Continuing with our call, we believe that Mario Draghi and the ECB will keep rates unchanged this Thursday after making a big splash cutting the main interest rate by 25bps (to +0.50%) last month.

Here’s how we’re sizing up our positioning:

- Draghi has signaled that he expects a gradual recovery in growth in the back half of 2013, and therefore is monitoring the impact of the May 2nd interest rate cut and the current high-frequency data

- Manufacturing PMIs were better in MAY vs APR (48.3 vs 46.7)

- May Eurozone Confidence figures (Economic, Consumer, Business, Services, Industrial) all improved month-over-month

- Sovereign yields remain largely anchored and the majority of European equity markets are positive YTD

- The ECB needs more time to consider non-standard measures to encourage growth, including initial hints at 1.) Increased lending to small and medium-sized enterprises (SMEs) and 2.) Cutting the deposit rate to negative

- On SME funding, it’s not clear the channel by which the funding would be carried out, ie from top-down coordination (Brussels/ECB) or bottom-up (at the individual CB/State Government level)

- On a negative deposit rate, there is mixed discussion about the merits and benefits of such a move. Denmark provides one example of this and its government has claimed that it had no impact in boosting lending, and could negatively distort the property market. The jury is still clearly out on this option

- Consensus is baking in no change to rates: 41 of 42 economists polled by Bloomberg agree

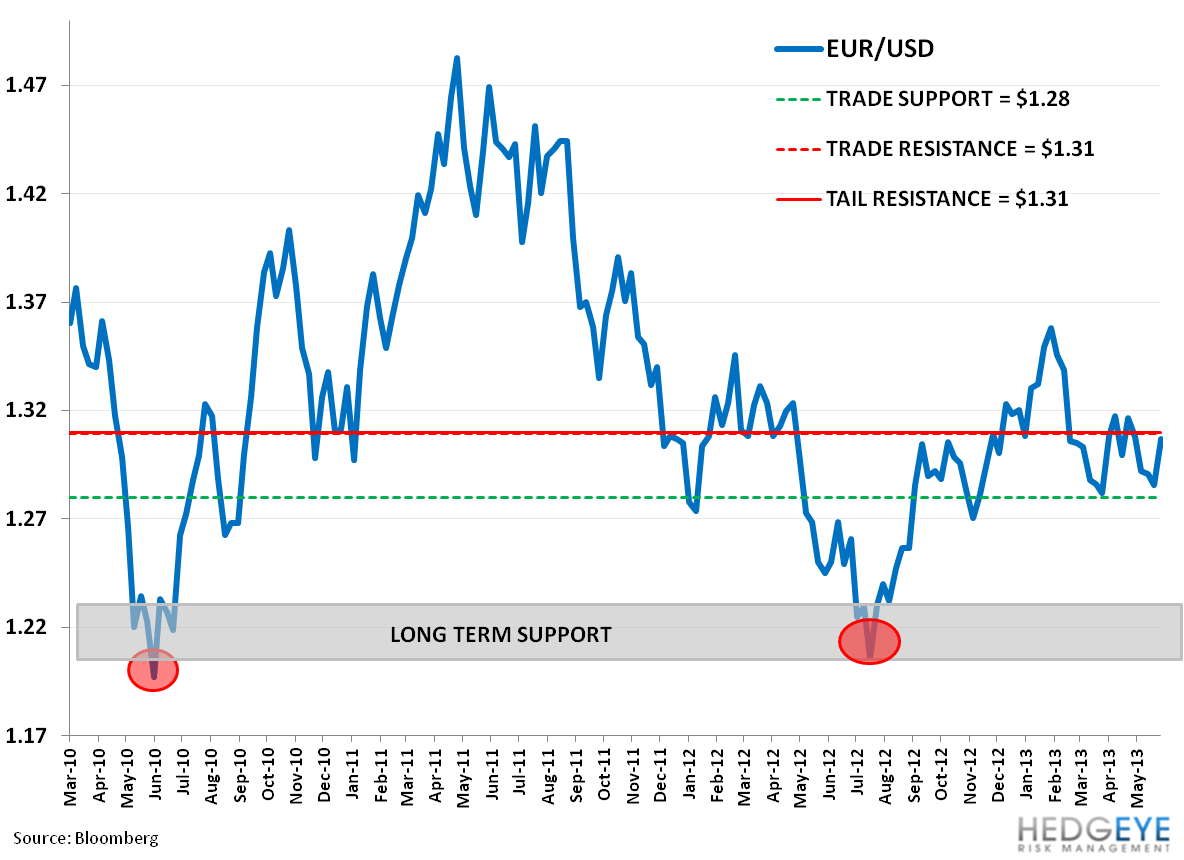

Our critical TAIL line of resistance on the EUR/USD at $1.31 has not changed over recent months. We’ll be monitoring this level closely into and out of Thursday’s ECB meeting. Our immediate term TRADE range is outlined in the chart below. (The cross can be traded via the etf FXE).

Matthew Hedrick

Senior Analyst