This note was originally published at 8am on May 28, 2013 for Hedgeye subscribers.

“A coach is someone who can give correction without causing resentment.”

-John Wooden

On weekends, I coach 4-6 year olds (hockey). During the week, I sometimes coach adults (macro). All the while, Mr. Market is always coaching me through something. I bear no resentment towards him. To the contrary, I quite enjoy it when he tells me what to do (signals).

With US stocks down for 4 of the last 5 days, there was another choice to be made on Friday – correction or crash? This wasn’t unlike many of the learning opportunities that Mr. Market has provided us in the last 6 months. Buying the correction has been the right choice.

The only thing that seems to be crashing this year is the idea that we are going to crash. The #EOW (end of the world) trade has been the worst place you could be long for the month of May. When you have #GrowthAccelerating, you don’t buy Yens, Gold, and Treasuries. Ask the Coach.

Back to the Global Macro Grind…

After covering all but 4 short positions on red Friday morning, I posted a note titled “Oversold: SP500 Levels, Refreshed.” I also re-shorted the Yen at our immediate-term TRADE overbought line of 101.22.

These aren’t victory laps; they are timestamps – and I am 100% accountable to them. Two of the four short positions we have left are related to Japanese Policies to Inflate (short Yens and JGBs). The other two are short Russia (world’s 3rd worst stock market YTD, next to Peru and Cyprus) and short Emerging Markets (EEM) which do not like #StrongDollar (and are down YTD).

What if I didn’t listen to the Macro Coach? What if I just ignored my signals and went with “feel”? Been there, done that – many times over, in many arenas and markets – and, in general, it doesn’t work. For us what works is the combination of A) Risk Signals and B) Research Views – when we have both, we move.

Last week’s US Equity market risk wasn’t the economic fundamentals – it was Ben Bernanke. He tried his best to confuse economic gravity (#GrowthAccelerating) with his longstanding and dogmatic view that he needs a weaker US Dollar to achieve his goals. #wrong

He got that last week – the Dollar weakened and so did the US stock market in kind (they now have a very positive correlation, Ben). Bernanke’s jawboning arrested #StrongDollar momentarily (-0.65% on the week), and the SP500 corrected -1.2% from its all-time weekly closing high.

Back to the Research View - whether Bernanke wants to acknowledge it or not, last week’s US economic data was decisively bullish:

- New Home Sales for April ripped +8.8% sequentially (month-over-month) to 454,000

- US weekly Jobless Claims surprised on the downside (again) at 340,000 (-8.9% year-over-year)

- US Durable Goods #GrowthAccelerated +3.3% in April (versus March)

That’s why US Treasury Yields continued to back up (despite Bernanke trying to talk them down). The US 10yr Yield is up again this morning to 2.04% and has no intermediate-term TREND resistance to 2.41%. So Mr. Market is trying to coach @FederalReserve through this…

Whether Bernanke tells his boys to listen to the market’s message will be his legacy. His boss (President Obama) cares about his political legacy too. On the cover of The Economist this weekend is a picture of Barry looking a little confused alongside the titled “How To Save His Second Term.”

Coach says the best way to make Obama look good is via our #StrongDollar, Strong America strategy. It worked for Reagan and Clinton – and it can work for Obama too. If he doesn’t get it, Hillary will – this isn’t that complicated, folks.

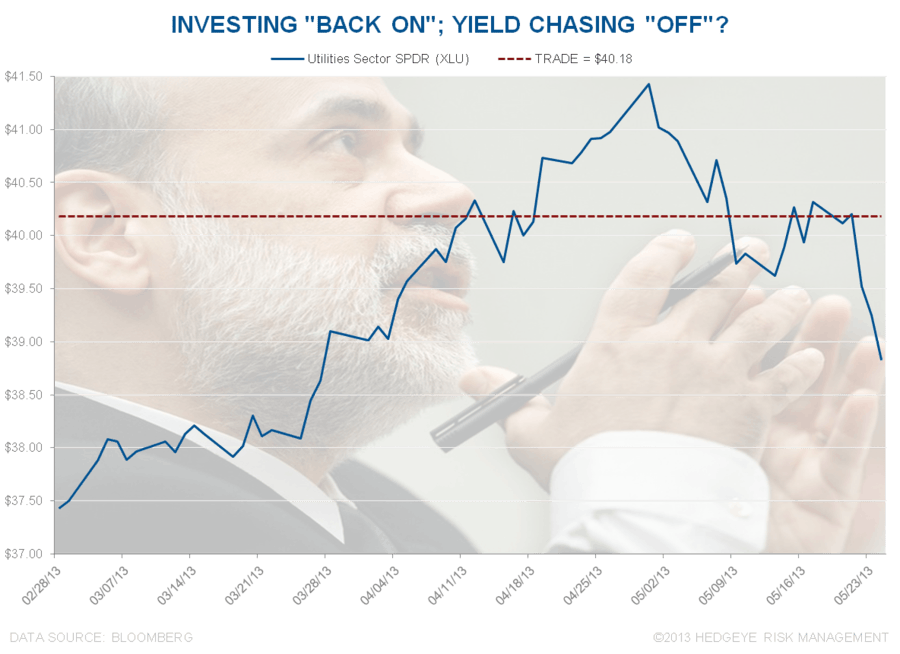

Coaching you through corrections in Yens, Gold, and Treasuries starts with reminding you that these aren’t corrections – in 2 of 3, they are crashes – and for many Americans still choking on Bernanke Yield Chasing trade, the third may very well become his Waterloo.

Just to show you how horrendous being long no-growth “yield” is performing in the last month, here’s the score:

- Utilities (XLU) are already down -6.3% for the month of May alone!

- With Treasuries down (Treasury Yields up +38bps in the last month!), Financials (XLF) lead the SP500 at +5.5% for May to-date

- Low Yield Stocks (i.e. Growth Stocks) are up +6.7% in the last month and now +20.1% for 2013 YTD

Got that Messrs Bernanke and Obama?”

With the US Dollar +5.1% YTD and Commodities -3.7% YTD, Coach says get the US Dollar right and you’ll start to get America right. Freedom, Liberty, and Growth are the best paths to prosperity – not Dollar Debauchery, fear-mongering, and sketch balls at the IRS.

We can get you guys through this. Yes We Can. Embrace #StrongDollar, and be the change.

Our immediate-term Risk Ranges for Gold, Oil (Brent), US Dollar, USD/YEN, UST 10yr Yield, VIX, and the SP500 are now $1341-1421, $101.48-103.94, $83.62-84.29, 101.21-103.66, 1.96-2.06%, 12.27-14.46, and 1642-1672, respectively.

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer