Our CEO Keith McCullough likes to frame sentiment as being bullish, bearish, or not enough of one or the other. The investment community is not bullish enough on Starbucks. The bear case does not scare us when it comes to Starbucks. We decided to run through some bull and bear points to refresh clients on our thesis.

Summary

We remain bullish on Starbucks at current levels. Despite the stock trading at the high end of its historical consensus forward earnings and cash flow multiples, we believe more upside is in store. Bullish factors we are focused on include rapid unit growth in China, expansion into new segments of the global food and beverage industry, and a commodity tailwind that only seems to be getting stronger.

Below, we go through the bear and bull cases for SBUX and offer our thoughts on each sub-point.

Performance

Starbucks has been a favorite name of ours for virtually all of the last four years. Aside from a period in 3Q12, when our research process suggested a more cautious stance was necessary, we have been bullish on the stock as it has taken share from competitors in existing businesses and grown its touch points in tangent areas of the food and beverage industries. Despite strong outperformance and plenty of bearish arguments to the contrary, we are reiterating our bullish stance today as we believe that the investment community is bullish, but not bullish enough, at this price.

As the quantitative levels, below, indicate, SBUX is in bullish formation with the immediate-term risk range at $62.63-$64.56 and TREND level support at $59.57.

Bear Case: Valuation, Sentiment, Portfolio Pitfall, Personnel Changes, EMEA, Brewer Growing Pains

Valuation

Valuation is a factor we consider when formulating all investment theses but is not, in itself, a thesis. It’s impossible to know if Starbucks’ stock is cheap or expensive at current levels unless one knows the forward earnings of the company. What would make the stock cheap to us is if the future growth potential of the company was being overestimated by the investment community. We do not believe that it is.

Sentiment

The investment community has become more bullish on Starbucks over the past year as the stock price has risen and visibility on the company’s future growth strategies has increased. Casual dining has seen sentiment rise more than quick service as investors have sought exposure to more discretionary niches of the consumer space. We believe that the stock has further to run over the intermediate TREND and long-term TAIL durations. Our CEO Keith McCullough likes to frame sentiment as being bullish, bearish, or not enough of one or the other. The investment community is not bullish enough on Starbucks.

Portfolio Pitfalls & Growing Pains

The history of the restaurant industry is littered with anecdotes of management teams that thought they could grow forever at an ever-increasing rate. Executive compensation structures more closely tied to unit growth targets than returns typified the folly of so many quick service and casual dining companies. Many companies have reaped the negative rewards of growing too fast and/or adding too many concepts to the company’s structure.

With respect to growth, Starbucks has not been perfect throughout its history. Between 2005 and 2009, Starbucks almost doubled its number of locations, to almost 17,000. In 2007, Howard Schultz flagged changes in the consumer experience to then-CEO Jim Donald as counter-productive initiatives. Examples included “flavor-locked packaging” and complicated espresso machines that eroded the degree to which visiting Starbucks resonated with consumers.

Perhaps the most acute risk we see in Starbucks’ future trajectory is the growing number of ventures under the auspices of the current management team. We expressed this on 6/5/12 in a note titled “ONE MOVE TOO MANY?”, writing that the company seemed to be embarking on an investment phase implied added risk to the share price. Managing five concepts, we wrote, seemed to be a departure from the returns-focused strategy had added value to the company in recent years.

The best argument against the idea that Starbucks will begin to destroy value by overstretching its shareholders’ capital is the current management team’s leadership. Schultz’ emphasis on discipline and rigor in his team’s approach to making capital allocation decisions differs greatly from other, less effective, executives in the industry.

Executive Changes

As Starbucks becomes larger, and a greater number of individuals assume leadership positions, the potential for executives to leave to pursue alternative paths could increase. Michelle Gass leaving the company for Kohl’s Corp. is a blow, with CEO Howard Schultz having praised her impact on several key areas of the business including a key role in the turnaround of 2008/2009.

What Gass’ departure means for the stock is difficult to know. The pessimist may infer that her departure represents, in part, a lack of confidence in Starbucks’ future trajectory as she had, just one month ago, been called back from her role leading the EMEA division to work in an undefined leadership role under Schultz focusing on making the “pieces” of Starbucks work together, according to The Wall Street Journal. Gass worked for Stabucks for 16 years and, in time, may have been a candidate to assume a leadership role in the company’s C-Suite.

We believe that Gass’ departure from the company is a negative but, given her focus on the EMEA division over the past couple of years, it is clear that the company has many other talented individuals that have helped drive important areas of the enterprise forward. If we were to speculate, we would guess that the incentive of almost $10 million over the next four years likely had more of an impact than unease in her role at Starbucks.

EMEA

The weakness of Europe’s economies poses a risk to all global companies but we believe that Starbucks is relatively well-prepared to weather the storm. The company derives a very small proportion of its earnings, or less than 2% of total consolidated operating income, from EMEA which offers shareholders peace of mind as Europe continues to struggle to find economic momentum. Even with such a low degree of exposure, the company is taking a proactive approach to mitigating the risk of further economic turbulence in EMEA by increasing the proportion of licensed to company-owned stores.

Bull Case: Strong Dollar, Growth Runway, Commodity Costs, Mgmt Team, ROIIC

Strong Dollar, Strong America, Strong Consumption

In November 2012, our Macro team turned positive on U.S. growth, which is 71% consumption, as the strengthening U.S. Dollar gave consumers a food and energy price cut. With the U.S. economy continuing to improve, we believe that Starbucks is one of the best ways to play a strengthening consumer. Jobless Claims, in particular, are an important metric for Starbucks’ Americas business as, in the most basic terms possible, more people going to work translates very closely into more people buying coffee as part of their daily routine.

Growth Runway

The strength of Starbucks’ Americas retail business is well-appreciated. Additional growth over the long-term TAIL will be largely driven by other segments of the business such as CPG, China, India, K-Cups, single-serve, home brewers, tea ($40 billion category), juice, and food among others. With management aiming to double the China unit count to 1,500 from 700 by the end of 2015 and viewing the CPG business as potentially becoming as large as the U.S. retail business, we believe that Starbucks is far from the end of the growth phase of its maturity curve.

Coffee Costs

Favorable coffee costs, coinciding with strong top-line growth, have resulted in strong earnings and cash flow generation. This tailwind is likely to continue through the end of the year and beyond, with management expecting a $100 million tailwind from coffee in 2014.

Management Team

This is not a quantifiable factor but for anyone that has been following the restaurant space for any significant period of time, it is evident that a management team’s aptitude is often evident in their communications with the investor communities. Starbucks, over the last five or six years, has demonstrated a consistency in its message and its commitment to prudent growth that has set is apart from most of its competitors. Starbucks’ brand is one of the best-recognized in the world as the company has taken proactive steps to build an industry-leading loyalty program and an unrivalled social media presence, which has manifested in strong organic growth.

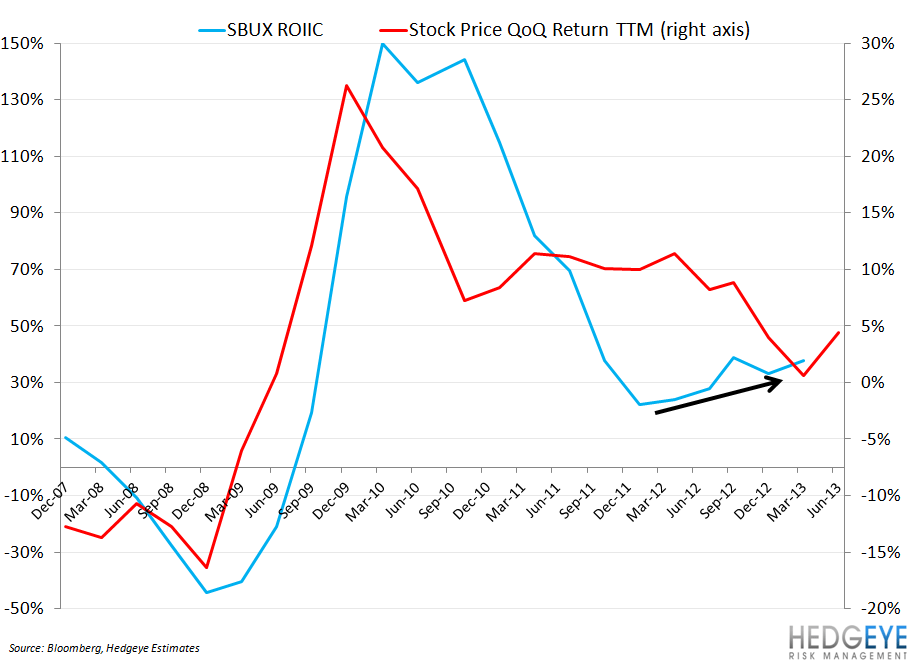

ROIIC

Last, but certainly not least, the ROIIC metric indicates that management is walking the walk. This chart is a key component of our process on all restaurant names – particularly those growing units – and Starbucks is better than most at sustaining a disciplined approach to expanding its business operations.

Howard Penney

Managing Director

Rory Green

Analyst