This note was originally published at 8am on May 31, 2013 for Hedgeye subscribers.

“I raise my flags, don my clothes

It's a revolution, I suppose.”

-Imagine Dragons

For the last five plus years, Hedgeye has delivered an Early Look to your inbox every market morning. Primarily, it has been Keith delivering the goods with the rest of the team chipping in from time to time. With over 1,000 Early Looks written, you would think it takes some sort of Macro Imagination to get these notes out the door every morning.

Fortunately for us the world provides a great amount of economic fodder and this morning is no exception, but to be fair some amount of creativity is required to keep these notes at least somewhat interesting. Moreover our research team, like your teams, requires creativity to generate interesting investment ideas. But, what exactly is the root of creativity?

A study by Jordan Peterson of the University of Toronto found that the, “decreased latent inhibition of environment stimuli appears to correlate with greater creativity among people with high IQ.” In layman’s terms, the research says that people whose brains are more open to stimuli from the outside environment will likely be more creative.

Conversely, the risk of too much outside stimuli is mental illness due to overload. In this regard, the differentiator between creativity and madness is a good working memory and a high IQ. In essence, with these attributes a person has the capacity to “think about many things at once, discriminate among ideas and find patterns”. Without them, one can’t handle the increased stimuli.

So even if we know the root of creativity and innovation, how do we accelerate it within our companies and ourselves? Interestingly social networks may be giving us a huge leg up in this regard. According to Martin Ruef from Stanford Business School:

“Entrepreneurs who spend more time with a diverse network of strong and weak ties...are three times more likely to innovate than entrepreneurs stuck within a uniform network."

In a nutshell, creative people are more open to outside stimuli and best leverage that creativity when exposed to broad network of loose ties. (And just think, my ex-girlfriend used to tell me I spent too much time on Facebook!)

Back to the global macro grind . . .

As I noted earlier, this morning is certainly providing a fair amount of economic fodder. A few points to call out:

- The Shanghai composite sold off hard into the close on chatter that tomorrow’s manufacturing PMI will come in below 50. This is consistent with the flash PMI reading from Hong Kong and also the pattern of economic data being leaked early (we removed long Chinese equities from our Best Ideas list earlier this year);

- Japanese equities outperformed over night, but finished down -5.7% on the week. The more interesting data point from Japan was April CPI which came in at -0.4% and clearly signals that the Bank of Japan has more to do before sustainable inflation is generated (Short Yen remains on our Best Ideas list); and

- Japanese government pension fund with $1.1 trillion in assets indicated it would consider increasing its allocation to equities. To buy one asset class, another asset class must be sold. If the action in the Japanese government bond market is telling us anything it is that this allocation is already occurring as yields on 10-year JGBs have been spiking recently.

Domestically, our thesis of economic growth going from stabilization to acceleration continues to be validated. Market internals clearly support this as the SP500 is up more than 16% this year and the treasury market is literally at 12-month lows. If you didn’t know, now you know . . . economic growth is good for equities and bad for bonds.

As we dig deeper in the market internals, the performance of the sub-sectors of the SP500 validate this view even more. As of last night, the top two performing sectors in the year-to-date are healthcare up 23.3% and financials up 23.0% and the two worst performing sectors are utilities up 8.6% and materials up 9.1%. There we have it again, the growth sectors are dramatically outperforming.

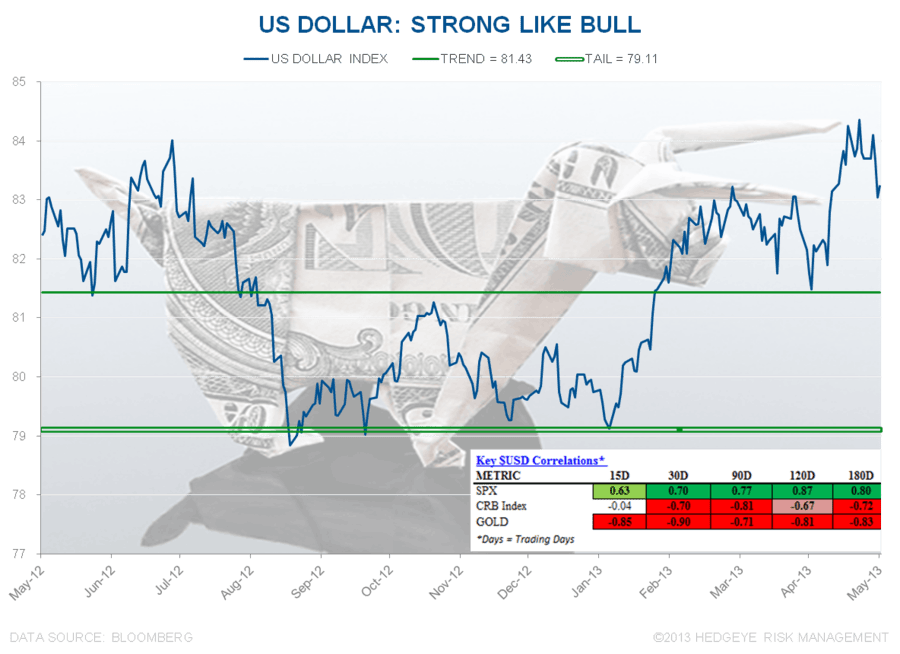

Now if you are a thoughtful stock market operator, you probably want to call me out on something from the last sentence, which is that materials should do well in an environment in which growth is accelerating. This is true except for the one important factor: the U.S. dollar. In the Chart of the Day, we highlight the impact of the dollar and the associated correlations over the last 180 days, which are +0.80 with the SP500, -0.72 with the CRB index, and -0.83 for gold. A strong dollar equals weak commodities.

This Macro theme of up dollar and down commodities is very positive for a number of sectors. This year our Restaurant team of Howard Penney and Rory Green has done an outstanding job leveraging the macro call with their stock specific work. One of their best ideas in my view has been a sell call on McDonald’s on April 25th and since then the stock has underperformed the market by some 800 basis points.

At the time more than 30 firms had recommendations on MCD and no one had a sell. This is creative and contrarian research at its finest. Needless to say, our restaurant team eats alpha for breakfast, lunch and most value meals! Ping us at sales@hedgeye.com if you want access to trial our restaurant research.

Our immediate-term Risk Ranges for Gold, Oil (Brent), US Dollar, USD/YEN, UST10yr Yield, VIX, and the SP500 are $1354-1423, $101.03-103.89, $83.10-83.98, 100.31-103.71, 2.03-2.19%, 12.28-15.31, and 1641-1674, respectively.

Keep your head up and stick on the ice,

Daryl G. Jones

Chief Creative Officer