“Books can lie, but places never do.”

-Jack Weatherford

I love that quote. Jack Weatherford uses it in the Introduction to this epic book I am still reading – Genghis Kahn and The Making of The Modern World. Politicians and market pundits can lie too, but markets are always scoring the truth.

Some will disagree and say that markets are often wrong. Agreed – if the market goes your way on the timeline that you outlined prior to taking your position, that is. Being positioned for what the market currently accepts as truth is the name of the game.

If you could be right every day, you would be. Very few will disagree with me on that.

Back to the Global Macro Grind…

Last week’s employment data continued to drive home a very simple, but trending, score in 2013 – US employment and consumption growth is accelerating. This shouldn’t have been a surprise by the time you saw the sequential improvement in the payroll data on Friday. Our preferred leading indicator (non-seasonally adjusted rolling jobless claims) has been trending bullish for 6 months.

Every 3 months, we update our Top 3 Global Macro Themes @Hedgeye. This quarter I was definitely nervous about one of them. Making a call that US growth could go from stabilizing to accelerating was more of a question to us than it was a definitive answer. Throughout Q213 however, US employment, housing, and consumption data has improved, impressively.

To review - our Macro Themes for Q2 2013 are:

1. US #GrowthAccelerating

2. #StrongDollar

3. #EmergingOutflows

Since the fulcrum factor in our trending themes remains the US Dollar, last week’s abrupt selloff in the US Dollar versus the Japanese Yen definitely mattered. An immediate-term TRADE does not an intermediate-term TREND make though, so this morning’s -1.25% reversal in that move to #StrongDollar’s benefit has me smiling again.

Alongside a big bounce in #StrongDollar versus Burning Yen, this is what you get pre-open:

- Gold and Silver down another -0.5-1.3%, respectively

- Copper and Corn down another -1.1-1.3% respectively

- US Equity Futures up another 6 handles, following Friday’s +1.3% bullish breakout back above 1624 SPX

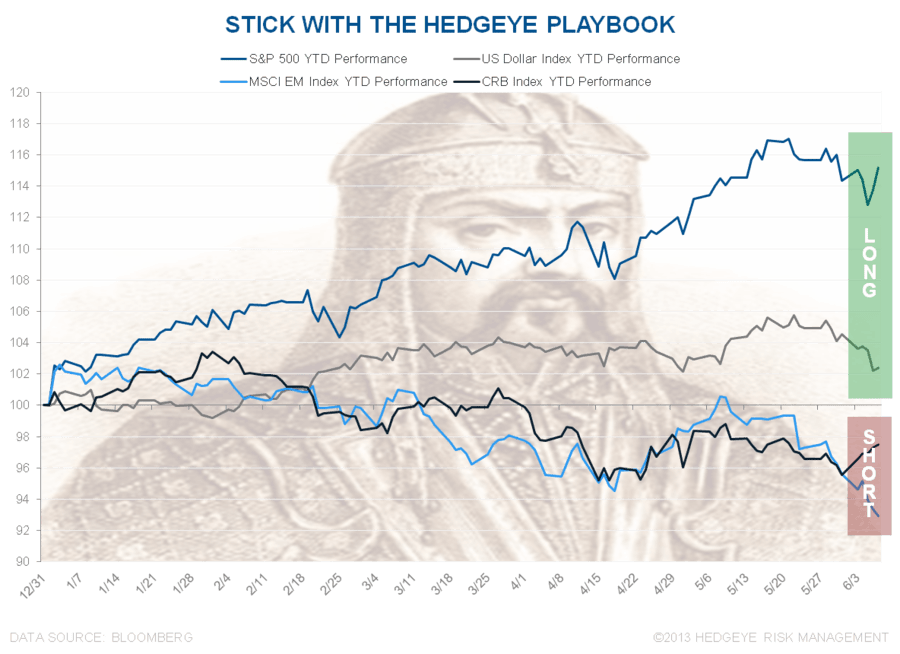

If you are betting on growth, you’ve recognized that the market’s version of the truth is currently paying people who have embraced the non-consensus bullish case that #StrongDollar is a pro-growth signal. You can see that in the following trending correlations:

- USD vs SP500 (on our intermediate-term TREND duration) has a positive correlation of +0.81

- USD vs Gold (on our intermediate-term TREND duration) has a negative correlation of -0.72

Moreover, if you want to dig into the multi-factor, multi-duration update, these correlations have actually strengthened across multiple factors in the last month. In addition to rising US Treasury yields, here are some more pro-growth signals to consider:

- US Financial Stocks (XLF) are +4.2% in the last month vs slow growth Utility Stocks (XLU) at -4.5%

- Low Dividend Yield stocks (i.e. higher growth stocks) = +20.9% YTD

- High Short Interest stocks (i.e. the ones that squeeze hedgies shorting them on “valuation”) = +19.1% YTD

Again, the score in the book may very well feel like a lie to people who are still bearish on growth, but where this market has scored the game for 2013 YTD isn’t. I’m not a fan of investing alongside what people are “feeling” anyway.

Another score that is developing quickly here is that a #StrongDollar eventually drives underperformance in Emerging Markets. We call this Theme #EmergingOutflows and it’s worth scoring this morning as well:

- MSCI Emerging Markets Index = down another -2.4% last week and -6.6% for 2013 YTD

- China’s Shanghai Composite Index = down another -3.9% last week and -2% for 2013 YTD

- Brazil’s Bovespa Index = down another -3.6% last week and -15% YTD

Investors we speak with on #EmergingOutflows fall into 1 of 3 camps:

- Bearish on everything (we aren’t) – so they think Copper and China going down is bearish for US stocks

- Bullish on Global Growth (we aren’t) – so they think they should buy Emerging Markets because they “look cheap”

- Bullish on US #GrowthAccelerating and #StrongDollar – so they are bearish on Emerging Markets tied to commodities

We’re obviously in the 3rd camp. Looking at this week’s contra-indicator camps (weekly futures and options contracts in the CFTC data) we’re still seeing Camp 1 A) buy Gold (weekly net long position +19% wk-over-wk) and B) short SPY (there’s still a net short position in SPY right now of -3,061 non-commercial contracts).

I’m not saying we’re going to nail the macro call in perpetuity. All I’m saying is that last week was one of the top 6 times in the last 6 months that you’ve had to re-load on the long side where it’s actually working. Bullish Places are as bullish does. And, globally, they are getting harder and harder to find.

Our immediate-term Risk Ranges for Gold, Oil (Brent), US Dollar, USD/YEN, UST10yr Yield, VIX, and the SP500 are now $1, $100.27-105.25, $81.31-82.96, 96.05-99.98, 2.07-2.22%, 13.77-15.87, and 1, respectively.

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer