Investing Ideas Updates:

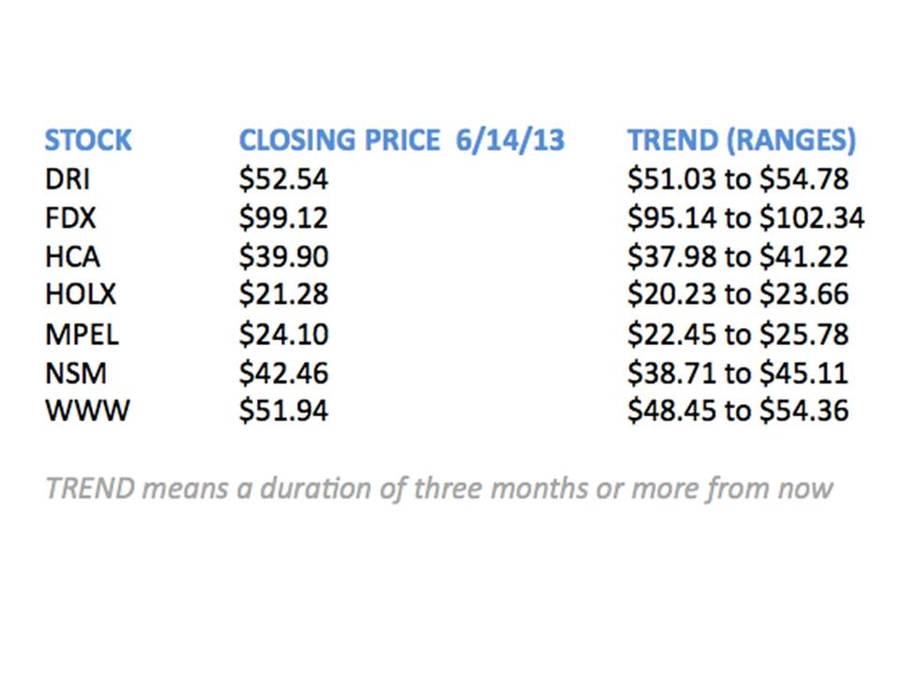

- DRI: Restaurants sector head Howard Penney does not have an update this week on Darden. (Please click here to see the latest Stock Report on DRI.)

- FDX: FedEx reports earnings next Wednesday, June 19. Industrials sector head Jay Van Sciver looks forward to this as the first major data point for our thesis.” Van Sciver thinks the headline number will be dragged down by buyout and depreciation charges – which don’t measure ongoing operations. But his focus is elsewhere. Calling FDX a “show me stock,” Van Sciver needs three things to emerge in next week’s report: meaningful sequential margin improvement at FedEx Express; a new fleet replacement schedule that should demonstrate Express’ plan to manage accelerated retirements of old aircraft; and solid guidance for 2014. If FDX can “show me” a solid case for margin expansion, investors should rally around this opportunity. Van Sciver believes the company has a low bar, given weak Q3 results. Van Sciver says the key to FDX shares regaining their upward momentum will be sequential margin improvement “and a path to further progress in guidance.” Van Sciver expects FDX to “show us” next week. (Please click here to see the latest Stock Report on FDX.)

- HCA: Health Care sector head Tom Tobin identifies a number of key drivers in both the near- and longer-term that should boost the hospital industry in general, with particular positive impact for HCA Holdings. Demographic and employment trends should provide a major boost to medical utilization overall (doctor visits, hospital stays, medical treatments, prescriptions and procedures). Tobin says the Great Recession ending leaves a reservoir of pent-up demand as people re-enter the workforce and obtain insurance coverage, and as women enter the workforce and start families – Tobin has identified a correlation between women’s employment and increased birth rates. Tobin expects a meaningful boost to HCA’s profitability from the Affordable Care Act. Finally, consolidation across the hospital industry should create cost savings from increased purchasing power and the ability to influence vendor pricing. (Please click here to see the latest Stock Report on HCA.)

- HOLX: Health Care sector head Tom Tobin says use of Hololgic’s ThinPrep® pap test technology will slow under new guidelines from the USPSTF (US Preventive Services Task Force – a panel of primary care and preventive care experts who serve voluntarily and review clinical services for effectiveness, in order to come up with guidelines for preventive care practices.) At the same time Tobin sees accelerated use from other USPSTF guidelines for increased HPV testing. The net effect, says Tobin, should be flat growth in HOLX’s core diagnostics business over the next few years. Citing earlier work indicating HPV is under-tested, Tobin’s model arrives at revenues numbers that could exceed analysts’ consensus projections for 2014 by much as $100 million. Tobin sees double upside for HOLX if revenue numbers start to come in closer to his estimates. First, more revenues is always better. But above-anticipated growth could also boost the multiple by several points as HOLX comes to be seen as more of a growth story. As fears over HOLX’s numbers decline, Tobin says the stock could become “a 20% grower with much greater stability going forward.” (Please click here to see the latest Stock Report on HOLX.)

- MPEL: Gaming, Lodging and Leisure sector head Todd Jordan does not have an update on Melco this week. (Please click here to see the latest Stock Report on MPEL.)

- NSM: Financials sector head Josh Steiner expects residential mortgage servicer / originator Nationstar to continue to expand its business through both acquisitions and internal expansion. “Acquisition announcements have been positive catalysts for the stock,” says Steiner, and NSM has some $300 billion in acquisitions in the pipeline. Steiner says NSM has a robust infrastructure to support significant increased volume, and he believes the company’s profit margins on their servicing business should improve significantly. The one factor not under their own control is the market-driven gain on sale profit margin – the profit NSM makes when they sell off loan portfolios. Steiner believes gain on sale margins will likely come in from their current spreads, but NSM’s volume growth should more than offset margin pressures. Steiner believes the elite group of high-touch, specialty mortgage servicing firms – of which NSM is the standout – should remain in a high growth phase through 2014. (Please click here to see the latest Stock Report on NSM.)

- WWW: One of the biggest objections thrown at Retail sector head Brian McGough over his bullish call on Wolverine World Wide is that there is risk of the “boat shoe trend” rolling over. The recently acquired Sperry – maker of topsiders – is WWW’s second largest brand. McGough concedes that, with Sperry representing 18% of WWW’s sales, there is certainly risk if the “trend” turns out to be merely a “fad.” Looking at his model, McGough says “there’s about $50-$80 million at risk if the boat shoe trend rolls over today.” Meanwhile, Sperry’s non-US business “represents a $300-$400 million growth opportunity.” While investors are hesitating about buying this stock, Sperry’s weekly sales data is up about 60% in the past three weeks. “People might be concerned about the trend reversing,” says McGough, “but they’re leaving money on the table so far.” WWW remains a top Retail idea. (Please click here to see the latest Stock Report on WWW.)

Macro Theme of the Week: Nothing to Fear but Plenty of Fear

Perhaps financial markets and real economic growth are more at risk than your calm demeanor would convey.

- Bill Gross, PIMCO

After an extended bubbly-fueled Happy Hour, markets are waking up with the mother of all hangovers. If you can smell the free-trade coffee, you should hope that it will clear the headache and restore clear vision before our erstwhile Master of the Universe get into the driver’s seat and start operating the heavy machinery of the Real Economy.

Legendary investor Bill Gross – co-founder of PIMCO and manager of the biggest ($292 billion) and one of the most successful (7% average annual return over 15 years) Treasury bond funds – doesn’t beat about the bush in his June letter to investors, telling folks to get out. Just plain get out. Out of bonds, out of stocks. Out of everything that has been artificially inflated by the global game of “Bubble Thy Neighbor.” Central bank-induced bubble-mania can last only so long before all those pretty baubles burst.

In Washington, Fed chairman Bernanke clears his throat and muses that it may be time to consider letting a little air out of the balloon, causing bond yields to consider rising a tad and sowing dread across the smoky battlefield of the financial markets. Money managers are ringing the tocsin on the end of a multi-decade bull market in bonds. In sympathy to Mr. Gross, it is not simple to trim close to $300 billion in Treasurys without coming near to capsizing the markets. This should give you a sense as to how uncomfortable Mr. Bernanke must be. Quoting from the Federal Reserve’s website, “Since the beginning of the financial market turmoil in August 2007, the Federal Reserve’s balance sheet has grown in size and has changed in composition. Total assets of the Federal Reserve have increased significantly from $869 billion on August 8, 2001, to well over $2 trillion.” Try getting out of that without moving the markets. As we see, even the hint that at some future time the Fed might consider trimming some of their bloated holdings has sent a shiver of panic through the markets.

From the US to Japan, what investors need to know is, the more government’s meddle in trying to fix the economy, the more volatility it creates. No less than air turbulence buffeting an airplane, volatility in the markets scares the heck out of folks. (You should know that most aircraft accidents occur during takeoff or landing, and air turbulence in midflight is almost always a non-event as far as actual safety is concerned. Something to keep in mind while you agonize over what to do with your stock portfolio.)

Greed, and Fear, and Loathing on Wall Street

With the Official Meddlers in high gear, market volatility is on a tear. Pundits expect a protracted period of turbulence – possibly running through year end, or even into Q1 of 2014 – as the Fed pretends to decide what policy steps it will take, aided and abetted by their partners in crime at the European Central Bank (see this week’s Macro call, “What’s Next for Europe”) and the Japanese policy to out-print the US Treasury. The “Fear & Greed” index maintained by CNN Money was registering Extreme Greed just one month ago. It now reads Extreme Fear. It’s “Risk-On” worldwide.

Hedgeye CEO Keith McCullough, who reminds us that Risk is always “On,” says our sentiment analysis since the end of 2012 “has indicated you want to be long fear – everyone is looking for a crisis that didn’t come.”

Did it finally come this week?

Hedgeye remains firmly bullish on US economic growth. This is not the same as being bullish on the stock market, which is easy to overlook with the indexes at all-time highs. The Fear Factor is so overpowering in the short term that people always lose sight of the longer term. As we have observed, highs are made in the markets when Greed overpowers Fear, as note the recent all-time highs in the stock market indexes, that coincided with the CNN index’s “Extreme Greed” reading. And conversely – no surprise here – when Fear is in the ascendant, markets make lows. This week’s gapping-down openings in the S&P 500 have been seen as nothing short as a sign that Life As We Know It is coming to an end.

Do You Have a Yen for Stability?

Japan’s Nikkei stock market index is down over 20% since May 22nd, flushing out with a one-day 6.4% drop, making for a textbook-perfect market crash. Our read is that the break in the strength of the Yen precipitated this final downdraft. The subsequent recovery in the currency may give their markets a bit of a lift, but don’t let a brief rise fool you. This is not a recovery – more like a drowning man whose body floats to the surface, but whose lungs are not capable of drawing air. Pretty nasty stuff, huh?

Conclusion: Fear the Fear

As Keith mentioned the other day in response to an interviewer’s question, When big stuff starts snapping and crashing like this, we get out of the way.

Have you ever heard an investment professional recommend taking no action? “Just say No” says McCullough. Fear is a function of uncertainty – and as we have observed, uncertainty is a barrier to higher stock prices. We think the Fear in today’s markets is a direct result of the false certainty offered by central bank money-printing. John Maynard Keynes famously observed that “markets can remain irrational longer than you can stay solvent.” The corollary is that there is no such thing as Eternal Solvency.

Even the government’s ability to print money will run out once the last tree is chopped down. But well before then, Chairman Bernanke’s credibility is the only force holding the line on the value of the dollar. We no longer trust in God – just in the questionable capacity of our unelected academic geniuses.

To quote another of Keynes’ lapidary sayings, “In the long run we are all dead.” Long after chairman Bernanke – and yes, Dear Reader, you and I too – are gone from this world, there will be an Economy. And the Economy is where real things happen that affect life. Expectations about the Real Economy drive stock prices – while real events often dampen price trends, leaving the market to mark time until the next expectation arises.

Folks have long been anticipating a crisis, which has uncooperatively failed to materialize. Even with the market retreating from all-time highs, Hedgeye remains more bullish on the US economy than the Fear consensus. The dollar has backed off its strong uptrend. If it catches its breath and resumes, we’ll be strongly bullish on the economy. If it flounders a bit, we’ll be just plain bullish. But make no mistake: we remain strong on our theme of increasing Consumption pushing the US economy higher.

At worst, compared to other world economies, the US remains “the best house in a bad neighborhood.” Bernanke could follow through on the worst of the market’s fears and actually pull the plug on the Fed’s bond buying. This would rock the bond markets. We think it would have a rocky, but not lasting affect on the stock market. As far as that elusive creature the Real Economy is concerned, we think folks would respond first with abject terror, then with surprise as it dawned on them that the Fed getting out of the way is actually the sustainable path to prosperity.

It may not look like it right now, but Confidence can replace Fear as the driving force in the economy. Which begs the question – what will the markets have to look forward to then?

Sector Spotlight: A LULU of a Week in Retail

In case we haven’t made the point lately, we are bullish on the consumer here at Hedgeye. Retail sector head Brian McGough says “this week’s surprisingly high Retail Sales report for the month of May certainly supports that thesis.” Retail Sales, reported on Thursday, rose 0.6% in May – ahead of the 0.4% rise that economists had projected. The numbers were goosed by big increases in new automobile sales, and in retail purchases of home-building supplies – adding credibility to Hedgeye’s thesis around new family unit formation, as young people with jobs and confidence about the future acquire things like dogs and babies that need houses to live in and cars to transport them.

McGough says the key theme in Retail today isn’t so much about consumers spending money, but about companies. As companies build out their infrastructures, McGough sees capital spending for the coming year up in the 30% range “almost across the board.”

McGough says this is very significant, as capital expenditures generally grow in line with sales, which tends to be in the 8%-10% range year over year. Hedgeye is bullish on consumption growth for a number of reasons but, says McGough, “the cold, harsh reality is that increased consumer spending will not lead to a 30% boost in Retail Sales.” This means companies either need to see strong improvements in their profit margins to justify the steep costs, or there could be a sector-wide decline in Return on Invested Capital (ROIC). McGough believes the second scenario is more likely.

A decline in ROIC is not the end of the world if it is temporary. Like the market overall, Retail valuation multiples are at their peak, and companies have just set new peak margin levels. There’s no ironclad rule that says peak P/E multiples on peak profit margins automatically mean the next move in the stock price is down. Theoretically, current peaks could be the precursor to yet-higher peaks. But how likely is that?

“Peak margins” means the internal profitability of companies’ sales operations are at the highest levels they have ever been. “Peak multiples” means the market is according the companies the highest P/E multiples ever, an enthusiastic endorsement of the sector’s robust growth.

Using a sports analogy – Hedgeye is big on sports analogies – McGough says a key element of our process is “making sure that we’re stepping up to the plate with a 3-and-0 count,” with strong odds that we will get on base. “When companies at peak multiples, and at peak margins start spending money at an increased rate, that’s more akin to a 0-2 count.” McGough sees a whole list of companies falling into this category, including LULU (Lululemon Athletica), COH (Coach), M (Macy’s), DKS (Dick’s Sporting Goods), HBI (Hanesbrands), RL (Ralph Lauren), CRI (Carter’s), GPS (Gap Stores), and GES (Guess).

McGough highlights the uncertainty swirling around the sector in his stand-out comment on the abrupt departure of LULU’s. McGough says LULU had only one thing to do, which was restore some investor confidence. They blew it.

On the plus side, departing LULU CEO Christine Day has taken the stock price from $3 to $80. On the minus side, the company recently suffered issues that cut severely into their credibility, such as having to trash an entire season’s worth of faulty athletic pants, and the eruption of profit margin problems. With problems in need of a fix, McGough says the investment community was stunned by the CEO’s departure, which he calls “the corporate equivalent of being bitten by your Golden Retriever.”

McGough likes companies where the investment community can be confident that management is taking returns higher, doing more with less. They include our Investing Ideas highlight stock WWW, and such names as Nike (NKE) and Footlocker (FL). When companies can grow operating profit faster than they are adding incremental capital to their business, it is usually a recipe for outsized multiple expansion over a prolonged time period.

The advice to Retail sector investors is the same as to any shopper: inspect the merchandise for defects before you put down your money. The stock market doesn’t give a store credit.

Investing Term of the Week: Volatility

“Volatile.” A substance that breaks down easily. A “volatile compound” evaporates readily at room temperature.

“Volatile.” A person who loses their temper easily.

“Volatile.” Stocks or other investment instruments whose prices move around erratically, generally giving rise to Uncertainty, if not Fear (see above).

At its basic level, financial Volatility is expressed in terms of the Standard Deviation of price moments around an average return over a period of time. (This is all the math you are going to get. If you are quantitatively savvy enough to want more than that, you don’t need us to explain this.)

There is Historical Volatility, a straightforward calculation based on the standard deviation of price movements of a security over a discreet time period.

There is Implied Volatility, a key part of the complex calculation that goes into options pricing models. Traders and quantitative analysts (“quants,” in the trade) use Implied Volatility instead of Price when determining which option contract to trade. Price is a function of a buyer and seller at a given moment, making it a subjective measure, not a statistical metric. Implied Volatility is a prediction of how an option will react to movements of the underlying stock.

If you want to get fancy, quants also use options pricing models for individual stocks, because stock price moves have what they call “implied optionality.” That’s an Ivy League way of saying you can predict the future price of a stock better by using an options pricing formula than by charting past price and volume moves.

The best known volatility instrument in the market today is the Volatility Index maintained by the CBOE (Chicago Board Options Exchange). Called the VIX, this index is calculated from a weighted average of volatility measures of a range of options on the S&P 500. To many investors, the VIX personifies the “Fear Trade.” VIX up = More Fear. VIX down = Less Fear.

Another way of expressing this – one often heard in the financial media – is “Risk On / Risk Off.” Says Hedgeye CEO Keith McCullough, “Risk is always on. Who are you trying to kid?”

Pin the Smile on the Trader

Just for fun, we leave you with what has to be the cutest financial risk metric of all. It’s called the Volatility Smile, named for the shape on the graph when volatility measures of options are lowest near the price where the underlying stock is trading (“at-the-money options”), with volatility increasing moving away from the current price in both directions (“in-the-money options and out-of-the-money options.”) Academics think the Smile reflects risk aversion in market participants, noting that equity options in the US markets started showing a Volatility Smile in the aftermath of the Crash of 1987. But they’re not sure.

The ultimate authority on most things in the cosmos – Wikipedia (from whom we also borrowed the chart) – says the Volatility Smile “is not fully understood, and modeling the volatility smile is an active area of research in quantitative finance.” This may make you feel better – Hey, the guys in the Ivory Tower don’t understand this stuff either! Or it may make you feel worse – You mean, the guys in the Ivory Tower don’t understand this stuff either?!

For those who prefer Certainty, there’s always Death and Taxes.