhetorics and the commitment of the Eurocrats to maintain the Eurozone’s existing fabric to push the cross higher, however capped in the near term under $1.40 given our StrongDollar call and the weak underlying fundamentals. (see slide 39 in the presentation for more).

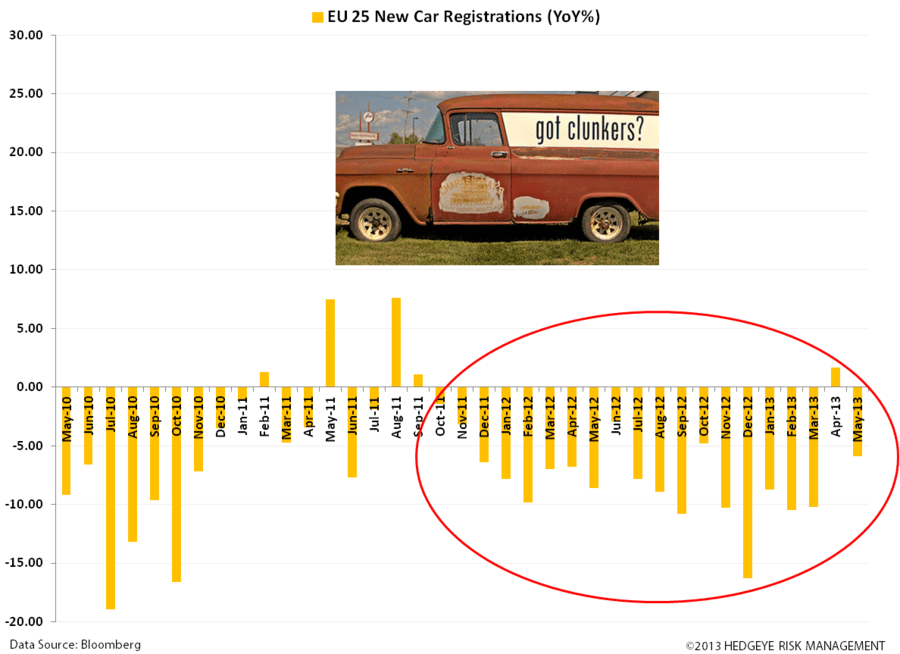

2). Fundamentals remain sluggish across the region and we expect long-term below-mean growth.

- The EU-27 New Car Registrations data came out for MAY at -5.9% Y/Y.

- >> Despite optimism last month over the +1.7% APR reading, registrations have been down for 18 straight months. We do not expect this trend to materially inflect into the summer, as we expect structural headwinds across the region to have a long tail. (see slide 8 for more).

Here are the figures broken down by manufacturer, with change Y/Y, according to the European Automobile Manufacturers' Association (ACEA):

Volkswagen (VOW.GR) 264,768 (2.8%)

PSA (UG.FP) 132,670 (13.2%)

GM (GM) 99,183 (11.3%)

Renault (RNO.FP) 94,535 (10.0%)

Fiat (F.IM) 80,930 (10.8%)

Daimler (DAI.GR) 58,360 +0.7%

Toyota (TM) 41,413 (4.9%)

BMW (BMW.GR) 65,392 (7.2%)

Nissan (NSANY) 33,747 +5.8%

Honda (HMC) 10,401 (3.5%)

Ford (F) 82,953 (0.3%)

3.) Europe will remain bifurcated, with clear winners and losers.

- According to the ZEW Survey, German Economic Sentiment (6-month forward looking) improved to 38.5 in JUN vs 36.4 in MAY.

- >> We expect relative outperformance from Germany vs its peers, especially as its exports benefit from a weak euro . (see slide 42 for more).

4.) Long the UK on the Rebound

- CPI rose to +2.7% in MAY Y/Y vs +2.4% in APR and wages growth improved from +0.6% to +1.3%.

- >> Our call remains that the UK will have headwinds, including sticky stagflation, but on balance we’re seeing an improved outlook, including from wage growth catching up to rate of inflation. (see slide 59 for more).

Matthew Hedrick

Senior Analyst