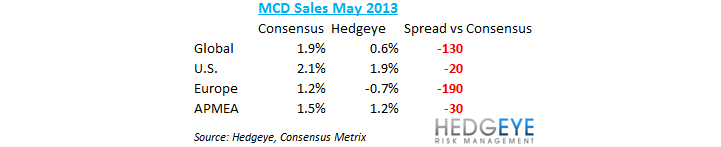

McDonalds is set to release its May sales results before the market open on Monday. We expect sales to disappoint versus consensus expectations as the difficult competitive environment in the U.S., as well as economic malaise in Europe, continues to impact results.

We’ve been the lone bears on Wall Street when it comes to MCD since turning negative on the name on 4/25. For May, much of the downside in global same-restaurant sales growth expectations comes from Europe. See our recent work on this here. For 2013, we still believe MCD is not going to hit the numbers that Wall Street is expecting.

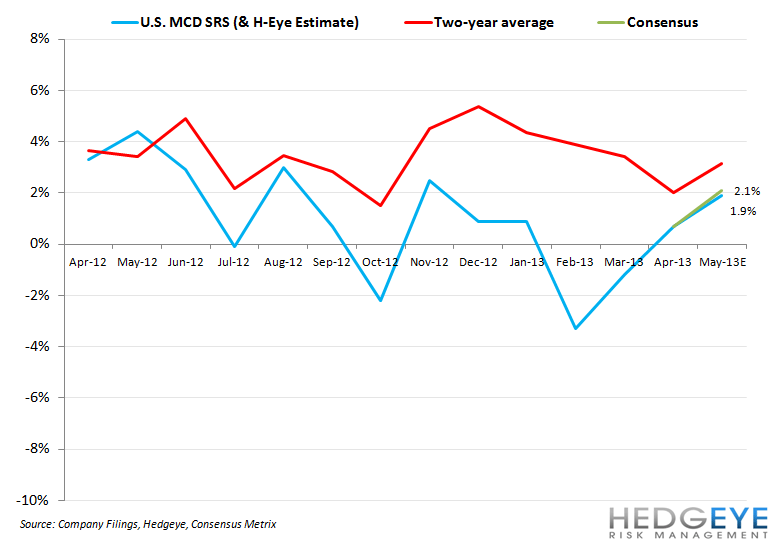

Below, we provide charts with our estimates for each region of the world versus consensus expectations. We will follow up Monday’s release with our thoughts on the data and our updated view of the stock. The long-term trend in MCD’s sales trends needs to reverse. As things currently stand, we believe the data suggests a strategic failure on the part of the company as well as a disconnect between investors’ expectations and the reality of the company’s fundamentals. As this continues, we are looking for more underperformance versus peer consumer and S&P 500 benchmarks.

Howard Penney

Managing Director

Rory Green

Senior Analyst