TODAY’S S&P 500 SET-UP – June 10, 2013

As we look at today's setup for the S&P 500, the range is 45 points or 1.18% downside to 1624 and 1.56% upside to 1669.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.87 from 1.87

- VIX closed at 15.14 1 day percent change of -8.96%

MACRO DATA POINTS (Bloomberg Estimates):

- 9:50am: Fed’s Bullard speaks in Montreal

- 11:00am: Fed to purchase $1b-$1.5b notes in 2017-2043 sector

- 11:30am: U.S. to sell $30b 3M bills, $25b 6M bills

- U.S. Rates Weekly Agenda

GOVERNMENT:

- President Obama speaks on Equal Pay Act’s 50th anniv.

- Jeff Chiesa, R-N.J., is sworn in as U.S. Senator

- House, Senate in session

- Senate Commerce Cmte votes on nominations of Penny Pritzker for Commerce Sec., Anthony Foxx for Transportation Sec.

- Senate to vote on Leahy amendment to farm bill, S. 954, followed by final passage, 5:30pm

- Fed issues interim rule on how to treat American branches of foreign banks for a section of Dodd-Frank that prevents bailouts of swaps dealers

WHAT TO WATCH

- Google said to be buying Waze for $1.1b for social maps

- Apple holds Worldwide Developers Conf.; to unveil new iOS

- Elan board rejects raised $6.7b Royalty Pharma offer

- AstraZeneca to buy Pearl Therapeutics for up to $1.15b

- SoftBank’s clearance for Sprint deal confirmed by officials

- China May industrial output rose 9.2% vs est. 9.4%

- Marchionne says Fiat may acquire Chrysler stake before IPO

- JBS said to agree to buy Seara food assets from Marfrig

- Exide files for Chapter 11 bankruptcy after losing Wal-Mart

- McDonald’s May global comp. sales seen gaining 1.9%

- GE CFO Sherin said to take over finance arm as soon as summer

- CBS said nearing $2.7b in upfront advertising commitments

- Hawke horror film “The Purge” outsells Vaughn/Wilson duo

- Japan revises growth to annual 4.1% in boost for Abe

- Obama tells Xi that China must act against cybertheft

- Pentagon’s cybersecurity plan calls for $23b through 2018

- U.S. Weekly Agendas: Finance, Industrials, Energy, Health, Consumer, Tech, Media/Ent, Real Estate, Transports

- North American M&A Agenda

- Canada Weekly Agendas: Energy, Mining

- Retail sales probably rose in May: U.S. Weekly Eco Preview

- U.S. Retail Sales, BOJ, Iran, U.S. Open: Wk Ahead June 10-15

EARNINGS:

- Navistar International (NAV) 4pm, $(1.20)

- Lululemon Athletica (LULU) 4pm, $0.30

- Diamond Foods (DMND) 4:01pm, (-$0.19)

- Annie’s (BNNY) 4:06pm, $0.28

- Pep Boys (PBY) 4:41pm, $0.09

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- WTI Trades Near Two-Week High on Economy; Sudan Oil Threatened

- Gold Bull Bets Reach Seven-Week High Before Retreat: Commodities

- China Approves Gold-Backed ETPs as Domestic Buyers Chase Bullion

- Gold Declines to Two-Week Low in London on U.S. Stimulus Outlook

- Corn Drops With Soybeans as Dry Weather May Aid Crop Conditions

- Freeport May Declare Force Majeure If Grasberg Shutdown Extends

- JBS Becomes Largest Chicken Producer With Marfrig Deal

- Rupee Slump Set to Boost Costs for India Bullion Importers

- Palm Oil Falls From Two-Month High on Concern India May Buy Less

- Allana in Ethiopia Snubs Potash Supply Concern: Corporate Canada

- Sudan Threatens to Shut South Sudan Oil Over Rebel Support

- San Onofre Seen as Latest Setback for U.S. Nuclear Power: Energy

- Bullion Bear Market Seen Extending to $1,303: Technical Analysis

- Deutsche Bank Starts Singapore Gold Vault With 200 Ton Capacity

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

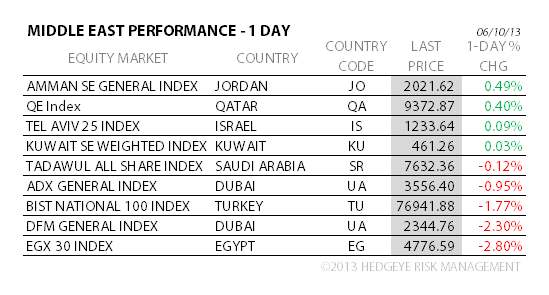

MIDDLE EAST

The Hedgeye Macro Team